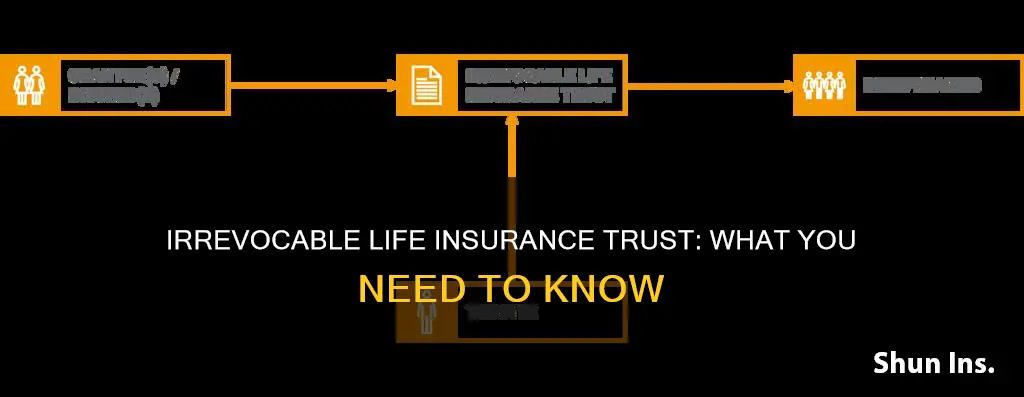

An irrevocable life insurance trust (ILIT) is a financial tool that helps individuals manage their life insurance policies and allocate benefits to beneficiaries when they pass away. It is a type of trust that holds one or more life insurance policies, allowing individuals to ensure that the benefits from a life insurance policy can avoid estate taxes and follow the interests of the insured. ILITs are constructed with a life insurance policy as the asset owned by the trust, and they involve three legal parties: the grantor, the trustee, and the beneficiary(ies).

| Characteristics | Values |

|---|---|

| Type of Trust | Irrevocable |

| Purpose | Estate planning, wealth transfer, tax reduction, asset protection, legacy planning |

| Parties Involved | Grantor, Trustee, Beneficiary/ies |

| Funding | Life insurance policy, income-producing asset |

| Control | Grantor gives up control of assets, beneficiaries cannot change or revoke the trust |

| Tax Implications | Avoids estate taxes, may incur gift tax, tax-free death benefit |

| Flexibility | Inflexible, difficult to modify or terminate |

| Use Cases | High-net-worth individuals, families with special needs, business owners, multiple beneficiaries |

Explore related products

What You'll Learn

![]()

Avoiding estate taxes

An irrevocable life insurance trust (ILIT) is a trust that holds one or more life insurance policies. It is a tool that can be used to avoid estate taxes.

When a person owns a life insurance policy, the proceeds from the policy are typically included in their estate's value, which can make the estate vulnerable to estate taxes. However, by transferring ownership of the policy to an ILIT, the proceeds are no longer considered part of the insured's estate and are therefore not subject to estate taxes. This is because the ILIT is a separate legal entity, and the proceeds from the life insurance policy are distributed to the beneficiaries of the trust, rather than the insured's estate.

In addition to avoiding estate taxes, an ILIT can also provide tax benefits during the grantor's lifetime by removing taxable assets from their portfolio. It also offers protection for government benefits, such as Social Security disability income or Medicaid, by allowing the trustee to carefully control how distributions from the trust are used, so as not to interfere with the beneficiary's eligibility for these benefits.

While an ILIT can be an effective tool for avoiding estate taxes, it is important to note that it is irreversible. Once the trust is created, it cannot be easily modified or terminated, and the grantor loses control over the assets within the trust. There may also be additional costs associated with setting up and maintaining an ILIT, such as professional fees and gift tax returns.

Maximizing Your Federal Life Insurance Benefits: Making Changes to FGLI

You may want to see also

Explore related products

![]()

Protecting legacy assets from creditors

An ILIT is a trust specifically designed to hold and control life insurance policies. It is a separate legal entity from the grantor's estate and is not included in the estate's value. The trust owns the life insurance policy, and the trustee pays the premiums and manages the policy. When the grantor passes away, the trustee collects the life insurance payout and distributes the proceeds to the beneficiaries.

One of the main advantages of an ILIT is its ability to protect legacy assets from estate taxes. In the US, if the value of an estate is over a certain threshold ($12.06 million in 2024), the estate becomes subject to a 40% federal estate tax. An ILIT can help reduce this tax burden by ensuring the proceeds from the life insurance policy are not considered part of the estate's value. This can provide liquidity to the estate, allowing beneficiaries to pay estate taxes while maintaining control of the estate's assets.

In addition to federal estate taxes, an ILIT can also help protect against state estate taxes. Each state has different rules and thresholds for estate taxes, and an ILIT can ensure that the value of the life insurance policy does not push the estate over these thresholds.

Another way an ILIT protects legacy assets is by shielding them from potential creditors. While each state has its own rules regarding how much of an insurance policy's value can be protected, any excess value above these limits is generally protected from the creditors of both the grantor and the beneficiary. This can be especially beneficial for individuals in highly litigious professions or those with beneficiaries who are at risk of legal action.

The irrevocable nature of an ILIT also ensures that the grantor's assets will be distributed according to their wishes. Once the trust is established, it cannot be changed or revoked, providing peace of mind that the grantor's legacy will be protected and preserved for their beneficiaries.

While an ILIT offers significant benefits in protecting legacy assets from creditors, it is important to carefully consider the potential downsides as well. Establishing an ILIT involves relinquishing control over the life insurance policy and accepting certain tax implications, such as potential gift tax payments. Consulting with legal and financial professionals is crucial to understanding the full implications of an ILIT and determining if it is the right choice for your estate planning needs.

