There are a few things to consider when it comes to insurance policies for two people who die at the same time. Firstly, it's important to differentiate between health insurance and life insurance. While it is possible to have multiple health insurance plans, the primary and secondary insurance designations will determine which plan is activated first and how much coverage you will receive. On the other hand, life insurance policies are typically designed to replace the income of the deceased and provide financial support to their beneficiaries. In the case of two people dying simultaneously, their respective beneficiaries would usually receive the death benefit outlined in their individual policies.

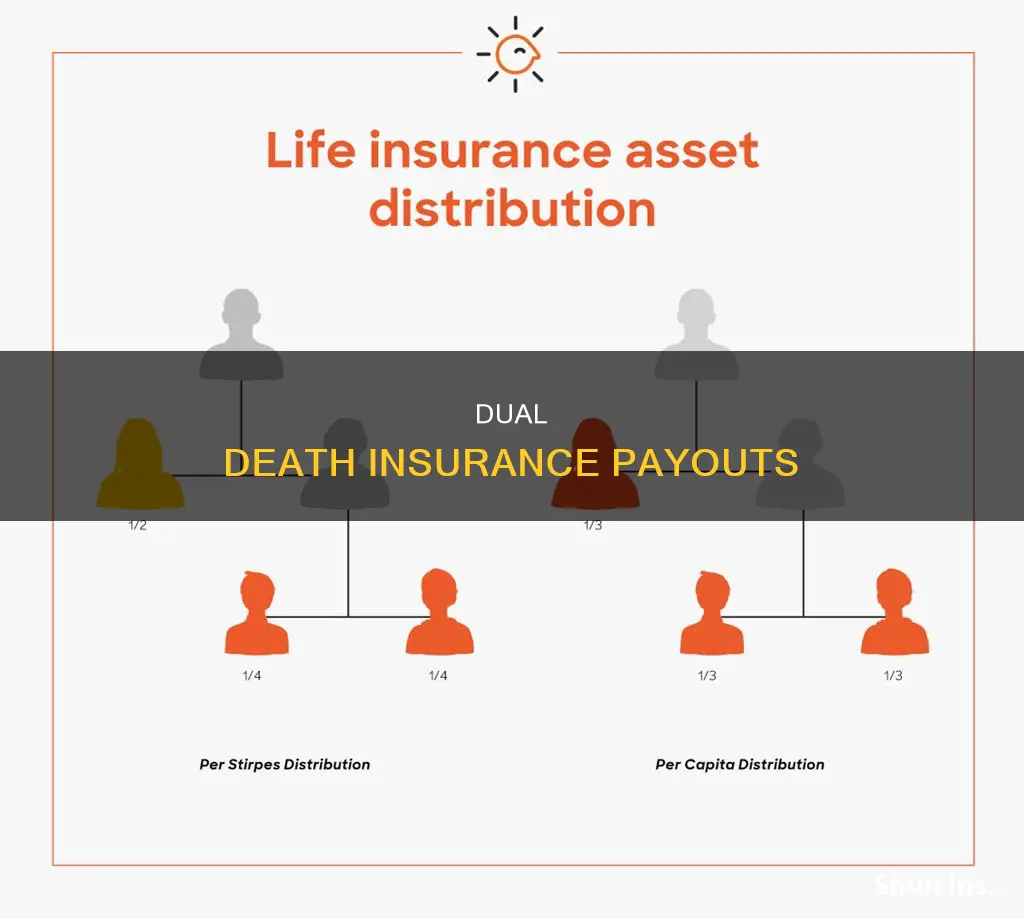

It is possible to have multiple life insurance policies, and this may be beneficial in certain situations. For example, if someone purchases a $250,000 term life policy at 30 and decides at 40 that they need more coverage, they can buy a second policy to close any financial gaps. Additionally, some couples opt for second-to-die insurance, which provides benefits to beneficiaries only after the last surviving person on the policy dies. This type of insurance is often used for estate planning and can be more affordable than individual plans.

However, it's important to weigh the pros and cons of multiple policies, as there may be limitations on the total amount of coverage allowed, and the cost of multiple premiums can add up. Ultimately, the decision to purchase additional insurance depends on individual circumstances, preferences, and financial needs.

| Characteristics | Values |

|---|---|

| Type of insurance | Second-to-die insurance, also known as survivorship policies, dual-life insurance, and joint-life insurance |

| Who is it for? | Usually married couples, but can be for any two people |

| When does it pay out? | Only after the last surviving person on the policy dies |

| Who does it pay out to? | The beneficiaries of the policy |

| What is it used for? | Estate planning, e.g. to fund an irrevocable life insurance trust (ILIT) or to pass benefits to children or grandchildren |

| How does it differ from regular life insurance? | The surviving partner doesn't receive any benefits after the other person dies |

| Is it more or less expensive than individual plans? | It may be less expensive |

| Are qualifications for survivorship policies more or less stringent than for individual plans? | They may be less stringent |

| What is the death benefit used for? | To offset estate-settlement costs and ensure beneficiaries can afford estate transfers of assets |

