Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance) are the two primary components of Original Medicare, which serves as the foundation of Medicare coverage. While Original Medicare is the most straightforward option and has the lowest monthly premiums, it is important to understand its limitations. For instance, neither Medicare Part A nor Part B covers prescription drugs, dental, vision, or hearing. These gaps in coverage may necessitate additional insurance, such as Medicare Supplement Insurance (Medigap) or a Medicare Advantage Plan. Furthermore, enrolling only in Medicare Parts A and B may impact your eligibility for other healthcare coverage options. Therefore, it is essential to carefully consider your specific healthcare needs when deciding if Medicare Parts A and B provide sufficient insurance coverage.

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

What You'll Learn

![]()

Medicare Part A and Part B explained

Medicare is federal health insurance for anyone aged 65 and over, as well as some people under 65 with certain disabilities. It is available in two main ways: Original Medicare and Medicare Advantage. Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance).

Part A helps cover inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Part A also covers doctors' services and tests, and preventive services. You must be lawfully present in the US for Medicare to pay for Part A and Part B-covered services.

Part B helps cover medical insurance costs, including doctors' services and tests, and preventive services. It is important to note that Part B does not cover all medical costs, and you may still be responsible for some out-of-pocket expenses.

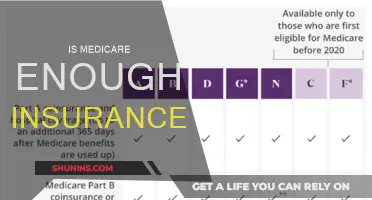

You can also shop for and buy supplemental coverage that helps pay your out-of-pocket costs for Part A and Part B. This is known as Medicare Supplement Insurance or Medigap. Medigap policies are standardized and, in most states, are named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, regardless of the insurance company. The price is the only difference between policies with the same letter sold by different companies. Generally, you need Part A and Part B to buy a Medigap policy.

Medicare Advantage, also known as Part C, is an alternative to Original Medicare that bundles several coverage types, including Parts A, B, and usually D (prescription drug coverage). Medicare Advantage plans are approved by Medicare and offered by private companies. These plans often have different out-of-pocket costs than Original Medicare or Medigap, and you may be restricted to using doctors within the plan's network.

Apple Medical Insurance: Getting Covered and Staying Healthy

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UY218_.jpg)

![]()

Limitations of Original Medicare

Original Medicare, also known as traditional Medicare, has limitations in terms of coverage, provider options, and out-of-pocket costs.

Firstly, it's important to note that Original Medicare does not cover all medical services and items. While Part A covers inpatient hospital care, skilled nursing care, home care, and hospice care, there are gaps in coverage for certain services and items. For example, Original Medicare typically does not cover most dental services, including routine cleanings, fillings, tooth extractions, or dentures. Additionally, it may not cover certain vision and hearing services, as well as some prescription drugs. To fill these gaps, individuals may need to purchase supplemental coverage, such as Medicare Supplement Insurance (Medigap) or a separate Medicare drug plan.

Secondly, Original Medicare provides more flexibility in choosing healthcare providers compared to Medicare Advantage. With Original Medicare, individuals can access any doctor or hospital that accepts Medicare across the United States. There are no provider networks or restrictions, allowing individuals to continue seeing their preferred healthcare providers without needing referrals to specialists. However, it's important to note that only about 83% of primary care physicians accept new Medicare patients, and a small percentage of doctors do not participate in Medicare at all.

Another limitation of Original Medicare is the potential for higher out-of-pocket costs. Unlike Medicare Advantage plans, Original Medicare does not have an annual cap on out-of-pocket expenses. This means that individuals could end up paying a significant amount of money if they require extensive medical care. To mitigate this, individuals can consider purchasing supplemental coverage, such as Medigap, which can help cover some of the out-of-pocket costs associated with Original Medicare.

Additionally, Original Medicare may not be sufficient for individuals who require extensive prescription drug coverage. While Medicare Advantage plans often include Part D coverage for prescription drugs, Original Medicare does not automatically include this benefit. Individuals with Original Medicare would need to enrol in a separate Medicare drug plan, and there may be penalties for late enrolment if they do not sign up when they first become eligible for Medicare.

Lastly, Original Medicare may not cover healthcare services received outside of the United States. For individuals who frequently travel internationally or spend extended periods abroad, this could be a significant limitation. In such cases, seeking alternative coverage options or purchasing travel insurance that includes healthcare coverage may be necessary.

How to Get Your Kaiser Medical Record Number

You may want to see also

Explore related products

$19.95 $14.95

![]()

Additional coverage and costs

Original Medicare consists of two main parts: Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance). These two components form the foundation of Medicare coverage, but they have their limitations. For instance, Medicare Part A does not cover all hospital costs, and there is a deductible for each benefit period. Similarly, Medicare Part B does not cover prescription drugs, dental, vision, or hearing.

