Life insurance is a crucial aspect of financial planning, providing peace of mind and security for loved ones. For those serving in the military, including the Marines, there are unique life insurance options tailored to their needs and the nature of their service. These insurance plans are designed to offer financial protection and support for families, ensuring their well-being in the event of a marine's death or injury. This raises important questions: What life insurance options are available specifically for Marines? How do these policies work, and what benefits do they provide? Understanding these insurance plans is essential for Marines and their families to make informed decisions and navigate the financial complexities that come with serving in the military.

| Characteristics | Values |

|---|---|

| Name of Insurance | Servicemembers' Group Life Insurance (SGLI) |

| Who is it for? | Active-duty members of the Army, Navy, Air Force, Space Force, Marines, Coast Guard, Commissioned members of the National Oceanic and Atmospheric Administration (NOAA), the U.S. Public Health Service (USPHS), Cadets or midshipmen of the U.S. military academies, Members, cadets or midshipmen of the Reserve Officers Training Corps (ROTC), Members of the Ready Reserve or National Guard, Part-time Reserve members |

| Cost | Low-cost term coverage with a monthly premium of 6 cents per $1,000 of insurance coverage. Traumatic Injury Protection coverage (TSGLI) is an additional $1 per month |

| Coverage | Coverage can be chosen by the service member and beneficiaries can be chosen and changed as needed |

| Post-discharge | Veterans' Group Life Insurance (VGLI) can be applied for within 1 year and 120 days of discharge. SGLI coverage can be converted to a permanent, individual insurance policy within 120 days of discharge without proof of good health |

| Terminal Illness | An advance insurance payment can be requested for a service member who is terminally ill |

Explore related products

What You'll Learn

![]()

Servicemembers' Group Life Insurance (SGLI)

To qualify for SGLI coverage, you must meet the qualifications under at least one of the following categories:

- Active-duty members of the Army, Navy, Air Force, Space Force, Marines, or Coast Guard

- Commissioned members of the National Oceanic and Atmospheric Administration (NOAA) or the U.S. Public Health Service (USPHS)

- Cadets or midshipmen of the U.S. military academies

- Members, cadets, or midshipmen of the Reserve Officers Training Corps (ROTC) engaged in authorized training and practice cruises

- Members of the Ready Reserve or National Guard, assigned to a unit, and scheduled to perform at least 12 periods of inactive training per year

If you are a Reserve member who does not qualify for full-time coverage, you may still be eligible for part-time SGLI coverage. You can choose your level of coverage or even refuse coverage completely. You can also choose your beneficiaries (the people who will receive the money from your life insurance policy if you die) and change them as needed.

If you have SGLI coverage, you will pay a monthly premium that will be automatically deducted from your base pay. The current basic SGLI premium rate is 6 cents per $1,000 of insurance coverage, with an additional $1 per month for Traumatic Injury Protection coverage (TSGLI).

When you leave the military, you have the option to convert your SGLI coverage to a permanent, individual insurance policy within 120 days of your discharge date without proof of good health. You may also be eligible to apply for Veterans' Group Life Insurance (VGLI) within one year and 120 days from your date of discharge, for up to the amount of coverage you had through SGLI. Additionally, service members who are totally disabled at the time of discharge may qualify for a Servicemembers' Group Life Insurance Disability Extension, which allows them to keep their SGLI coverage for up to two years after discharge at no additional cost.

Life Insurance vs Assurance: What's the Real Difference?

You may want to see also

Explore related products

![]()

SGLI coverage costs

Servicemembers' Group Life Insurance (SGLI) offers low-cost term coverage to eligible service members. If you are a service member who meets certain criteria, you will be automatically signed up for SGLI.

If you have SGLI coverage, you will pay a monthly premium that will be automatically taken out of your base pay. The current basic SGLI premium rate is 6 cents per $1,000 of insurance coverage. This premium includes an additional $1 per month for Traumatic Injury Protection coverage (TSGLI). For example, the new coverage amounts will be $450,000 for $27 a month and $500,000 for $30 a month. TSGLI coverage is automatic with SGLI coverage, adding $1 to the above premium amounts.

