Life insurance and health insurance are two of the most commonly discussed types of insurance. They are both crucial components of a well-rounded financial plan, but they serve different purposes. Life insurance provides security and peace of mind for your family in your absence. It is an income replacement tool, providing a cash sum to your loved ones if you die during the length of the policy. Health insurance, on the other hand, covers your medical affairs, paying for treatment costs such as surgery, prescription drugs, and sometimes dental and vision care.

| Characteristics | Values |

|---|---|

| Purpose | Life insurance provides financial security for families who rely on the policyholder's income. Health insurance covers medical and surgical expenses incurred by the insured. |

| Coverage | Life insurance covers the policyholder's family in their absence. Health insurance covers the policyholder's medical affairs. |

| Benefits | Life insurance provides a death benefit to help maintain the family's standard of living and ensure financial goals. Health insurance reduces the financial burden of medical expenses and ensures access to necessary healthcare services. |

| Tax implications | Tax benefits may be available for both life and health insurance, but this can vary depending on the jurisdiction. |

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

What You'll Learn

- Life insurance provides a cash sum to your loved ones if you die during the length of the policy

- Health insurance is designed to pay for treatment costs, such as urgent surgery or prescription drugs

- Life insurance is not a savings or investment product and has no cash value unless a valid claim is made

- Health insurance can also cover other health-related costs, such as prescription drugs, preventive care, and sometimes dental and vision care

- Life insurance is an income replacement tool for families who rely on the policyholder's income

![]()

Life insurance provides a cash sum to your loved ones if you die during the length of the policy

