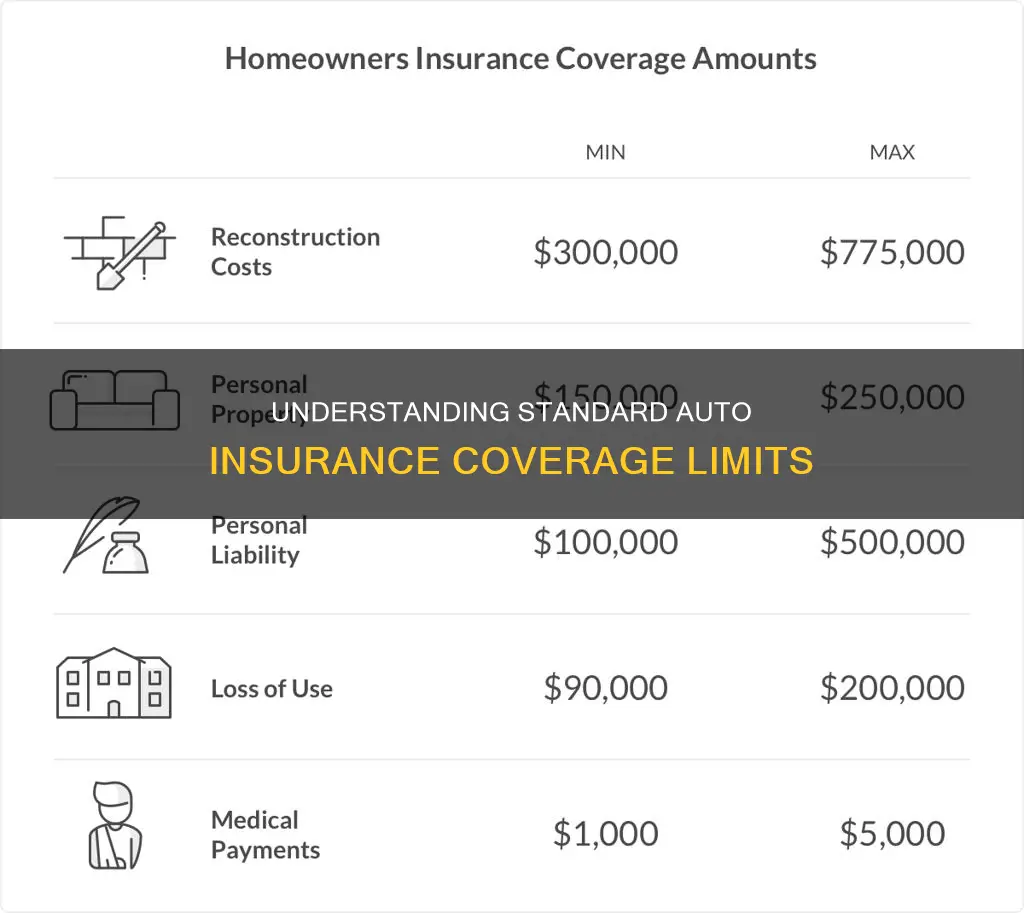

Auto insurance coverage limits refer to the maximum amount that an insurance company will pay out for a claim. In the US, auto liability coverage is the only type of auto insurance that is legally required in every state. This coverage includes property damage and medical expenses for the other driver and their passengers if you are at fault in an accident. The minimum coverage requirements vary by state, for example, in Texas, the minimum coverage is $30,000 of coverage for injuries per person, up to a total of $60,000 per accident, and $25,000 of coverage for property damage, also known as 30/60/25 coverage.

| Characteristics | Values |

|---|---|

| Coverage limits | The maximum amount an insurer may pay following a covered loss |

| Liability coverage | Required by law in every state; covers property damage, medical expenses, and other damages to another person and their vehicle |

| Bodily injury coverage | Covers medical expenses, lost wages, compensation for pain, etc. for the other driver and their passengers |

| Property damage coverage | Covers damages to the claimant's property |

| Uninsured motorist coverage | Covers injuries and damages incurred from an accident caused by an uninsured motorist |

| Collision coverage | Optional coverage that provides coverage for damage caused by a collision with another vehicle or object |

| Comprehensive coverage | Optional coverage that provides coverage for damage to your vehicle not caused by a collision, such as theft, animal strike, vandalism, fire, etc. |

| Medical payments coverage | Covers medical bills for you and your passengers |

| Personal injury protection (PIP) coverage | Covers medical bills, lost wages, and other non-medical costs for you and your passengers |

| Uninsured/underinsured motorist coverage | Covers damages if you're hit by an uninsured driver or a driver without adequate coverage |

| Towing and labor coverage | Covers towing and labor costs if your car can't be driven |

| Rental reimbursement coverage | Covers rental car or ride-sharing services if your car is stolen or being repaired |

Explore related products

What You'll Learn

![]()

Liability coverage

Property Damage Liability Coverage

This aspect of liability insurance covers the costs of repairing or replacing the other driver's vehicle and other damaged property, such as fences, structures, or personal belongings inside their car. It also includes legal fees if you are sued for property damage. Essentially, it insures you against accidental damage to another person's property caused by your vehicle.