When you leave the military, you can apply for Veterans' Group Life Insurance (VGLI) within 1 year and 120 days from your date of discharge for up to the amount of coverage you had through SGLI. If you pay the VGLI premium, you will be able to keep your life insurance coverage for as long as you keep paying the premiums. You also have the option to convert your SGLI coverage to a permanent, individual insurance policy within 120 days from your date of discharge without proof of good health. You may be able to keep your coverage for up to 2 years after the date you leave the military at no cost to you if you meet certain requirements.

Colonial Penn Life Insurance: Is It Rated Well?

You may want to see also

Explore related products

![SUPCASE for Samsung Galaxy Z Fold 7 Case with Kickstand (UB Pro), [Built-in Tempered Glass Screen Protector] [Hinge Coverage] [Military-Grade Protection] Full-Body Heavy-Duty Rugged Phone Case, Guldan](https://m.media-amazon.com/images/I/7138LUR30RL._AC_UY218_.jpg)

![SUPCASE for Samsung Galaxy Z Fold 7 Case with Kickstand (UB Grip), [Compatible with MagSafe] [Built-in Privacy Screen Protector] [Hinge Coverage] Military-Grade Protection Phone Case, Dark](https://m.media-amazon.com/images/I/71AFEVzsaQL._AC_UY218_.jpg)

![]()

Eligibility for SGLI

Servicemembers' Group Life Insurance (SGLI) is a low-cost term insurance option for eligible service members. If you are a service member who meets the criteria, you will be automatically signed up for SGLI.

To be eligible for full-time SGLI coverage, you must meet at least one of the following requirements:

- You are an active-duty member of the Army, Navy, Air Force, Space Force, Marines, or Coast Guard.

- You are a commissioned member of the National Oceanic and Atmospheric Administration (NOAA) or the U.S. Public Health Service (USPHS).

- You are a cadet or midshipman of the U.S. military academies.

- You are a member, cadet, or midshipman of the Reserve Officers Training Corps (ROTC) and are engaged in authorized training and practice cruises.

- You are a member of the Ready Reserve or National Guard, assigned to a unit, and are scheduled to perform at least 12 periods of inactive training per year.

- You are a volunteer in the Individual Ready Reserve (IRR) mobilization category.

If you are a Reserve member who does not qualify for full-time coverage, you may still be eligible for part-time coverage. In this case, you will be automatically signed up through your service branch, and you can check with your unit's personnel office for more information.

It is important to note that you can choose your level of coverage or even refuse coverage completely. Additionally, you have the option to choose your beneficiaries (the individuals who will receive the money from your life insurance policy in the event of your death) and change them as needed. You can submit any changes or updates online through the SGLI Online Enrollment System (SOES).

To receive more specific information about your eligibility for SGLI, you can contact the Office of Servicemembers' Group Life Insurance (OSGLI) by calling 800-419-1473 or emailing the Prudential Insurance Company.

Cashing in on Gerber Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![SUPCASE for Samsung Galaxy Z Fold 7 Case with Kickstand (UB Pro), [Built-in Tempered Glass Screen Protector] [Hinge Coverage] [Military-Grade Protection] Full-Body Heavy-Duty Rugged Phone Case, Ruddy](https://m.media-amazon.com/images/I/71XGCOGE+DL._AC_UY218_.jpg)

![]()

SGLI beneficiaries

Servicemembers' Group Life Insurance (SGLI) is a low-cost term insurance coverage option for eligible service members. If a service member meets the criteria, they are automatically signed up for SGLI.

Service members with full-time SGLI coverage can manage their SGLI coverage and beneficiary information using SOES. They can make changes to their life insurance coverage and beneficiary information at any time without completing a paper form or visiting their personnel office. To access SOES, service members can sign in at www.dmdc.osd.mil/milconnect and go to the Benefits Tab, Life Insurance SOES- SGLI Online Enrollment System.