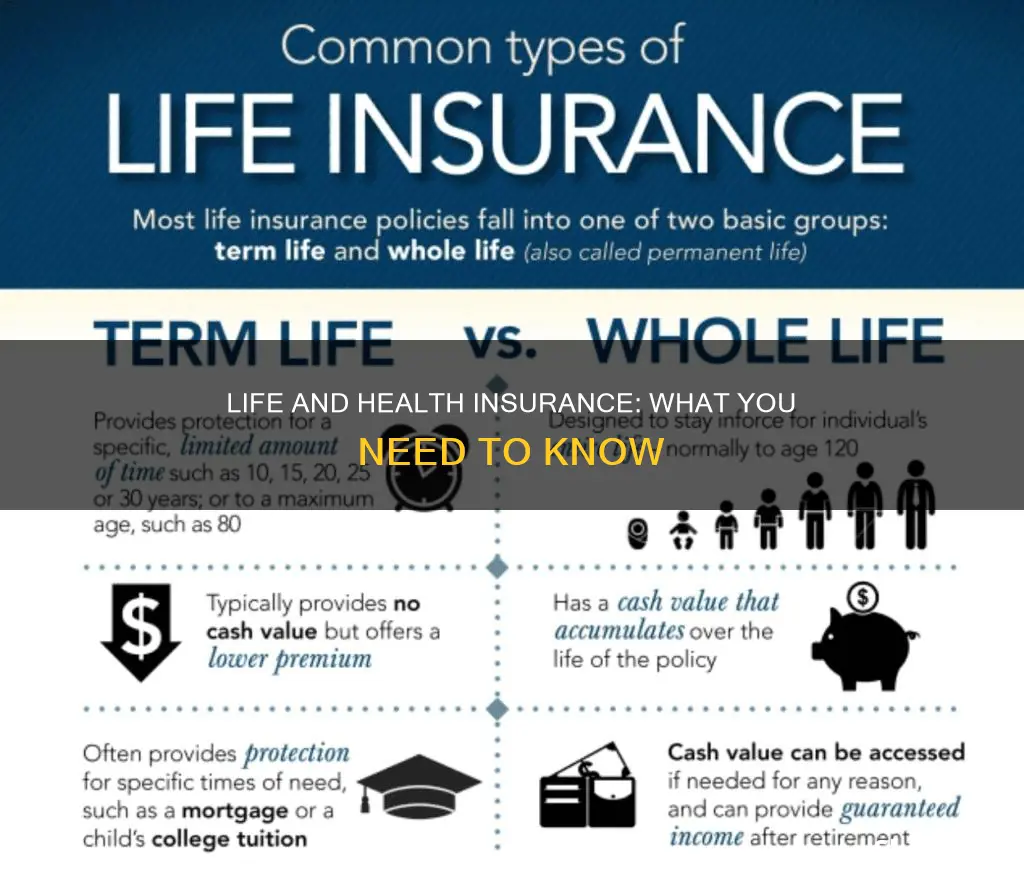

Life insurance and health insurance are often confused, but they are two different things. Life insurance provides a cash sum to your loved ones if you die during the length of the policy. This can be a low-cost plan with terms of 10 to 30 years, or a whole life insurance policy that provides permanent lifetime protection. You can also get universal life insurance, which provides permanent lifetime protection but is adjustable. This means that you can increase or decrease the plan's benefits and premium as your family's needs change.

Term life insurance is a good option for those looking to protect specific short-term financial obligations. For example, you might want to take out a term life insurance policy to cover the cost of your mortgage if you were to die before it was paid off. This would ensure that your loved ones could stay in the family home without the burden of mortgage payments.

Whole life insurance, on the other hand, is a policy that provides permanent lifetime protection and also serves as an investment account. This type of policy earns dividends and can be cashed out. It is a good option for those who want to provide financial security for their loved ones in the event of their death, as well as build wealth over time.

Universal life insurance is similar to whole life insurance in that it provides permanent lifetime protection. However, it offers more flexibility in terms of adjusting the benefits and premiums. This type of policy is often chosen by those who want the security of lifetime protection but also want the option to change their coverage as their needs and circumstances change.

Haven Life Insurance: Ticker Talk and More

You may want to see also

Explore related products

![]()

Health insurance is designed to pay for treatment costs, such as urgent surgery or prescription drugs

Life insurance and health insurance are two of the most commonly discussed and often confused types of insurance. While both are crucial components of a well-rounded financial plan, they serve different purposes. Life insurance is a financial product designed to provide security and peace of mind for your family in the event of your death. It is an agreement between an individual (the policyholder) and an insurance company, whereby the policyholder makes regular premium payments and, in exchange, the insurance company promises to pay a designated beneficiary a sum upon the insured person's death. This payment, often called the death benefit, can help replace lost income, cover various expenses, provide financial support, and ensure the well-being of loved ones. It can be used to fund children's education, save for retirement, or pay the mortgage.

On the other hand, health insurance is a type of insurance coverage that pays for medical and surgical expenses incurred by the insured. It can cover urgent surgery, prescription drugs, preventive care, and sometimes dental and vision care. Health insurance can provide a critical safety net by reducing the financial burden of medical expenses and ensuring access to necessary healthcare services. It is designed to pay for treatment costs while you are alive, and it can help you see a doctor more quickly.

While life insurance provides financial protection for your family in the event of your death, health insurance covers your medical expenses and ensures access to healthcare services. Both types of insurance are important to have, as they serve different but essential purposes. By understanding the differences between life and health insurance, you can make informed decisions about your financial planning and ensure that you and your loved ones are protected.

Does Life Insurance Blood Test Detect Cancer?

You may want to see also

Explore related products

![Life and Health Insurance License Exam Secrets Study Guide - Full-Length Practice Test, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71PdYCnP8ML._AC_UY218_.jpg)

![]()

Life insurance is not a savings or investment product and has no cash value unless a valid claim is made

Life insurance is a type of insurance that provides financial protection in the event of the insured person's death. It is designed to help cover the costs associated with death, such as funeral expenses, outstanding debts, and providing financial support for dependents.

While life insurance can provide peace of mind and financial security for loved ones, it is important to understand that it is not a savings or investment vehicle. The primary purpose of life insurance is to protect against the financial risks associated with death, not to accumulate wealth.