Explore related products

What You'll Learn

- Second-to-die insurance is a type of life insurance for two people that provides benefits to beneficiaries after the last surviving person on the policy dies

- You can have multiple life insurance policies on one person

- Primary and secondary health insurance rules

- Pros and cons of having multiple health insurance plans

- You can have more than one income protection insurance policy

![]()

Second-to-die insurance is a type of life insurance for two people that provides benefits to beneficiaries after the last surviving person on the policy dies

Second-to-die insurance is a type of life insurance policy that covers two people, usually a married couple, and pays out only after the second person dies. This type of insurance is often used for estate planning, where it can help fund an irrevocable life insurance trust (ILIT) or pass on death benefits to children or grandchildren. It is also known as survivorship insurance or dual-life insurance.

Second-to-die insurance policies are typically less expensive than individual plans because they are based on the joint life expectancy of the insured parties and only pay out after both have died. This type of insurance may also have less stringent qualification requirements, making it a good option for couples where one partner has health issues.

The death benefit from a second-to-die insurance policy can be used to pay estate taxes and other settlement costs, ensuring that beneficiaries can afford to keep assets like a family vacation home instead of having to sell it to pay taxes. The benefit can also be used to provide financial support for surviving children or grandchildren, especially those with special needs.

In addition to estate planning, second-to-die insurance can be used to address specific situations, such as providing financial support for a disabled child or giving spouses with medical conditions better coverage options. It can also be a tool for strategic wealth transfer within families, helping to create generational wealth.

While second-to-die insurance policies are commonly used by wealthier families to reduce estate tax exposure, they can also be beneficial for retirees of lesser means who wish to leave a financial legacy for their heirs. By purchasing a survivorship whole life policy, they can guarantee that their children will receive a tax-free death benefit while also having the financial freedom to spend their savings on travel or future medical expenses.

Insurance Buying: Key Considerations

You may want to see also

Explore related products

![Joint Hearing of Special Insurance Investigation [of Senate] and Assembly Insurance Committee on Proposed Legislation Arising out of the Insurance Investigation of 1905-1906](https://m.media-amazon.com/images/I/61jiDmuIosL._AC_UY218_.jpg)

![]()

You can have multiple life insurance policies on one person

While one life insurance policy is often sufficient, it is possible to have multiple policies on one person. This is referred to as "laddering" and is useful if you have different coverage goals. For example, you might want to cover your income, mortgage payments, and your children's college debt. In this case, you could buy three term policies of different lengths and amounts to match each need.

There are no legal limits to how many life insurance policies you can own, but there are limits to the benefits you can receive. These are typically set at 20 to 30 times your annual income. This is because life insurance is designed to replace your earning power, not to increase the wealth of your beneficiaries.

There are several reasons why you might want to have more than one life insurance policy:

- To have an individual policy in addition to group coverage: Supplemental life insurance offered through an employer can be low-cost or free. However, you may not be able to keep this if you leave your job, so it's a good idea to have an individual policy as well.

- To meet different financial goals: Term life insurance is great for basic income replacement, while the cash value of a permanent policy can help with retirement planning.

- To create an insurance ladder: Rather than buying one large policy, you can use a strategy called life insurance laddering to build coverage with multiple policies in different amounts.

- To respond to changes in your financial obligations: You might need to buy additional life insurance if your financial situation changes, such as having another child or starting a business.

- To add long-term care coverage: As you get older, you might want to buy additional life insurance to help cover the cost of long-term care.

If you're considering buying additional coverage, it's important to understand the limits on the amount of life insurance you can have. These limits are typically tied to your income or net worth. The amount of coverage you can buy relative to your income varies by age and insurer. For example, for adults 40 and younger, coverage is limited to 25 to 35 times annual income, while for adults 60 to 70, coverage can be limited to 5 times annual income.

Additionally, if you have one policy and want more, the insurer may require a medical exam to evaluate your insurability. It's also important to consider the potential drawbacks of having multiple health insurance plans, such as double premium and deductible payments, and complications with billing.

Short-Term Insurance Obligation: Understanding the Necessity

You may want to see also

Explore related products

![Island of Death [Dual Format Blu-ray + DVD]](https://m.media-amazon.com/images/I/91ynEn0WzBL._AC_UY218_.jpg)

![]()

Primary and secondary health insurance rules

It is legal to have two health insurance plans, but it is important to understand how primary and secondary insurance works. When you have two forms of health insurance coverage, one is considered primary while the other is secondary. The primary insurance is responsible for paying first on any claims, and the secondary insurance comes into play if the primary insurance is unable to cover the entire claim.

