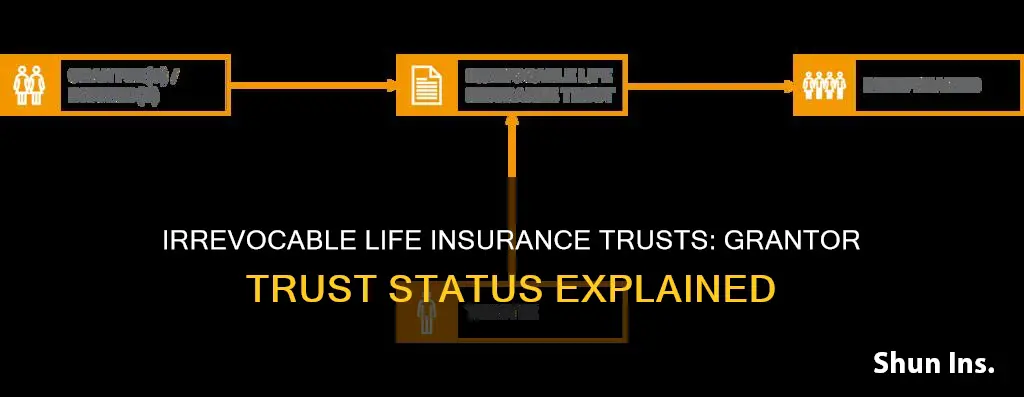

An irrevocable life insurance trust (ILIT) is a financial tool used to manage life insurance policies and allocate benefits when the grantor passes away. Once established, an ILIT cannot be altered or terminated. The grantor initiates and finances the trust, choosing a trustee to manage it and one or more beneficiaries to receive the benefits. The trustee pays the life insurance premiums, collects the death benefit when the grantor passes away, and handles payouts to the beneficiaries.

The ILIT is a separate legal entity from the grantor's estate and is not included in the estate's value. The trust owns the life insurance policy and is the payor, rather than the policy owner. The grantor typically pays the trust, and the trustee uses these funds to pay the life insurance premiums. When the grantor passes away, the trustee collects the life insurance payout and handles the distribution to the beneficiaries.

The ILIT has its own federal tax identification number and must file annual state and federal income tax returns, although it usually has no taxable income while the grantor is alive. When the grantor dies, the entity that owns the policy and collects the death benefit remains, so the death benefits are not taxed.

| Characteristics | Values |

|---|---|

| Modifiability | An ILIT is irrevocable and cannot be modified or terminated by the grantor |

| Ownership | The trust owns the life insurance policy and is the beneficiary of the policy |

| Control | The trustee manages the trust and distributes the proceeds to the beneficiaries |

| Taxation | The ILIT is considered a separate legal entity and is not included in the grantor's estate for taxation purposes; it has its own federal tax identification number and must file annual state and federal income tax returns |

| Purpose | To manage life insurance policies, minimize estate and gift taxes, protect government benefits, and provide liquidity to pay estate taxes |

| Parties | Grantor, trustee, and beneficiaries |

Explore related products

What You'll Learn

![]()

Irrevocable life insurance trusts (ILITs) are a type of financial tool

ILITs are irrevocable, meaning they cannot be rescinded, amended, or modified post-creation. They are constructed with a life insurance policy as the asset owned by the trust. Once the grantor contributes property or life insurance death benefits to the trust, they cannot change the terms of the trust or reclaim any of the properties held within. The grantor loses control of the assets before their death, and the beneficiaries can make changes to the trust.

The parties involved in an ILIT are the grantor, trustee(s), and beneficiaries. The grantor creates and funds the trust, choosing a trustee to manage it. The trustee pays the life insurance premiums, collects the death benefit when the grantor passes away, and handles payouts to the beneficiaries. The grantor chooses one or more beneficiaries to receive the ILIT's life insurance policy benefits.

ILITs offer several advantages, including tax advantages, asset protection, and the assurance that the benefits will be used according to the grantor's wishes. They can help minimize estate taxes, avoid gift taxes, and protect government benefits. ILITs are also useful for setting aside assets for specific purposes, such as paying estate taxes, as these assets are not taxable.

