Group life insurance is a single contract for life insurance coverage that extends to a group of people. It is offered by an employer or another large-scale entity, such as an association or labour organisation, to its workers or members. Group life insurance is fairly inexpensive, and may even be free for certain employees. It is a common workplace benefit.

| Characteristics | Values |

|---|---|

| Who is it for? | A group of people, usually employees of a company or members of an organisation |

| Who purchases it? | The employer or organisation |

| Who pays for it? | The employer or organisation, although employees may pay for more advanced coverage |

| How much does it cost? | Relatively inexpensive |

| What does it cover? | Death |

| How much does it cover? | Relatively low coverage amount |

| When does coverage end? | When a member leaves the group |

| Who is it not suitable for? | Individuals |

Explore related products

What You'll Learn

![]()

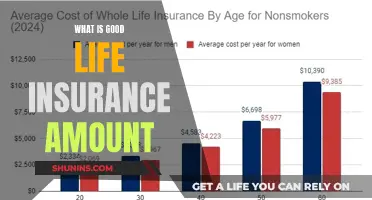

How much does group life insurance cost?

Group life insurance is a single contract for life insurance coverage that extends to a group of people. It is typically offered by an employer or another large-scale entity, such as an association or labour organisation, to its workers or members. It is usually free or low-cost coverage based on your annual pay.

Group life insurance is often inexpensive because it is purchased on a wholesale basis, meaning companies can secure lower costs for each individual employee than if they were to purchase an individual policy. The cost of group life insurance will vary based on the specific terms of the policy, such as the length of the policy term and any additional features or riders that are included.

Group life insurance policies are generally cheaper the more people you cover under one policy. For example, MediCompare offers group life insurance starting from £4.99 per month.

Group life insurance is often included as part of a larger employer or membership benefit package. Members of a group life policy do not need to submit to a medical examination and are not subject to individual underwriting. Coverage is normally only valid for as long as a member is part of the group. Once the member leaves, whether through resignation or firing, the coverage ends.

Life Insurance: A Safety Net for Premature Death

You may want to see also

Explore related products

![]()

Who can offer group life insurance?

Group life insurance is offered by an employer or another large-scale entity, such as an association or labour organisation, to its workers or members. It is a single contract for life insurance coverage that extends to a group of people.

By purchasing group life insurance policy coverage through an insurance provider on a wholesale basis for its members, companies are able to secure costs for each individual employee that are much lower than if they were to purchase an individual policy. This means that group life insurance is often free or low-cost for employees, and is a common workplace benefit.

Group life insurance is often part of a larger employer or membership benefit package. It is fairly inexpensive, and may even be free for certain employees. It is also easy to qualify for, as it does not require a medical examination.

Group life insurance policies generally come with certain conditions. Coverage is normally only valid for as long as a member is part of the group. Once the member leaves, whether through resignation or firing, the coverage ends. Employees who elect coverage through the group policy usually receive a certificate of coverage, which is needed to provide to a subsequent insurance company in the event that an individual leaves the company or organisation and terminates their coverage.

Collateral Assignment Life Insurance: Boon for Businesses?

You may want to see also

Explore related products

![]()

Who can receive group life insurance?

Group life insurance is a single contract for life insurance coverage that extends to a group of people. It is offered by an employer or another large-scale entity, such as an association or labour organisation, to its workers or members. It is fairly inexpensive and may even be free for certain employees.

Group life insurance is purchased by an employer or organisation for its staff or members, who retain the master contract. Employees who elect coverage through the group policy usually receive a certificate of coverage, which is needed to provide to a subsequent insurance company if an individual leaves the company or organisation and terminates their coverage.

Group life insurance coverage is normally only valid for as long as a member is part of the group. Once the member leaves, whether through resignation or firing, the coverage ends.

Group life insurance is a common workplace benefit. It typically offers free or low-cost coverage based on your annual pay. You usually lose coverage when you leave your job, so consider buying a policy outside work as well.

Understanding Life Insurance Illustrations: A Beginner's Guide

You may want to see also

Explore related products

![]()

What are the benefits of group life insurance?

Group life insurance is a single contract for life insurance coverage that extends to a group of people. It is usually offered by an employer or another large-scale entity, such as an association or labour organisation, to its workers or members.

The benefits of group life insurance include:

- It is fairly inexpensive and may even be free for certain employees.

- It is easy to qualify for a group policy, with coverage guaranteed to all group members.

- Unlike individual policies, group insurance doesn't require a medical exam.

- It is a good value for money. Group members typically pay very little, if anything at all.

- It is a common workplace benefit, so it is widely available.

- It can be purchased on a wholesale basis, so companies are able to secure lower costs for each individual employee compared to purchasing an individual policy.

Becoming a Life Insurance Agent in Alabama: A Guide

You may want to see also

Explore related products

![DJ&RPPQ Tablet Case Fits 10 inch Tablet 2023,[Sleep/Wake] Also for 10 in Sony Nokia Slim Soft TPU Back Smart Magnetic Stand Protective Cover Cases,Dark Blue](https://m.media-amazon.com/images/I/715WESBYwWL._AC_UY218_.jpg)

![]()

How does group life insurance compare to other types of insurance?

Group life insurance is a single contract for life insurance coverage that extends to a group of people. It is usually offered by an employer or another large-scale entity, such as an association or labour organisation, to its workers or members. It is fairly inexpensive, may even be free for certain employees, and is pretty common nationwide.

Group life insurance is different from other types of insurance in that it is purchased by an employer or organisation for its staff or members, rather than by an individual. This means that group life insurance is often cheaper than individual policies, as companies are able to secure lower costs for each individual employee than if they were to purchase an individual policy.

Another difference is that group life insurance policies generally have certain conditions attached to them. For example, coverage is normally only valid for as long as a member is part of the group. Once the member leaves, whether through resignation or firing, the coverage ends. This is in contrast to whole life insurance, which provides coverage no matter when you die and is permanent. Whole life insurance policies have higher premiums and death benefits and constitute the most popular type of life insurance.

Group life insurance policies also do not require a medical examination, which is often a requirement for individual policies. This makes qualifying for group policies easier, with coverage guaranteed to all group members. Group life insurance is often offered as part of a larger employer or membership benefit package and may have a relatively low coverage amount.

Life Insurance: Visualizing Your Coverage with Diagrams

You may want to see also

Frequently asked questions

Group life insurance is a single contract for life insurance coverage that extends to a group of people. It is offered by an employer or another large-scale entity, such as an association or labour organisation, to its workers or members.

Group life insurance is fairly inexpensive and may even be free for certain employees. It is offered as a piece of a larger employer or membership benefit package.

If you leave your job, you will lose your coverage. However, if you have elected coverage through the group policy, you will receive a certificate of coverage, which you can provide to a subsequent insurance company.