The primary insurance payer is the insurance company that pays the claim first. When you receive health care services, the primary payer pays your medical bills up to the coverage limits. The secondary payer then reviews the remaining bill and picks up its portion. The secondary insurance may cover some or all of the remaining costs. However, you may still be responsible for some cost-sharing, copay, and coinsurance fees.

Determining which health plan is primary is usually straightforward: if you are covered under an employer-based plan, that is typically the primary insurance. If you are also covered under a spouse's plan, that would generally be the secondary insurance. There are rules in place to ensure that individuals cannot profit from medical claims by receiving duplicate coverage for the same illness or injury.

The birthday rule is often used to determine which insurance is primary when a child is covered under two separate parental plans. The parent whose birthday comes first in the calendar year provides primary coverage for the child. If both parents share a birthday, the parent who has had coverage for a longer period will be the primary insurer. In cases of divorced or separated parents, the health plan of the parent with custody is considered primary. If the parents have joint custody, the birthday rule is typically used, unless there is a court order requiring one parent to provide coverage.

Having two health insurance plans can help cover normally out-of-pocket medical expenses. However, it is important to consider the potential drawbacks, such as double premium and deductible payments, coverage overlap, and complications with billing.

Aflac: Primary or Secondary Insurance?

You may want to see also

Explore related products

![]()

Pros and cons of having multiple health insurance plans

Pros of Having Multiple Health Insurance Plans

- Multiple health insurance plans can help cover more medical costs and out-of-pocket expenses than a single plan.

- The primary insurance plan may cover what the second plan does not, and the secondary health insurance plan may cover the copays, deductibles, and coinsurance of the first plan.

- Multiple plans can offset more costs, increasing your savings when receiving healthcare.

- Job loss and turning 26 can result in the loss of coverage, but a secondary insurance plan can prevent a lapse in coverage if you lose your primary plan.

- Multiple plans can give you more accessible care, as most insurance plans limit the types of procedures and care providers you can access.

- If you have a specific medical condition or need, such as fertility treatments or cancer therapies, a separate, specialised insurance plan can provide better coverage.

- You can get additional tax benefits under Section 80D of the Income Tax Act with multiple health insurance plans.

Cons of Having Multiple Health Insurance Plans

- You will likely have to pay separate premiums and deductibles for each plan, which can be costly.

- The reimbursement process may be delayed and more complicated, as insurance providers have to navigate multiple benefits.

- There may be overlap between plans, meaning you don't get additional benefits.

- Your expenses may not be entirely covered, as the combined coverage can't exceed 100% of your health costs.

- You will need to navigate separate policies and rules for each plan.

- Doctors may only want to bill a single policy, so the process could become more complicated.

The Evolution of Term Insurance: A Historical Perspective

You may want to see also

Explore related products

![]()

You can have more than one income protection insurance policy

Yes, it is possible to have more than one income protection insurance policy. This is also known as sick pay insurance. However, it's important to note that having multiple policies does not mean you can claim the full amount from each policy. Each insurance provider will set a limit on the proportion of your salary or income that can be claimed, typically between 50% and 70% of your gross income. If the total benefit payable from multiple policies exceeds this maximum percentage, the payout will be reduced accordingly.

Having two income protection policies can provide flexibility and financial support. For example, if your employer provides one of your policies, you may want to take out a second, personal policy. That way, if you change jobs or your employer withdraws this benefit, you still have financial security. A personal policy can also be tailored to your specific needs and will stay with you throughout your career.

It's worth noting that critical illness insurance works differently from income protection insurance. Critical illness insurance will pay out across multiple policies if you have more than one.

When choosing an income protection policy, it's important to consider the level of cover, the waiting or deferred period before payouts begin, the maximum period of payment, and the retirement age limit.

In summary, while it is possible to have more than one income protection insurance policy, there are limits to the total amount that can be claimed, and careful consideration is needed to ensure the policies provide the intended benefits.

Navigating the Cigna Claims Process: A Guide to Submitting Bills for Swift Reimbursement

You may want to see also

Frequently asked questions

Yes, you can have multiple life insurance policies on the same person. An example is having a top-up policy on a group policy or another policy with additional types of cover.

Yes, you can claim on multiple life insurance policies if you have complied with your duty of disclosure and disclosed this in every subsequent life insurance application form.

As long as you aren't over-insured, it is generally acceptable to have more than one life insurance policy. However, income protection policies typically have built-in offset clauses, meaning you can generally only insure up to 70% of your salary.

![Lone Survivor [4K Ultra HD + Blu-ray + Digital HD]](https://m.media-amazon.com/images/I/91ySONfPzAL._AC_UY218_.jpg)

![Designated Survivor Complete Series [DVD]](https://m.media-amazon.com/images/I/71Uz8ckdzZL._AC_UY218_.jpg)