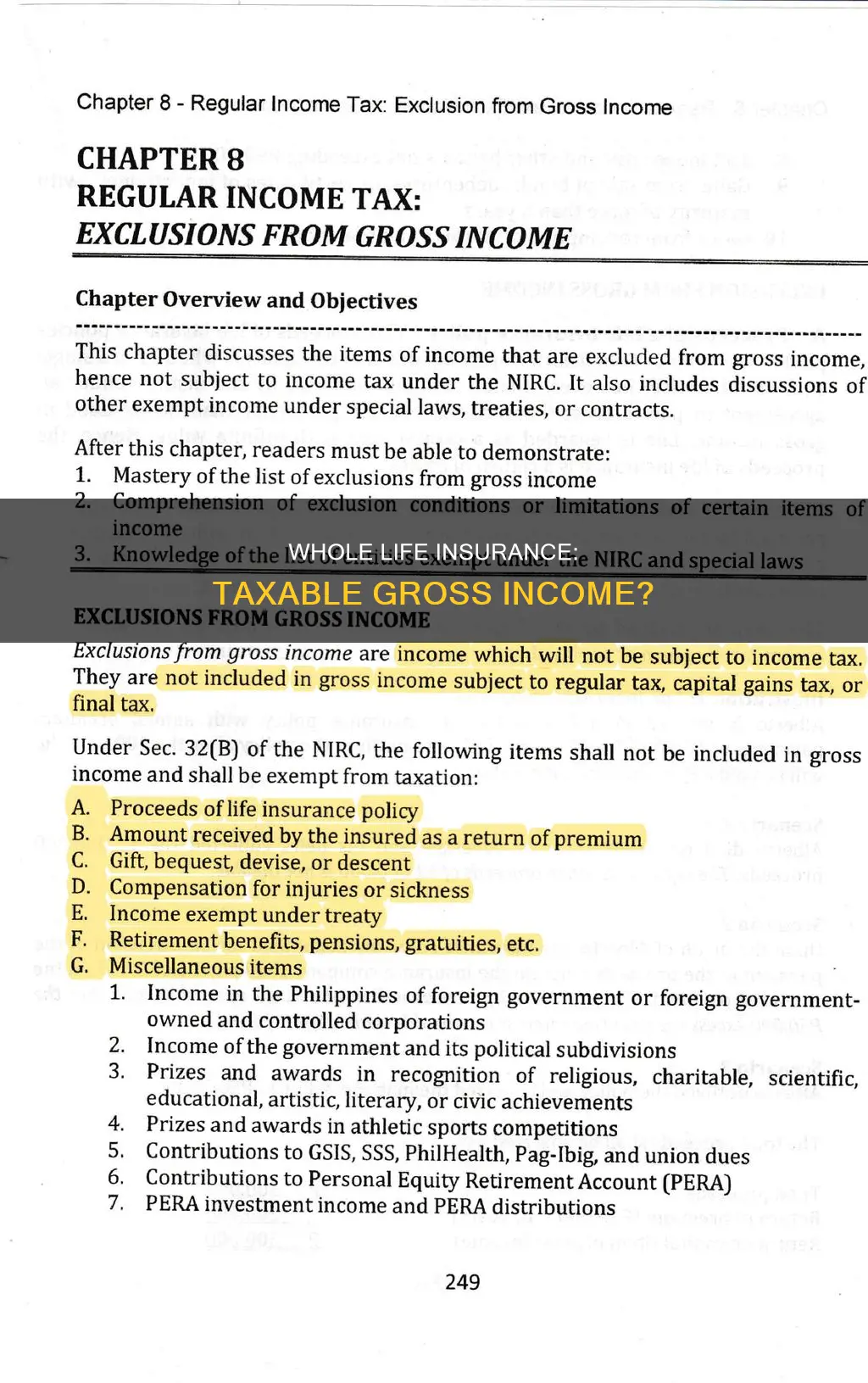

Whole life insurance is a type of permanent life insurance that provides coverage for the entirety of the policyholder's life, as long as premiums are paid. It also has a cash value component that grows over time and can be used during the lifetime of the policyholder. This cash value is not taxed while it is growing, but once the policy is cashed out, the difference between the cash value and the total amount paid in premiums is taxed as income. Whole life insurance proceeds paid to beneficiaries upon the death of the policyholder are generally not considered part of the beneficiary's gross income and are therefore not taxed. However, there are certain exceptions to this rule, such as when the payout is structured in multiple payments or when the policyholder has withdrawn money or taken out a loan.