For service members with part-time SGLI coverage, the SGLV 8286 form must be used to make changes to SGLI coverage and beneficiary information. The completed form should be submitted to the service member's branch of service personnel office. It's important to note that while service members can name anyone as their SGLI beneficiary without their consent, the spouse will be notified if a beneficiary other than the spouse is named.

Key Man Life Insurance: Protecting Your Business's Future

You may want to see also

Explore related products

![Spigen Liquid Air Designed for iPhone 16 Pro Case [Camera Control Button Coverage] [Military-Grade Protection] Compatible with MagSafe- Matte Black](https://m.media-amazon.com/images/I/71YWOg9OzVL._AC_UY218_.jpg)

![]()

Veterans' Group Life Insurance (VGLI)

Veterans Group Life Insurance (VGLI) is a life insurance program that allows service members to convert their Servicemembers' Group Life Insurance (SGLI) coverage to term life insurance that is renewable every five years. It was established as part of the Veterans' Insurance Act of 1974, which aimed to provide continued life insurance protection to veterans transitioning back to civilian life. Before VGLI, veterans often found it challenging to obtain life insurance due to health issues or the high cost of individual policies.

VGLI is administered by the Office of Servicemembers' Group Life Insurance (OSGLI), a division of the Prudential Insurance Company of America, under the oversight of the Department of Veterans Affairs (VA). Members with full-time SGLI coverage are eligible for VGLI when they leave the service. VGLI coverage is issued in multiples of $10,000 up to a maximum of $500,000. However, a service member's VGLI coverage amount cannot exceed the SGLI coverage they had when they left the service.

To be eligible for VGLI, one must have had SGLI coverage while in the military and be able to convert their coverage to VGLI upon separation from service. VGLI offers guaranteed acceptance within 240 days of separation, making it a viable option for veterans with medical issues or those seeking straightforward, renewable term insurance.

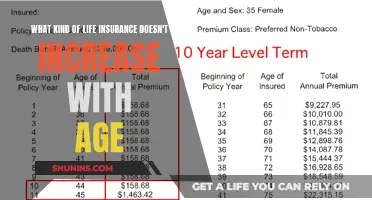

VGLI premiums are calculated based on the age of the insured veteran, with rates increasing in five-year age bands. As veterans age, the risk associated with providing life insurance coverage rises, leading to higher premium costs. This means that while younger veterans may initially benefit from relatively low premiums, the cost of maintaining VGLI coverage can become significantly higher over time. Therefore, it is important to assess your financial goals and compare the specifics of VGLI with alternative military life insurance policies to determine the best option for your needs.

Pension Retiree Life Insurance: Can You Expect an Increase?

You may want to see also

Frequently asked questions

Servicemembers' Group Life Insurance (SGLI) offers low-cost term coverage to eligible service members. If you’re a service member who meets certain criteria, you'll be automatically signed up.

You may be eligible for full-time SGLI coverage if you meet at least one of these requirements: You’re an active-duty member of the Army, Navy, Air Force, Space Force, Marines, or Coast Guard; You’re a commissioned member of the National Oceanic and Atmospheric Administration (NOAA) or the U.S. Public Health Service (USPHS); You’re a cadet or midshipman of the U.S. military academies; You’re a member, cadet, or midshipman of the Reserve Officers Training Corps (ROTC) engaged in authorized training and practice cruises; or You’re a member of the Ready Reserve or National Guard, assigned to a unit, and scheduled to perform at least 12 periods of inactive training per year.

If you have SGLI coverage, you’ll pay a monthly premium that’ll be automatically taken out of your base pay. The current basic SGLI premium rate is 6 cents per $1,000 of insurance coverage. The premium includes an additional $1 per month for Traumatic Injury Protection coverage (TSGLI).

If you qualify for SGLI, you will be automatically signed up through your service branch. Check your unit’s personnel office for more information.

Yes, you can choose your beneficiaries (the people you pick to get the money from your life insurance policy if you die) and change them as needed. Submit your changes online through the SGLI Online Enrollment System (SOES).