However, ILITs also have some drawbacks and complexities. They require careful attention and can be costly to set up, so they may not be suitable for everyone. It is important to consult with a lawyer and financial advisor when considering an ILIT.

Life Insurance and Capital Gains Tax: What's the Verdict?

You may want to see also

Explore related products

![]()

ILITs are used to manage life insurance policies

An irrevocable life insurance trust (ILIT) is a trust created during the insured's lifetime that owns and controls a term or permanent life insurance policy. It is a financial tool used to manage life insurance policies and allocate benefits when the grantor passes away. ILITs are constructed with a life insurance policy as the asset owned by the trust. The trust can also manage and distribute the proceeds that are paid out upon the insured’s death, according to the insured's wishes.

The parties in an ILIT are the grantor, trustees, and beneficiaries. The grantor typically creates and funds the ILIT. Gifts or transfers made to the ILIT are permanent. The trustee manages the ILIT and the beneficiaries receive distributions.

The primary reason for having an ILIT own a life insurance policy is to keep the insurance proceeds out of the grantor’s estate for estate tax purposes. When a grantor owns insurance on their own life, the proceeds will be included in the grantor’s taxable estate; when an ILIT owns the insurance, the proceeds typically will not be included in the grantor’s taxable estate. This can be a powerful tool for wealth management and can help ensure that the policy is used in the best possible way to benefit your family.

ILITs can also be used to control how benefits are distributed. For example, if the beneficiary in the life insurance trust is receiving government assistance, the life insurance benefits must be received in a way that does not disturb the government’s help. With an ILIT, there is more control over how and when money is distributed to beneficiaries.

Another benefit of ILITs is mitigating the generation-skipping transfer tax. Typically, the IRS can tax up to 40% of gifts to people over 37.5 years younger than the gift giver. This tax is not possible within an ILIT, allowing grantors to help prepare grandchildren listed as beneficiaries financially.

Borrowing from Life Insurance: Genworth's Policy Loan Option

You may want to see also

Explore related products

![]()

ILITs are beneficial for tax advantages

An irrevocable life insurance trust (ILIT) is a financial tool used to manage life insurance policies and allocate benefits when the grantor passes away. It is a trust designed to hold life insurance, existing separately from the grantor's estate and not included in the estate's value.

Avoiding Estate Taxes

If a life insurance policy is owned by an individual, the death benefit is included in their gross estate and is subject to state and federal estate taxation. However, when an ILIT owns the life insurance, the proceeds from the death benefit are not part of the insured's gross estate and are therefore not taxed. This can be especially useful for beneficiaries of estates valued at over $1 million, which is the threshold at which many states begin taxing estates.

Avoiding Gift Taxes

A properly-drafted ILIT avoids gift tax consequences since contributions by the grantor are considered gifts to the beneficiaries. To avoid gift taxes, the trustee must notify the beneficiaries of their right to withdraw a share of the contributions for a 30-day period. After 30 days, the trustee can then use the contributions to pay the insurance policy premium.

Protecting Government Benefits

The proceeds from a life insurance policy owned by an ILIT can help protect the benefits of a trust beneficiary who is receiving government aid, such as Social Security disability income or Medicaid. The trustee can control how distributions from the trust are used so as not to interfere with the beneficiary's eligibility to receive government benefits.

Tax-Free Death Benefit

The death benefit within an ILIT can be tax-free and provide funds to cover estate taxes and other expenses, avoiding the need to sell high-value assets such as a business or property.

Leveraging Annual Gift Tax Exclusion

An ILIT enables the grantor to leverage the annual gift tax exclusion by using gifts to pay the premiums on the life insurance in the trust. For example, in 2024, an individual can give up to $18,000 a year to a beneficiary without reporting it to the Internal Revenue Service (IRS).

Protection from Divorce, Creditors, and Legal Action

An ILIT can protect insurance benefits from divorce, creditors, and legal action against the grantor and beneficiaries.

Variable Life Insurance: Taxable Death Benefits?