Explore related products

What You'll Learn

- Interest on whole life insurance policies is not taxed until the policy is cashed out

- Whole life insurance death benefits are not taxable

- Whole life insurance cash value is not taxable

- Whole life insurance premiums are not tax-deductible

- Whole life insurance policies can be used to reduce tax obligations on other income

![]()

Interest on whole life insurance policies is not taxed until the policy is cashed out

Whole life insurance is a type of permanent life insurance that lasts for the rest of your life, as long as you continue to pay your premiums. It has a death benefit and a secure cash value account that grows over time. The premiums and death benefit remain the same. Whole life insurance policies also accumulate cash value as policyholders pay into the plans with their premium dollars. A portion of the premium dollars goes into a fund that accumulates interest.

The interest generated from whole life insurance policies is not taxed until the policy is cashed out. This is known as "tax-deferred", and it means that your money grows faster because it is not being reduced by taxes each year. The interest you make on your cash value is applied to a higher amount. This is beneficial because your earning power during your prime working years will likely put you in a higher income bracket, meaning you pay a higher percentage of your income in taxes. Later in life, when you are no longer earning a regular paycheck, your income and tax bracket could be lower. So, if you withdraw your money when you are in a lower tax bracket, it will be taxed less than when it was first applied to your account.

The cash value of your whole life insurance policy will not be taxed while it is growing. You can access the cash value while you are still alive through a loan, withdrawal, or policy surrender. However, if you withdraw more than the total amount of premiums paid, the excess may be taxable. If you decide to borrow against your cash value, it will not be treated as taxable income, but it will have interest charged by the insurance company until you pay it back.

If you choose to cash out your whole life insurance policy, the amount you are required to pay taxes on is the difference between the cash value you receive and the total you paid in premiums during the time the policy was in force. For example, if you pay $100 per month for 20 years ($24,000) and then cash out the policy and receive $30,000, the amount subject to taxes is $6,000.

Canceling Life Insurance in Florida: What You Need to Know

You may want to see also

Explore related products

![]()

Whole life insurance death benefits are not taxable

However, there are some exceptions and special cases to be aware of. For example, if the payout is structured to be paid in multiple instalments, these payments can be taxable. This is because the payments include proceeds and interest, and it is the interest that is taxed.

Another exception is if the policyholder has withdrawn money or taken out a loan. Whole life insurance policies earn cash value/interest over time, and if the money withdrawn or loaned is more than the total amount of premiums paid, then the excess may be taxable.

If you surrender your policy, the amount you paid into your policy (the cash basis) that you get back is considered a tax-free return of your principal. However, any funds over your policy's cash basis will be taxed as regular income.

It is also important to note that, according to the IRS, if life insurance proceeds are included as part of the deceased's estate and together exceed the federal estate tax threshold of $12.92 million (as of 2023), estate taxes must be paid on the proceeds over the allowed limit.

Life Insurance After a DUI: What You Need to Know

You may want to see also

Explore related products

![]()

Whole life insurance cash value is not taxable

Whole life insurance is a type of permanent plan that lasts for the rest of your life, provided you continue to pay your premiums. It has a death benefit and a secure cash value account that grows tax-free. The cash value of your whole life insurance policy will not be taxed while it's growing. This is known as "tax-deferred", and it means that your money grows faster because it's not being reduced by taxes each year. This means that the interest you make on your cash value is applied to a higher amount.

The cash value of your whole life insurance policy is not included in gross income and is not taxed until the policy is cashed out. This means that, in many cases, you won't have to worry about paying taxes on it. However, there are some instances where you may owe taxes on the cash value. For example, if you withdraw more than the total amount of premiums paid, the excess may be taxable. Additionally, if the policy is classified as a Modified Endowment Contract (MEC), it will receive less favourable tax treatment than a non-MEC policy.