There are different types of life insurance policies available, such as term life insurance, whole life insurance, and universal life insurance. Term life insurance provides coverage for a specific period, usually between 10 and 30 years. Whole life insurance, on the other hand, offers permanent lifetime protection and can also serve as an investment account that earns dividends and can be cashed out. Universal life insurance is also a form of permanent lifetime protection but offers more flexibility in terms of adjusting the benefits and premiums as needed.

While some life insurance policies, such as whole life insurance, may offer investment-like features, it is important to remember that the primary purpose of life insurance is risk protection, not wealth accumulation. Therefore, when considering life insurance, it is essential to understand the specific terms and conditions of the policy, including any potential cash value or investment returns, to ensure it meets your individual needs and expectations.

Who Gets Your Life Insurance: Contingent Beneficiary Basics

You may want to see also

Explore related products

![]()

Health insurance can also cover other health-related costs, such as prescription drugs, preventive care, and sometimes dental and vision care

A and H Insurance provides an array of insurance plans, benefits, and products for employer groups, individuals, and families. They offer term life insurance, whole life insurance, and universal life insurance. Term life insurance is a low-cost plan with terms of 10 to 30 years, which is great for those looking to protect specific short-term financial obligations. Whole life insurance provides permanent lifetime protection and also serves as an investment account that earns dividends and can be cashed out. Universal life insurance provides permanent lifetime protection but is adjustable.

The flexibility of A and H Insurance plans means that you can increase or decrease the benefits and premiums as your family's needs change. This allows you to customise your coverage to ensure that you have the protection you need at a price that fits your budget. You may even be able to skip some payments by using the plan's built-up cash value to pay.

Life Insurance, Suboxone, and You: What to Expect

You may want to see also

Explore related products

$82.51 $92.95

![]()

Life insurance is an income replacement tool for families who rely on the policyholder's income

Term life insurance, for example, offers coverage for a specified term, typically ranging from 10 to 30 years. This type of policy is ideal for those seeking to safeguard short-term financial commitments. On the other hand, whole life insurance provides permanent lifetime protection and also functions as an investment account that accumulates dividends and can be cashed out. Universal life insurance is another option that offers permanent coverage but with the added flexibility of adjustability.

The primary purpose of life insurance is to ensure that your family's financial needs are met even after you're gone. It provides a safety net, allowing your dependents to maintain their standard of living and cover essential expenses such as mortgage payments, education costs, or daily living expenses. By purchasing a life insurance policy, you can have peace of mind knowing that your family will be taken care of financially.

Additionally, life insurance can also serve as a valuable investment vehicle. Whole life insurance policies, for instance, build cash value over time, which can be borrowed against or withdrawn to meet future financial needs. This feature adds an extra layer of financial security, providing funds for retirement, education, or other significant expenses.

It's important to note that life insurance should not be confused with health insurance. While both types of insurance are essential components of a comprehensive financial plan, they serve different purposes. Health insurance focuses on covering medical expenses, while life insurance provides financial protection for your loved ones upon your death.

Client ID in IDBI Federal Life Insurance: What's the Significance?

You may want to see also

Frequently asked questions

Life insurance is a financial product designed to provide security and peace of mind for your family in the event of your death. It is an agreement between an individual (the policyholder) and an insurance company. In exchange for regular premium payments, the insurance company promises to pay a designated beneficiary a sum upon the insured person’s death. This payment, often called the death benefit, can help cover various expenses, provide financial support, and ensure the well-being of loved ones left behind.

Health insurance is a type of insurance coverage that pays for medical and surgical expenses incurred by the insured. It can also cover other health-related costs, such as prescription drugs, preventive care, and sometimes dental and vision care. Health insurance can provide a critical safety net by reducing the financial burden of medical expenses and ensuring access to necessary healthcare services.

Life and health insurance are crucial components of a well-rounded financial plan. While life insurance provides financial security for your family in the event of your death, health insurance covers your medical expenses while you are alive. Both types of insurance are essential to ensuring peace of mind and protecting yourself and your loved ones.