Life insurance is often used as a tool for estate planning, which involves creating a plan to distribute a person's assets and liabilities after their death. An estate refers to the total collection of assets and items of value that belong to a person, which are passed on to their beneficiaries upon their death. Life insurance can be a significant asset that a person leaves to their beneficiaries, helping them avoid financial hardship and pursue essential goals. It can also be used to increase the value of the estate left to beneficiaries and assist in settling the deceased's affairs.

| Characteristics | Values |

|---|---|

| Definition | An estate is the total collection of assets and items of value that belong to a person, which are passed on to their beneficiaries upon their death. |

| Use in insurance | Life insurance is commonly used as part of estate planning. |

| Beneficiaries | Life insurance proceeds usually go directly to named beneficiaries, bypassing the estate. |

| No beneficiaries | If there are no beneficiaries, the proceeds may become part of the estate assets. |

| Taxes | The payout is often exempt from certain taxes, which makes life insurance attractive for estate planning. |

| Estate planning | Life insurance can help beneficiaries cover final expenses and estate taxes, and leave a nest egg for children. |

| Types of insurance | Term life insurance offers coverage for a specific period at an affordable rate but doesn't build cash value. Whole life insurance provides lifetime coverage and includes a cash value that grows over time. Universal life insurance offers flexible premiums and death benefit amounts, plus a cash value component. |

Explore related products

What You'll Learn

![]()

Life insurance and estate planning

Life insurance can be used in estate planning in several ways. Firstly, it can provide extra financial support to loved ones by helping to replace lost income, cover funeral costs, and pay off any debts. Life insurance policies can also be used to pay federal estate taxes, especially if there are delays in the distribution of assets. Secondly, life insurance can be used to divide ownership of a family business. Business owners can take out a life insurance policy that specifically outlines how ownership will be divided after their death, allowing each heir to decide whether to sell or keep their stake in the business. Thirdly, life insurance can benefit your estate by providing financial protection to your loved ones. For example, if you have outstanding debts at the time of your death, your family members may not be directly responsible for paying them back, but creditors could go after your estate. Life insurance can be used to pay off these debts, protecting your family's finances.

There are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance provides coverage for a fixed period, usually between 10 and 30 years, and is best suited for those with finite insurance needs, such as providing for minor children until they come of age. Permanent life insurance, on the other hand, provides lifetime coverage and is suitable for estate planning, especially for those with large or complex estates. Permanent life insurance can be used to pay estate taxes, eliminate inheritance inequities, and provide for heirs with disabilities. However, it is important to note that permanent life insurance can be significantly more expensive than term life insurance.

When choosing a life insurance policy, there are several factors to consider, including income, healthcare costs, family size, and business ownership. It is also important to carefully choose the beneficiary of your life insurance policy, as this person or entity will receive the death benefit shortly after your death. By combining life insurance and estate planning, you can create a comprehensive plan that provides invaluable financial support to your family and friends after your death.

Variable Life Insurance: Understanding the Savings Portion Calculation

You may want to see also

Explore related products

![]()

Life insurance beneficiaries

An estate is the total collection of assets and items of value belonging to a person, which are passed on to their beneficiaries upon their death. Life insurance is often used as part of estate planning and can be a significant asset that a decedent leaves to a beneficiary. Many people purchase life insurance policies to increase the value of the estate they leave to their beneficiaries.

There are two main types of life insurance beneficiaries: primary and contingent. The primary beneficiary is the person or entity first in line to receive the death benefit. The contingent beneficiary is the backup who will receive the payout if the primary beneficiary passes away before the insured or cannot be located.

It is important to keep beneficiary designations up to date, as life changes. Beneficiaries can be changed or updated at any time, but it is crucial to remember to do so. Failing to keep beneficiary designations current can result in the wrong person receiving the benefits.

In the case of no designated beneficiary, the death benefit may be paid to the insured person's estate and distributed according to their will or state laws. To avoid this, it is recommended to consult an estate planning attorney or financial professional to ensure that the death benefit is distributed according to the insured person's wishes.

Life Insurance Agents: Understanding Their Hourly Pay Structure

You may want to see also

Explore related products

![]()

Life insurance and wills

An estate refers to the total collection of assets and items of value that belong to a person, which are passed on to their beneficiaries upon their death. Life insurance is often used as part of estate planning and can significantly increase the value of the estate left to beneficiaries.

Life insurance is a long-term contract with an insurance company that pays out to the stated beneficiaries upon the death of the insured. It replaces the income of the deceased, helping their dependents maintain their standard of living, pay off debts, and save for the future. The death benefit from a life insurance policy provides a large cash sum that can make an immediate impact on beneficiaries, helping to protect families and transfer wealth to the next generation.

A will, on the other hand, is a legal document that outlines your wishes for the distribution of your assets and property after your death. It also specifies who should have custody of minor children. A will ensures that your assets are distributed according to your wishes and can help prevent family conflicts and streamline the distribution process.

It is important to regularly review your estate plan, including your life insurance policy and will, to ensure they align with your current wishes. While life insurance beneficiaries generally take precedence over a will, it is crucial to update your policy if your beneficiaries predecease you or if your wishes change.

In summary, life insurance and wills serve complementary roles in estate planning. Life insurance provides financial security for your loved ones, while a will ensures your assets are distributed according to your wishes. Together, they provide a comprehensive financial safety net for your beneficiaries and allow you to leave a lasting legacy.