You may want to see also

Explore related products

![]()

ILITs are a good way to protect assets from creditors

An irrevocable life insurance trust (ILIT) is a financial tool used to manage life insurance policies and allocate benefits when someone passes away. ILITs are a good way to protect assets from creditors, as they are irrevocable and separate from the grantor's estate. This means that the trust owns the life insurance policy, and the grantor typically pays the trust, which then pays the insurance premiums. When the grantor passes away, the trustee collects the insurance payout and handles the payouts to the beneficiaries.

ILITs offer several benefits that can help protect assets from creditors. Firstly, they can be used to minimise estate taxes, as the proceeds from the death benefit are excluded from the grantor's estate and are not subject to state and federal estate taxation. Secondly, ILITs can help protect government benefits for beneficiaries who are receiving aid such as Social Security disability income or Medicaid. The trustee can control how distributions from the trust are used to ensure the beneficiary's eligibility for government benefits is not affected.

Additionally, ILITs can provide asset protection for beneficiaries in the event of future litigation. Since the trust is not considered owned by the beneficiaries, it can be difficult for courts to link the assets to them, making it challenging for creditors to access them. ILITs also offer favourable tax treatment, as the cash value accumulating in a life insurance policy and the death benefit are tax-free.

While ILITs offer strong protection against creditors, it is important to note that they cannot be modified once established. Therefore, it is crucial to carefully consider the implications and seek expert advice before setting up an ILIT.

Understanding the Diverse World of Life Insurance Options

You may want to see also

![]()

ILITs are a good option for legacy planning

Irrevocable Life Insurance Trusts (ILITs) are an excellent option for legacy planning. They are a powerful tool that can be leveraged for legacy planning in many wealth management plans to ensure that the policy is used in the best way to benefit your family.

One of the main benefits of ILITs is that they can be used to minimize estate taxes. When a life insurance policy is owned by an individual, the death benefit is included in their gross estate and is subject to state and federal estate taxation. However, when the policy is owned by an ILIT, the proceeds from the death benefit are not part of the insured's gross estate and are therefore not subject to these taxes. This can result in a greater percentage of assets being passed on to future generations.

Another advantage of ILITs is that they can be used to avoid gift taxes. A properly drafted ILIT avoids gift tax consequences since contributions by the grantor are considered gifts to the beneficiaries. Additionally, ILITs can help protect the benefits of a trust beneficiary who is receiving government aid, such as Social Security disability income or Medicaid. The trustee can control how distributions from the trust are used to ensure that the beneficiary's eligibility for government benefits is not affected.

Furthermore, ILITs offer a level of asset protection for the beneficiaries. Since ILITs are not considered to be owned by the beneficiaries, it is difficult for courts to link the assets to them, making it nearly impossible for creditors to access them. This can be especially useful in cases where the beneficiary may become embroiled in future litigation.

In addition to the financial advantages, ILITs also offer legal advantages. They provide heirs with the assurance that the benefits will be used according to the benefactor's wishes, as an appointed trustee can supervise the trust and distribute the assets accordingly. This can be particularly important if the insured has beneficiaries who are minors or adults with a history of reckless spending habits.

Overall, ILITs are a good option for legacy planning as they offer both financial and legal benefits that can help ensure that the insured's wishes are carried out and that their heirs receive the maximum benefit from the policy.

Life Insurance: Money Pit or Smart Investment?

You may want to see also

Frequently asked questions

An irrevocable life insurance trust (ILIT) is a trust that cannot be altered or undone after its creation. It is created to own and control a term or permanent life insurance policy or policies while the insured is alive.

An ILIT can be used to minimize estate taxes, avoid gift taxes, protect government benefits, and more. It also provides a level of asset protection for the beneficiaries.

One of the main drawbacks of an ILIT is that it cannot be modified once it is finalized. This means that any assets put into the trust cannot be reclaimed by the grantor. Additionally, while ILIT assets are not taxed as part of the grantor's estate, they are taxed as part of the beneficiaries' estates.

An ILIT involves three legal parties: the grantor, the trustee, and the beneficiaries. The grantor creates and funds the trust, the trustee manages it, and the beneficiaries receive distributions. The trustee pays the life insurance premiums and collects the death benefit when the grantor passes away.

Irrevocable life insurance trusts are complicated legal entities and require expertise to set up. It is recommended to work with an experienced lawyer and a financial advisor to properly establish the trust.