Term life insurance provides coverage for a set period of time, usually 10-30 years, and is more affordable than whole life insurance. Whole life insurance offers lifelong coverage and includes an investment component that grows over time, but it is significantly more expensive. Adjustable life insurance is a hybrid of term and whole life insurance that allows policyholders to adjust features such as the period of protection and the premium paid.

| Characteristics | Term Life Insurance | Complife |

|---|---|---|

| Coverage | Temporary, for a set period of time (usually 10-30 years) | Permanent |

| Cost | Cheaper | More expensive |

| Cash value | No | Yes |

| Premium | Fixed | Adjustable |

Explore related products

What You'll Learn

![]()

Term life insurance is more affordable than whole life insurance

Adjustable life insurance, a hybrid of term and whole life insurance, allows policyholders to adjust features such as the period of protection and the premium paid. However, the initial premium for adjustable life insurance is lower than for an equivalent amount of term insurance. This means that, despite the flexibility it offers, adjustable life insurance is still more expensive than term life insurance.

Gerber Life Insurance: Is It a Good Adult Option?

You may want to see also

Explore related products

![]()

Whole life insurance offers lifelong coverage

Whole life insurance is a good option for those who want the security of lifelong coverage and the ability to build wealth through their policy. The investment component of whole life insurance means that the policy can grow in value over time, providing additional financial benefits. This can be especially useful for retirement planning or for covering unexpected expenses.

However, it is important to note that whole life insurance policies are significantly more expensive than term life insurance. The higher cost is due to the lifelong coverage and the investment component, which allows the policy to accumulate cash value. While whole life insurance offers more comprehensive coverage, it may not be feasible for those on a tight budget.

Additionally, whole life insurance policies typically do not allow for adjustments to the premiums or death benefit. This means that once the policy is in place, the premiums must be paid consistently to maintain coverage. This can be a challenge if one's financial situation changes unexpectedly.

Overall, whole life insurance offers the advantage of lifelong coverage, investment growth potential, and the ability to build retirement wealth. However, it comes at a higher cost and may require careful financial planning to sustain the premiums over the long term.

Borrowing Against Life Insurance: What You Need to Know

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Term life insurance does not accumulate cash value

Term life insurance provides coverage for a predetermined period, usually 10-30 years, after which few people still need insurance coverage. The coverage can often be renewed, but only up to a specific age, and premiums will generally increase with each renewal. Term life insurance is ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage.

Whole life insurance, on the other hand, offers permanent coverage and a cash value. You can't change your whole life premiums or death benefit, which can make it harder to maintain a whole life insurance policy, especially if you're on a budget.

Adjustable life insurance is a hybrid of term life and whole life insurance that allows policyholders to adjust certain features, such as the period of protection and the premium amount. While the initial premium for adjustable life insurance is lower than for an equivalent amount of term insurance, coverage for life is subject to premium increases.

Understanding ADA and Taxable Income from Principal Life Insurance

You may want to see also

Explore related products

![]()

Whole life insurance includes an investment component

Whole life insurance is significantly more expensive than term life insurance, as it offers lifelong coverage. However, the initial premium for whole life insurance is lower than for an equivalent amount of term insurance. This is because term life insurance policies only offer coverage for a set period, usually 10-30 years, after which few people still need insurance coverage. Whole life insurance policies are also more difficult to maintain, especially if you're on a budget, as the premiums cannot be changed.

Life Insurance: Your Personal Asset and Financial Security

You may want to see also

Explore related products

![]()

Whole life insurance is better for those who want coverage for life

However, it is important to note that whole life insurance is significantly more expensive than term life insurance. Term life insurance is ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage. It is more affordable and can be renewed, but it does not accumulate cash value, meaning you cannot withdraw or borrow against the policy while you are alive.

Adjustable life insurance is a hybrid of term life and whole life insurance that allows policyholders to adjust certain features, such as the period of protection and the premium amount. While this can provide more flexibility, it is important to consider that coverage for life is subject to premium increases.

Cancer and Term Life Insurance: Does Level Death Benefit?