Bodily Injury Liability Coverage

Bodily injury liability coverage takes care of the medical expenses of the other party if you are responsible for the accident. It may also cover lost wages and legal fees if the injured party decides to take legal action. This type of coverage ensures that the other person's injuries sustained in the accident are financially taken care of.

Understanding Coverage Limits

It's important to note that the required minimum liability limits vary from state to state. While most states mandate liability insurance, the specific coverage types and amounts can differ. Therefore, it's crucial to check the requirements of your state to ensure you have the appropriate coverage.

When deciding on your liability coverage limits, consider the potential costs of an accident. Opting for higher coverage limits provides better protection, but it also increases your insurance rate. Choosing the right coverage limits is crucial to safeguarding your financial security in the event of a car accident.

Vehicle Impound: No Insurance, Now What?

You may want to see also

Explore related products

![]()

Collision coverage

Collision insurance can provide financial peace of mind in the event of an accident, regardless of who is at fault. It covers a wide range of collision scenarios, including rear-ending another vehicle, collisions with stationary objects like trees, and even if your car flips over. This coverage can also extend to situations where a friend or family member is driving your car with your permission and gets into an accident.

When deciding whether to opt for collision coverage, it's important to consider the age and value of your car. For older vehicles with lower values, the cost of collision coverage may outweigh the benefits. As a general rule of thumb, if the cost of collision coverage is more than 10% of your car's actual cash value, it might not be a worthwhile investment. However, for newer or more expensive cars, collision coverage can provide valuable protection.

Another factor to consider is your financial situation. In the event of an accident, could you afford to repair or replace your car without insurance? Collision coverage can help you get back on the road without incurring a sudden large expense. It's worth noting that collision coverage typically comes with a deductible, which is the amount you have to pay before the insurance company covers the rest. A higher deductible can lower your monthly premium, but it also means you'll have to pay more out of pocket if an accident occurs.

Ultimately, collision coverage is a valuable addition to your auto insurance policy if you want the peace of mind of knowing that your vehicle is protected in the event of a collision, regardless of fault. It's important to weigh the costs and benefits based on your car's value and your financial situation to make an informed decision.

Insurance Drop: When You're Not Covered

You may want to see also

Explore related products

![]()

Comprehensive coverage

- Weather conditions like wind damage from hurricanes, floods, hail, and falling objects

- Fires and explosions

- Total or partial car theft and vandalism

- Hitting or being hit by a deer or other animal

- Violence from civil unrest or riots

- Glass claims and windshield repair

When deciding whether to purchase comprehensive coverage, consider the value of your car, whether you live in an area prone to weather-related disasters or car theft, and how much you can afford to pay out of pocket for repairs or replacement.

Auto Insurance Deductibles: Rising Costs?

You may want to see also

Explore related products

![]()

Medical payments coverage

The cost of Medical Payments Coverage varies, but it is generally inexpensive, with many policyholders adding coverage for $5 to $8 per month. The cost increases with higher coverage limits. When deciding on the amount of Medical Payments Coverage to purchase, it is essential to consider your specific financial situation, the existence of other insurance for medical expenses, and whether you have a high-deductible health insurance plan.

While Medical Payments Coverage is not mandatory in most states, it can provide financial peace of mind in the event of an accident. It is worth considering, especially if you have a high-deductible health insurance plan or want additional coverage for medical expenses related to automobile accidents.

Selling Auto Insurance in Texas: Strategies for Success

You may want to see also

Explore related products

![]()

Personal injury protection

In Texas, for example, insurance companies are required to offer every driver at least $2,500 of PIP insurance, with the option to increase coverage to $5,000 or $10,000 for additional financial protection. While PIP insurance is not mandatory in Texas, you must sign a waiver if you want to decline the coverage.

It's important to note that PIP has certain limitations. It won't cover the other drivers' injuries in a collision, any injuries from an accident while committing a crime, or injuries sustained while being paid for driving.

When considering auto insurance, it's essential to review the specific requirements and options available in your state, as they can vary significantly across the United States.

Michigan Auto Insurance: Country's Highest Rates?

You may want to see also

Frequently asked questions

Auto insurance financially protects you by paying the other driver’s car repair and medical bills if you cause an accident. Depending on the type of coverage you have, it can also pay to repair or replace your car if it’s damaged or stolen.

Insurance limits, or coverage limits, refer to the maximum amount of money your auto insurance policy will pay following a covered loss. Once that limit is reached, you will be responsible for paying any additional costs out of pocket.

The typical coverage limits for auto insurance, also known as liability coverage limits, are usually written out in three numbers, such as 100/300/50. This means you have a $100,000 limit per person for bodily injury in an accident, a $300,000 total limit per accident for bodily injury, and a $50,000 limit per accident for property damage.

When choosing your coverage limits, it is important to consider your financial situation and how much you could afford to pay out of pocket in the event of an accident. Additionally, review your policy regularly to ensure that you are comfortable with the limits you have selected.