If you only have Original Medicare, you may want to consider additional coverage to fill in the gaps. One option is to enroll in a Medigap policy, which is standardized and offered by private insurance companies. Medigap policies are typically named by letters, like Plan G or Plan K, and the benefits are the same no matter which insurance company sells them. The price is the only difference between policies with the same letter sold by different companies. It is recommended to buy a Medigap policy within six months of getting Part A and Part B to avoid medical underwriting and potential denial of coverage.

Another option for additional coverage is to enroll in Medicare Part D, which provides prescription drug coverage. Most Medicare Advantage Plans include Part D coverage, and it is important to note that you cannot join a separate Medicare drug plan with most Medicare Advantage Plans. Additionally, there is a Part D late enrollment penalty if you go 63 days or more without creditable drug coverage after getting Medicare, and this penalty is paid monthly for as long as you have Part D coverage.

Medicare Advantage Plans are an alternative to Original Medicare and offer health and drug coverage. With Medicare Advantage, you typically can only use doctors who are in the plan's network. It is important to compare the costs and coverage of Original Medicare and Medicare Advantage to determine which option is best for your needs.

The cost of Medicare varies based on factors such as the policy chosen, where you live, and your income level. There is no yearly limit on out-of-pocket expenses unless you have supplemental coverage or join a Medicare Advantage Plan. If you have limited income and resources, you may be eligible for assistance with premiums, deductibles, coinsurance, and copayments.

Medicaid as Secondary Insurance: Kentucky's Options Explored

You may want to see also

Explore related products

![]()

Medigap eligibility

Medigap, also known as Medicare Supplement Insurance, is an optional insurance policy that helps cover the gaps in Original Medicare (Parts A and B) plans. It is important to note that Medigap is not available to everyone, and there are specific eligibility requirements that must be met to qualify for a Medigap policy.

To be eligible for a Medigap policy, you must be enrolled in Medicare Parts A (Hospital Insurance) and Part B (Medical Insurance). Additionally, you must be a US citizen or a permanent legal resident for at least five continuous years, and meet one of the following qualifications:

- Be 65 years or older.

- Have End-Stage Renal Disease (ESRD), also known as permanent kidney failure requiring dialysis or transplant.

- Receive disability benefits from the Social Security Administration or the Railroad Retirement Board for at least 24 months consecutively.

- Be diagnosed with Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig's disease.

The best time to buy a Medigap policy is during the Medigap Open Enrollment Period, which is a one-time, six-month window that starts when you are 65 or older and enrolled in Medicare Part B. During this period, insurance companies cannot deny you coverage or charge you more due to pre-existing health conditions. If you delay enrolling in Medicare Part B because you are still working, your Medigap Open Enrollment Period will begin when you do enroll in Part B.

After the Medigap Open Enrollment Period ends, your options to buy a Medigap policy may be limited, and the policy may cost more. Additionally, insurers may use your medical history to determine your premium and eligibility for coverage. However, you can still apply for Medigap at any time, and certain situations may grant a guaranteed-issue right to Medigap. For example, if you have a Medicare SELECT policy and move out of its coverage area, you have the right to purchase a different Medigap policy in your new location.

Anxiety Medication Costs: Insurance Coverage and Expenses

You may want to see also

Explore related products

![]()

Medicare Advantage Plans

When considering a Medicare Advantage Plan, it is important to review the specific benefits offered by each plan as they can vary. For example, some plans may only offer Part B coverage, and not all plans include drug coverage. Additionally, Medicare Advantage Plans typically have a network of approved doctors and hospitals that you must use to receive coverage.

Before enrolling in a Medicare Advantage Plan, it is recommended to consult with your employer, union, or benefits administrator to understand how it may affect your existing coverage. In some cases, enrolling in a Medicare Advantage Plan might cause you to lose your current coverage, including that of your spouse and dependents. It is also important to note that Medicare Advantage Plans can disenroll you for reasons such as moving outside their service area or losing Medicare eligibility. Therefore, it is crucial to review your options and understand the specific terms and conditions of the plan.

Prescription Drug Insurance: Understanding Your Medicare Options

You may want to see also

Frequently asked questions

Medicare Part A covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care services.

Medicare Part B is medical insurance. Most people pay a monthly premium for Part B.

Medicare Part A and B form the foundation of Medicare coverage. However, there are gaps in Original Medicare coverage. For instance, neither Medicare Part A nor B provides comprehensive prescription drug, dental, vision, or hearing coverage. Therefore, it is essential to understand the benefits and limitations of Medicare Part A and B before deciding whether you need additional coverage.