You may want to see also

Frequently asked questions

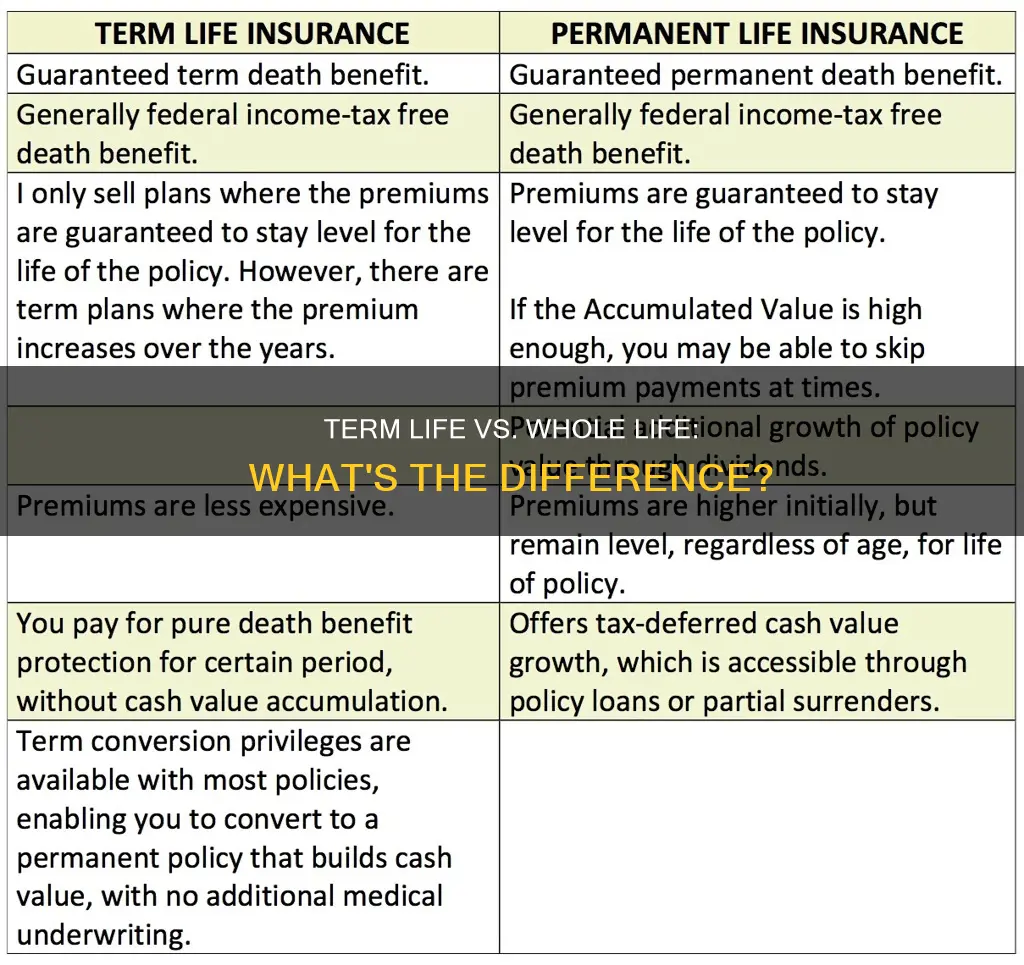

Term life insurance is cheaper and covers you for a set period of time, while whole life insurance (complife) lasts your entire life and can be more expensive. Term life insurance provides a cash benefit to the policyholder, while whole life insurance provides a death benefit to the beneficiary. Term life insurance does not accumulate cash value, meaning you can't withdraw or borrow against the policy while you're alive. Whole life insurance, on the other hand, can build cash value that you can borrow against.

Term life insurance is more affordable than whole life insurance. It also provides coverage for a predetermined period, making it ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage. Term policies are also customised to your needs and can help your family financially should you pass away while the policy is in force.

Whole life insurance offers lifelong coverage as long as you continue paying your premiums. It includes an investment component that grows over time, allowing you to build retirement wealth and income through the policy's cash value account. Whole life insurance also provides flexibility in terms of death benefits and allows policyholders to custom design certain aspects.

No, term life insurance does not accumulate cash value, so you cannot withdraw or borrow against the policy while you are alive. Whole life insurance, on the other hand, can build cash value that you can borrow against, but this makes it a more complex and expensive product.