Life and Health Insurance: Is Your License Active?

You may want to see also

Explore related products

![]()

Choosing a manager of assets

An irrevocable life insurance trust (ILIT) is a legal arrangement that seeks to minimise an individual's current tax burden and the impact of taxes on their estate after their death. An ILIT allows the insured to choose a manager of assets and how the beneficiaries receive them. This manager of assets is known as the trustee.

When choosing a trustee, it is important to select a reliable and trustworthy individual or company, as they will be responsible for handling estate matters. Effective communication between the grantor and trustee is also vital for successful trust management.

- Premium Payments: The trustee must ensure that insurance premiums are paid promptly and inform the grantor about payment amounts and due dates.

- Crummey Letters: Trustees must send annual letters to beneficiaries, notifying them of their right to withdraw their share of gifts made by the grantor to cover insurance premiums.

- Policy Monitoring: Trustees maintain regular contact with the insurance company, monitoring policy performance and status on behalf of the ILIT.

- Tax Reporting: The trustee is responsible for filing tax returns for the insurance trust, if required, and reporting any gifts made to comply with tax regulations.

- Distribution of Death Benefits: In the event of the grantor's death, the trustee ensures the proper distribution of policy proceeds among beneficiaries according to the provisions of the trust.

It is recommended to appoint an impartial third-party trustee to manage the affairs of the insurance trust. This can help ensure effective management and distribution of assets according to the wishes of the grantor.

Life Insurance: Should Employers Offer It?

You may want to see also

Explore related products

![]()

Avoiding probate

An irrevocable life insurance trust (ILIT) is a powerful tool for reducing estate taxes and protecting assets. By setting up an ILIT, individuals can keep the proceeds from a life insurance policy out of their taxable estate, avoiding probate. Here's how it works and the benefits it offers in avoiding probate:

How an ILIT Avoids Probate

When an individual sets up an ILIT, they transfer ownership of their life insurance policy to the trust. The ILIT then becomes the owner and beneficiary of the policy. Upon the individual's death, the life insurance payout goes directly to the trust beneficiaries, bypassing the individual's estate. This separation ensures that the death benefit is not considered part of the taxable estate, avoiding probate and the associated delays and expenses.

Benefits of an ILIT in Avoiding Probate:

- Estate Tax Reduction: The primary advantage of an ILIT is the significant reduction in estate taxes. By keeping the life insurance proceeds out of the taxable estate, individuals can save on taxes that could be as high as 40%.

- Asset Protection: ILITs protect assets from creditors' claims. The cash value and death benefits of the life insurance policy are shielded from civil lawsuits or bankruptcy.

- Preserving Government Benefits: ILITs can help beneficiaries maintain eligibility for means-tested government aid programs. The trustee can control distributions to ensure they do not interfere with government benefits.

- Control Over Distribution: ILITs allow grantors to control how the life insurance benefit is distributed. They can arrange for smaller, timed installments instead of a lump sum payout to beneficiaries.

- Avoid Gift Tax Consequences: Properly structured ILITs can help avoid gift tax consequences by utilizing the annual gift tax exclusion.

While ILITs offer significant benefits in avoiding probate, it's important to consider potential drawbacks, such as the loss of control over the policy and the complexity of setting up and managing the trust. Consulting with a professional is essential to determine if an ILIT aligns with an individual's specific needs and goals.

Life Insurance: Expensive or Affordable?

You may want to see also

![]()

Tax considerations

Irrevocable Life Insurance Trusts (ILITs) are a crucial aspect of estate planning, offering several tax advantages. Firstly, they enable individuals to ensure that the benefits from a life insurance policy are exempt from estate taxes, preventing the need to sell high-value assets to cover these taxes. This is achieved by transferring assets from the insured to the trust, which then uses a life insurance policy to distribute proceeds upon death.

ILITs also allow for the utilisation of the annual gift tax exclusion. Gifts can be used to pay premiums on the life insurance within the trust, and if structured correctly, can be excluded from gift taxes. The annual gift tax exclusion amount is $18,000 per beneficiary in 2024, and $19,000 in 2025. It's important to note that if the gifts exceed the yearly limit, they must be reported to the Internal Revenue Service (IRS) using Form 709.

Another key tax benefit of ILITs is the protection of government benefits for beneficiaries. The proceeds from a life insurance policy owned by an ILIT can safeguard government aid, such as Social Security disability income or Medicaid, for beneficiaries. The trustee can manage distributions to ensure they do not interfere with the beneficiary's eligibility for these benefits.

Furthermore, ILITs can provide tax-efficient wealth transfer to beneficiaries outside of the taxable estate. By removing taxable assets from the grantor's portfolio, ILITs may reduce their current tax burden. Additionally, the cash value accumulating in a life insurance policy and the death benefit are typically exempt from taxation when owned by an ILIT.

While ILITs offer significant tax advantages, it's important to consider potential drawbacks, such as the loss of personal control over the policy and associated costs for setting up and maintaining the trust.

How to Withdraw from Your Life Insurance Policy

You may want to see also

Frequently asked questions

An irrevocable life insurance trust (ILIT) is a financial tool used to manage life insurance policies and allocate benefits when someone passes away.

An ILIT involves three legal parties: the grantor, who initiates and finances the trust; the trustee, who manages the trust and pays the insurance premiums; and the beneficiary/beneficiaries, who receive the benefits of the policy.

ILITs can help to reduce the tax burden on an estate, ensure assets are distributed according to the grantor's wishes, and avoid probate. They can also protect beneficiaries from creditors and legal action, and ensure that inherited assets don't interfere with a beneficiary's eligibility for government benefits.

ILITs can create gift tax issues that impact the grantor's tax bill, and they are difficult to change or terminate.