Who Gets Your Life Insurance Payout: Contingent Beneficiaries Explained

You may want to see also

Explore related products

$13.94 $17.99

![]()

Life insurance and taxes

Life insurance is often used as part of estate planning. An estate is the total collection of assets and items of value belonging to a person, which are passed on to their beneficiaries upon their death. Life insurance can increase the value of the estate left to beneficiaries, such as children or spouses. It can also assist beneficiaries in settling the decedent's affairs.

Life insurance proceeds are generally not taxable. When the policyholder of a life insurance policy passes away, the proceeds or death benefits are paid to the named beneficiary or beneficiaries. This payout is usually not considered part of the beneficiary's gross income and is therefore not subject to income or estate taxes. However, there are some cases when a death benefit can be taxed.

If the payout is structured as multiple payments over time, such as an annuity, the payments can be subject to taxes. This is because the payments include both proceeds and interest, and the interest is considered taxable income. Similarly, if you have a whole life insurance policy that allows you to withdraw or take out a loan against the policy's cash value, and you withdraw more than your cumulative premium payments, you may have to pay income taxes on the excess amount.

In some cases, an employer-paid group life plan may be taxable according to the Internal Revenue Service (IRS). If the death benefit exceeds $50,000, the amount over $50,000 is subject to income taxes. Additionally, if life insurance proceeds are included as part of the deceased's estate and the total value exceeds the federal estate tax threshold, which was $13.61 million as of 2024, estate taxes must be paid on the amount above the limit. Some states also have their own inheritance or estate taxes, depending on the value of the estate and the location of the deceased.

It is important to consult with a tax advisor or estate planning attorney to understand the specific tax implications of life insurance in your unique situation.

Insure Your Life, Health, and Property: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Life insurance and debt

An estate is the total collection of assets and items of value that belong to a person, which are passed on to their beneficiaries upon their death. Life insurance is often used as part of estate planning and can be a significant asset that a decedent leaves to a beneficiary. Many people purchase life insurance policies to increase the value of the estate they leave to their beneficiaries.

Life insurance can also be used to pay off debt. Depending on the type of debt, it may be passed on to a spouse or other family members after death. Life insurance can be used to cover these debts and ensure that family members are not burdened.

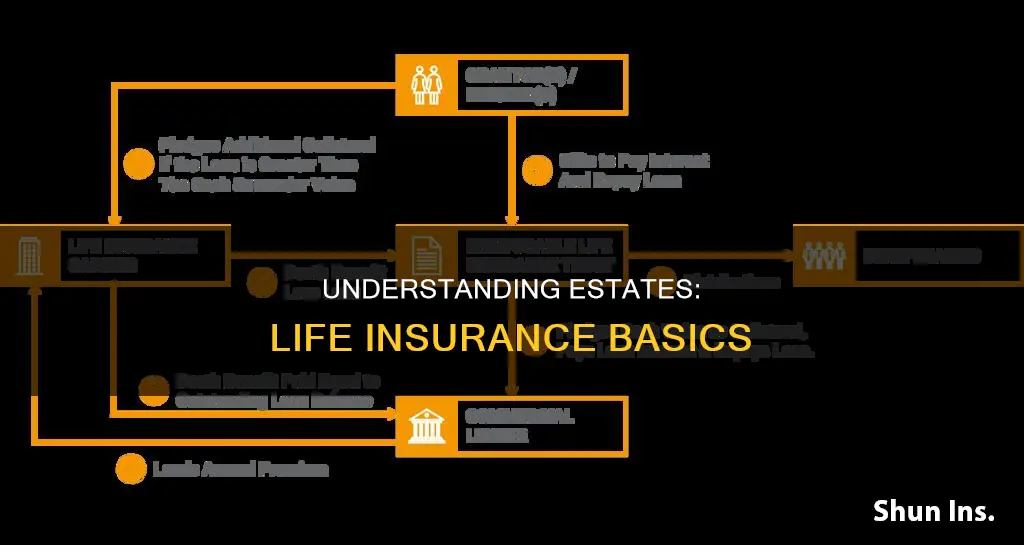

There are a few ways to use life insurance to pay off debt. One way is to name a trust as the beneficiary of the life insurance policy. The death benefit is then paid to the trust, and a trustee can distribute the funds according to the trust's instructions. This allows for more control over how and when loved ones receive the proceeds from the life insurance policy.

Another way to use life insurance to pay off debt is to borrow against the policy. This is only possible with certain types of life insurance policies, such as whole life or universal life, which accrue a cash value over time. Policyholders can borrow against this cash value to pay off debt, such as credit card debt. However, borrowing against a life insurance policy can reduce the death benefit, and there may be tax implications if the policy lapses.

It is important to carefully consider the pros and cons of using life insurance to pay off debt. While it can provide a tax-friendly way to help provide financial support and security for others, it can also reduce the death benefit and impact the estate's value. Consulting with professionals, such as an estate planning attorney or financial planner, can help individuals navigate the complexities of life insurance and estate planning to make the best decisions for their unique situations.

Check Your SBI Life Insurance Status: Quick and Easy Steps

You may want to see also

Frequently asked questions

An estate is the total collection of assets and items of value that belong to a person, which are passed on to their beneficiaries upon their death.

Life insurance can play a major role in estate planning, from helping beneficiaries cover final expenses and estate taxes to leaving a nest egg for children.

A life insurance beneficiary is the designated recipient of a life insurance policy's death benefit, while the beneficiary of a will receives a specific asset or assets from the deceased's estate.

Yes, if the value of the estate exceeds the federal estate tax threshold, placing a life insurance policy in an irrevocable trust can provide a tax-free inheritance for beneficiaries.

Life insurance can help equalize an estate with multiple heirs, especially when there are investments that are difficult to divide, such as real estate or a business.