Annuities and life insurance are both financial products offered by insurance companies. However, they are very different. Life insurance is designed to benefit your family after your death, while annuities are designed to provide you with an income during your retirement. In this article, we will explore the differences between these two products in more detail and consider how they can help with financial planning.

| Characteristics | Values |

|---|---|

| Purpose | Life insurance: to provide financial protection for loved ones after your death. Annuity: to provide a guaranteed income for yourself after retirement. |

| Protection | Life insurance: protects loved ones. Annuity: protects yourself. |

| Provider | Life insurance: provided by insurance companies. Annuity: provided by life insurance companies. |

| Payment | Life insurance: paid out to loved ones after your death. Annuity: paid out to you after retirement. |

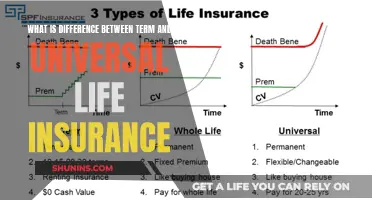

| Investment | Life insurance: better for leaving an inheritance. Annuity: more investment and income guarantees. |

Explore related products

$14.99 $14.95

What You'll Learn

- Annuities are a type of insurance contract designed to turn your money into future income payments

- Life insurance is better for leaving an inheritance

- Annuities are financial products offered by life insurance companies

- Life insurance policies protect your family's financial well-being in case you pass away

- Annuities help protect your financial well-being by providing a pension-like stream of income

![]()

Annuities are a type of insurance contract designed to turn your money into future income payments

Annuities are financial products offered by life insurance companies. They are created to help you meet a unique set of goals and objectives. While life insurance policies protect your family's financial well-being in case you pass away, annuities help protect your financial well-being by providing a pension-like stream of income that you can use to help fund your retirement.

Annuities provide the opposite type of protection to life insurance. Life insurance provides protection for loved ones when you die; annuities provide a guaranteed lifetime income for yourself, which means you won't outlive your assets or money.

Both annuities and life insurance can help provide financial security. However, it is important to consider your financial goals, budget, and needs when deciding whether both financial products are right for you.

MetLife Insurance: Can I Cancel My Policy?

You may want to see also

Explore related products

![]()

Life insurance is better for leaving an inheritance

Life insurance is designed to benefit your family after your death. It can financially help protect your partner, children, or other loved ones. This means that you can leave an inheritance for your family, which they will receive when you die.

Annuities, on the other hand, are designed to help protect your financial well-being. They provide a guaranteed income for yourself, either for a specific number of years or for your entire lifetime. This means that you won't outlive your assets or money. Annuities are a type of insurance contract, where you buy an annuity with either one lump sum payment or many payments over time. You can set up the annuity with a growth period, where it builds your savings.

While annuities can help to provide financial security, they are not as effective as life insurance when it comes to leaving an inheritance. Life insurance policies are specifically designed to provide financial support for your loved ones after your death, making them a better option if you want to leave money or assets to your family.

Suicide and Life Insurance: What Cover Does My Dad Have?

You may want to see also

Explore related products

![]()

Annuities are financial products offered by life insurance companies

Annuities are created to help you meet a unique set of goals and objectives. They help protect your financial well-being by providing a pension-like stream of income that you can use to help fund your retirement. In return for the premium paid by you, the insurance company will provide an income for a specific number of years, or for your entire lifetime, depending on your choice.

Annuities provide the opposite type of protection to life insurance. While life insurance provides protection for loved ones when you die, annuities provide a guaranteed lifetime income for yourself, which means you won't outlive your assets or money.

Canceling Guarantee Trust Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Life insurance policies protect your family's financial well-being in case you pass away

Life insurance policies are designed to protect your family's financial well-being in the event of your death. They are a way to ensure that your loved ones will be provided for financially after you're gone. This can include your partner, children, or other family members.

Life insurance is a good option if you want to leave an inheritance for your family. It provides peace of mind and added financial protection for your loved ones. There are different options available for policy design and coverage length, so you can choose a plan that suits your specific needs and budget.

In contrast, annuities are financial products offered by life insurance companies that provide a guaranteed income for yourself during your retirement years. With an annuity, you enter into a contract with the insurance company, agreeing to pay a premium in exchange for a steady income for a specified number of years or for the rest of your life. This income can be used to fund your retirement and ensure that you don't outlive your assets.

Annuities offer more investment and income guarantees than life insurance. You can choose to buy an annuity with a lump sum payment or through multiple payments over time. During the growth period, your savings will accumulate, and the return will depend on the type of annuity you choose. For example, a fixed annuity offers a guaranteed interest rate, while a variable annuity allows you to invest your savings in mutual funds.

While life insurance focuses on protecting your family after your passing, annuities are designed to protect your own financial well-being during retirement. Both products can provide added financial security, and it may be beneficial to consider both options when planning for your financial future.

Whole Life Insurance Interest: Taxable or Not?

You may want to see also

Explore related products

![]()

Annuities help protect your financial well-being by providing a pension-like stream of income

Annuities are a type of insurance contract designed to turn your money into future income payments. You can buy an annuity with either one lump sum payment or many payments over time. You can set up the annuity with a growth period, where it builds your savings. The return depends on the type of annuity. For example, a fixed annuity pays a guaranteed interest rate. A variable annuity lets you invest your savings in mutual funds.

Annuities are financial products offered by life insurance companies. They are created to help you meet a unique set of goals and objectives. Annuities help protect your financial well-being by providing a pension-like stream of income that you can use to help fund your retirement. This means that you won't outlive your assets or money.

Life insurance, on the other hand, protects your family's financial well-being in case you pass away. It is better for leaving an inheritance and can financially help protect your partner, children, or other loved ones.

Kansas Death Certificate Requirement for Life Insurance

You may want to see also

Frequently asked questions

Annuities provide a stream of income while you or your family are alive, whereas life insurance provides a cash payment on the death of the insured individual.

An annuity is a contract that offers a stream of cash flow for a set period of time, often during retirement, in exchange for money paid into the annuity.

Life insurance is a contract that offers a cash payment to the contract's beneficiaries if the policyholder dies while the policy is active and the terms of the contract are met.

Yes, it can be smart to have both an annuity and life insurance as each product offers a distinct form of added financial protection.