Medical bills can be extremely expensive and difficult to understand, and it's not uncommon for people to be slapped with a huge bill following an emergency room visit. However, there are ways to fight back against these charges. Firstly, it's important to check that the bill is accurate and that you actually owe it. Mistakes are common, so it's worth reviewing the bill for possible errors and asking for an itemised list of charges. If you have insurance, you should also check that the bill reflects what your provider understood would be covered. You can then dispute any incorrect or unexpected charges with the hospital billing department, and you may be able to negotiate a lower rate. If you are uninsured, you can still ask for a rate reduction in exchange for paying upfront, as hospitals would often rather collect something than nothing.

| Characteristics | Values |

|---|---|

| What to do if you can't pay a medical bill | Make sure the provider accurately calculated the bill and that you owe it before you pay. There may be protections under federal and state law as well as financial assistance that you may be entitled to claim. |

| What is a surprise bill | A surprise bill is when a consumer receives unexpected bills from out-of-network providers when they sought services at an in-network facility. |

| What to do if you receive a surprise bill | If you received a surprise bill for medical services provided after July 1, 2017, and have already paid more than your in-network cost share, file a complaint with your health insurer with a copy of the bill. |

| How to fight an outrageous medical bill | Challenge what's in your bill and how it was coded, ask for a prompt-pay discount, call the hospital multiple times, consider hiring a professional, and be aware that sometimes negotiating won't work and can even backfire. |

| How to lower your ER bill | Review your bill for possible errors, know your insurance policy, use a benchmark to negotiate, prevent a bigger bill by questioning all tests, and be smart about where and when to get care. |

Explore related products

What You'll Learn

![]()

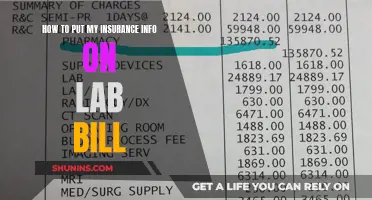

Review your bill for errors

Reviewing your bill for errors is an important step in disputing a medical bill. Here are some tips on how to do this effectively:

- Get an itemized copy of your bill: Ask for an itemized bill that lists every charge clearly. This will allow you to identify any double charges, coding mistakes, or incorrect calculations.

- Compare your bill to your insurance plan: Go through your itemized bill line by line and compare it against your health insurance plan to determine which charges you are responsible for and which ones your insurance company should cover. Also, check if there are any charges that should be covered by your provider.

- Wait for the Explanation of Benefits (EOB) report from your insurance company: The EOB will explain what your insurance company has covered for a specific date and healthcare visit. Make sure that the bill from the hospital or doctor reflects your benefits payment.

- Look for discrepancies: Check for any discrepancies such as tests you didn't receive, provider names you don't recognize, or incorrect dates of service. Ensure that the services you received align with the charges on your bill.

- Identify mistakes in your emergency room receipt: Emergency room receipts can contain mistakes, such as cancelled tests that were ordered but not performed, or errors in coding levels. Be sure to review your bill carefully to identify any potential errors.

- Compare your bills with the Explanation of Benefits (EOB): After reviewing your bills for accuracy, compare them with the EOB from your insurance company. Pay close attention to what you were charged, the amount the insurance company allowed, and what the insurance company paid or didn't pay for.

- Be aware of out-of-network charges: Even if the hospital is in your insurance network, some providers who treat you may be out-of-network, resulting in unexpected costs. In an emergency, you may have no choice but to be treated by out-of-network doctors. However, if your condition is not an emergency, consider visiting an in-network urgent care facility first to avoid higher costs.

- Contact the billing department: If you spot potential errors or have questions about your bill, start asking questions of the healthcare facility's billing department. Sometimes, just asking the question may lead to a discount.

CVS Flu Shot Services: Understanding Insurance Billing

You may want to see also

Explore related products

![]()

Understand your insurance policy

Understanding your insurance policy is crucial to know your rights and responsibilities in the event of a loss or medical emergency. Here are some essential things to keep in mind:

Know What's Covered and What's Not:

Read your policy document carefully. Understand the specific coverages provided, including medical procedures, prescription drugs, mental health care, etc. Be aware of any exclusions or limitations to your coverage. For example, some policies may not cover pre-existing conditions or certain types of treatments.

Understand Your Costs:

Familiarize yourself with key insurance terms like "deductible," "copayment," "coinsurance," and "premium." The deductible is the amount you pay out-of-pocket before your insurance company starts contributing. A copayment is a fixed amount you pay for a covered service, like a doctor's visit. Coinsurance is your share of the cost, usually calculated as a percentage of the allowed amount. The premium is the amount you pay monthly or annually for your insurance coverage.

Review the Declaration Page:

The declaration page is typically the first part of your insurance policy. It identifies the insured, the risks or property covered, policy limits, and the policy period. This section will give you a clear overview of who and what is covered, as well as the timeframe of your coverage.

Understand the Insuring Agreement:

The insuring agreement summarizes the insurance company's major promises. It states what is covered and what they agree to do in the event of a loss or claim. Understand the difference between named-perils coverage, where only listed perils are covered, and all-risk coverage, where all losses are covered except specified exclusions.

Be Aware of Exclusions and Conditions:

Exclusions take away coverage from the insuring agreement. Common exclusions include certain perils, causes of loss, and specific types of property. Conditions, on the other hand, are provisions that qualify or limit the insurer's promise to pay. For example, you may be required to protect your property after a loss or cooperate during an investigation.

Know Your Rights and Responsibilities:

Understand your rights as a policyholder, such as your right to dispute a claim or bill, and your responsibilities, such as providing accurate information and paying premiums on time. Knowing these will help you navigate any disagreements or disputes with your insurance company effectively.