Another feature of whole life insurance is that, in many cases, the policyholder is allowed to take out a loan against the cash value of the policy without tax consequences. Taking out a loan reduces the death benefit value of the policy until it is repaid, along with any interest owed. It's important to note that if the policy terminates before the loan is repaid, the policyholder might receive a tax bill.

Globe Life Insurance: Overdose Coverage Explained

You may want to see also

Explore related products

![]()

Whole life insurance premiums are not tax-deductible

Life insurance is a financial product that provides a lump-sum payment to beneficiaries upon the death of the insured. The death benefit remains in effect as long as the policyholder pays the insurance premiums. The amount of the premium depends on the insured's age and health, the size of the death benefit, and the type of coverage. While life insurance is intended to support beneficiaries, it is still subject to certain tax implications.

However, there are a few exceptions to this rule. If you are not directly or indirectly a beneficiary of the policy, you may be able to deduct the premiums as a business expense. Additionally, if you are divorced and your divorce agreement was executed before 2019, any life insurance premiums you pay as part of that agreement may be considered alimony and can be deducted from your income taxes.

It is important to note that while whole life insurance premiums themselves are not tax-deductible, there may be other tax implications associated with the policy. For example, if you take out a loan against the cash value of the policy, the proceeds from the loan are typically not taxable, even if they exceed the total premiums paid. On the other hand, if you withdraw gains from interest or dividends, those amounts would generally be subject to income tax.

Furthermore, while the death benefit from a whole life insurance policy is generally not taxable, it may be included as part of the insured's estate for tax purposes if it exceeds the federal estate tax threshold. In such cases, estate taxes must be paid on the proceeds over the allowed limit.

Life Insurance Settlement: Guaranteed Payment Options

You may want to see also

Explore related products

![]()

Whole life insurance policies can be used to reduce tax obligations on other income

Borrowing Against the Policy:

Whole life insurance policies allow you to borrow against the cash value of the policy. This can be done without tax consequences as long as the loans are structured properly. The loaned amount is not considered taxable income, even if it exceeds the total premiums paid. However, it is important to work with a financial professional to ensure proper structuring and avoid unnecessary taxation.

Withdrawals and Dividends:

You can also access the cash value of your whole life insurance policy through withdrawals. As long as the withdrawals do not exceed the total amount of premiums paid, they are typically not subject to taxes. However, if you withdraw any gains, such as dividends or interest, those amounts would be taxed as ordinary income. Proper structuring is crucial to avoid unnecessary taxation.

Charitable Donations:

Donating to charities or non-profits is another way to reduce tax obligations. By signing over some of the benefits of your whole life insurance policy and naming a charity as a beneficiary, you may be able to claim a charitable income tax deduction. This strategy can help lower your taxable income while also supporting a cause that is important to you.

Tax-Deferred Growth:

The cash value of a whole life insurance policy grows tax-deferred. This means that the money grows faster because it is not reduced by taxes each year. The interest earned on the cash value is applied to a higher amount, resulting in greater overall growth. This can be advantageous, especially if your income and tax bracket are lower in retirement.

Death Benefits:

While not directly reducing tax obligations on other income, it is important to note that the death benefit paid out to beneficiaries from a whole life insurance policy is typically income-tax-free. This means that your loved ones will receive the full benefit without having to pay income taxes on it.

It is always recommended to consult with a financial professional and a tax advisor to understand the specific tax implications of your whole life insurance policy and how it can be utilized to reduce tax obligations on other income.

Retired Corrections Officers: Life Insurance Benefits in New York

You may want to see also

Frequently asked questions

Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person are not included in gross income and don't need to be reported to the IRS.

Yes, there are a few exceptions to this rule. If you opt for monthly installments instead of a lump sum, the funds that have yet to be distributed will accrue taxable interest. Also, if you plan to name your estate as a beneficiary, you may owe taxes as well.

Yes, the cash value of your whole life insurance policy will not be taxed while it's growing. This is known as "tax-deferred," and it means that your money grows faster because it's not being reduced by taxes each year.

Yes, it's important to note that if you withdraw more than the total amount of premiums paid, the excess may be taxable. Additionally, if your employer pays for your whole life insurance policy, the premium paid on policy amounts above $50,000 is considered part of your taxable income.