Remember, insurance policies can be complex, and each policy is unique. Take the time to carefully review your entire policy, seek clarification from your insurance company or agent when needed, and don't be afraid to ask questions. This will ensure you are fully informed about your coverage and prepared to handle any emergencies or claims that may arise.

Understanding Term Life Insurance: A Guide to This Crucial Coverage

You may want to see also

Explore related products

![]()

Use a benchmark to negotiate

If you've received a large bill for emergency treatment, it's worth checking whether the charges are reasonable compared with a benchmark. If they aren't, you can use the benchmark to negotiate a lower bill.

How to find a benchmark

You can use a resource like Healthcare Blue Book to look up the average fees for a particular service in your location. You can also use an AI search tool like ChatGPT to look up what Medicare pays on average for a certain service, based on the service's unique medical code, called a CPT code. Medicare pays lower rates than private health insurers, so the hospital or healthcare provider is still able to make a profit at these rates.

How to use the benchmark to negotiate

Once you have the benchmark, you can tell the hospital's billing department that it's the amount you're willing and able to pay under an interest-free payment plan within your budget.

Other tips for negotiating a medical bill

- Offer to pay upfront: If you can afford to pay a portion of the bill upfront, you may be able to earn a discount.

- Ask about financial assistance programs: Nonprofit hospitals are required to make it clear that financial assistance programs are in place.

- Appeal your insurance claim: If you believe what you're being asked to pay is incorrect, you can submit an internal appeal and request an external review.

Challenging a Hospital Bill: Navigating the Process Without Insurance

You may want to see also

Explore related products

![]()

Apply for hospital financial aid

If you have received a large medical bill and are concerned about your ability to pay, you may be able to apply for hospital financial aid, also known as "charity care". This is a requirement for nonprofit hospitals under the Affordable Care Act, but for-profit hospitals may also have financial assistance policies in place.

To apply for financial aid, you will first need to verify that the hospital you received treatment from offers financial assistance. You can do this by searching for the hospital's financial assistance policy online, calling the hospital, or asking for a copy of their policy if you are still at the hospital. Nonprofit hospitals are required to make this information easily accessible on their websites, along with an application form and a plain-language summary of the policy.

Once you have found the relevant information, you will need to check that you meet the eligibility criteria outlined in the policy. Each hospital's policy is different, but you will usually need to demonstrate financial need and may also need to show that you have already exhausted other insurance options. Some hospitals use a sliding scale to determine the level of assistance they will provide, with lower-income patients receiving more support. You may also need to show that the procedure you underwent qualifies for financial assistance, as some treatments may not be covered.

If you meet the eligibility criteria, you can then follow the instructions in the policy to apply for financial assistance. This may involve submitting an application form online or by mail, and you will likely need to provide documentation of your financial situation, such as proof of income. The hospital's billing department should be your first point of contact if you have any questions about the process.

It is important to start the application process as soon as possible, as there may be deadlines for applying, and you don't want to risk your bill being sent to collections. If your bill is already in collections, be sure to notify the debt collectors that you are seeking financial assistance and ask them to pause collections while your application is being processed.

Navigating the Insurance Billing Process as a BCBA: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Ask for a prompt-pay discount

If you have received a large bill for emergency treatment and you don't have insurance, one strategy is to ask for a prompt-pay discount. Many hospitals are willing to offer discounts if you pay your bill within a short time frame. This is because they know that collecting payment can be a lengthy and difficult process, so they would rather receive a lower amount promptly than spend time and resources chasing the full amount.

You can ask for a prompt-pay discount by calling the hospital's billing department and requesting information on payment options. You should also ask about any potential discounts for early payment. It is a good idea to get a sense of the typical fees for the service you received, so that you know whether the bill is reasonable. You can do this by using a resource like Healthcare Blue Book, which lists average fees for services in your location. If the bill seems excessive, you can use this information to negotiate a lower rate.

When negotiating, it is important to remain calm and polite. You could say something like: "I received this bill for [amount] and I wanted to discuss payment options. I understand that the typical fee for this service in this area is [amount], so I am wondering if there is any flexibility on the amount charged. I am able to pay promptly, and I would be happy to discuss a payment plan."

If the billing department is not willing to negotiate, you could try asking to speak to a supervisor, who may have more flexibility. Remember to always document your conversations, including the date, time, and name of the person you spoke to. This will help you keep track of your discussions and show that you are serious about resolving the issue.

Overall, asking for a prompt-pay discount can be an effective way to reduce your emergency bill when you don't have insurance. It is important to act quickly, be polite but assertive, and be prepared to negotiate.

Emergency Aid: Unraveling the Complexities of Ambulance Insurance Billing

You may want to see also

Frequently asked questions

First, make sure that you owe the bill. Check the charges and ask for an itemized list of charges if something doesn't look right. If you have insurance, check that the bill reflects the payment by your insurance company. You can also dispute a medical bill with a debt collector or a credit reporting company.

A surprise bill is an unexpected bill from an out-of-network provider when you sought services at an in-network facility. This could be because the provider is not in your health insurer's network, even though you had no choice in who your provider was.

If you received a surprise bill for medical services provided after July 1, 2017, and have already paid more than your in-network cost share, file a complaint with your health insurer with a copy of the bill. Your health insurer will review your complaint and should tell the provider to stop billing you.

The No Surprises Act protects people covered under group and individual health plans from receiving surprise medical bills when they receive most emergency services, non-emergency services from out-of-network providers at in-network facilities, and services from out-of-network air ambulance service providers.