Life insurance is a crucial financial safety net for individuals and their families. While term life insurance offers lower premiums and sufficient coverage for a specified term, whole life insurance guarantees coverage for life and offers the advantage of cash value accumulation. This cash value can be utilised during the lifetime of the policyholder, providing a unique opportunity for wealth creation and financial stability. The best life insurance for cash flow will depend on individual needs, financial situations, and the specific offerings of different insurance companies. This article will explore the features, benefits, and considerations of various life insurance options to determine which one offers the best cash flow potential.

Characteristics and Values of Life Insurance Policies with Best Cash Flow

| Characteristics | Values |

|---|---|

| Type | Whole life insurance, Variable life insurance, Variable universal life insurance, Term life insurance |

| Premium | Higher premiums for whole life insurance, lower for term life insurance |

| Payout | Death benefit, Living benefit |

| Riders | Disability waiver of premium rider, long-term care rider, index participation feature (IPF) rider |

| Tax | Tax-free withdrawals and loans, tax-free dividends |

| Investment options | High-grade bonds, government-backed mortgages |

| Cash flow banking | Borrowing against the cash value of the policy, using the policy as collateral for a loan |

| Creditor protection | Policy may offer protection from certain legal claims |

| Early surrender | May incur surrender charges |

| Flexibility | Universal life insurance offers more flexibility in premium payments |

Explore related products

What You'll Learn

![]()

Whole life insurance policies

It is important to note that the standard structure for a whole life insurance policy takes a significant amount of time to accumulate cash value, as the premiums primarily fund the policy's death benefit. However, some companies offer modified whole life insurance, which provides lower premiums for the initial years, making it a more affordable option for those seeking to build cash value over time. Additionally, certain companies provide policies with early access to cash value, allowing policyholders to access their funds earlier in the policy's lifespan.

When considering whole life insurance policies, it is crucial to compare quotes and features from different providers to find the most suitable coverage for your needs. Some notable companies offering whole life insurance include:

- State Farm: Offers a combination of low costs and average historical performance of investments.

- Penn Mutual: Known for its strong financial strength and low internal costs, allowing more money to go towards the cash value.

- Guardian: Allows policyholders to choose from level premium policies or "limited payment" policies that can be paid off in a specified number of years.

- MassMutual: Offers a range of whole life policies, some of which earn cash value at a set interest rate of 3%.

- Thrivent: Provides whole life policies with various payment options, including level premiums until a specified age or higher payments over the first 10 years to build cash value faster.

Life Insurance and Short-Form Death Certificates: What's Accepted?

You may want to see also

Explore related products

![]()

Term life insurance policies

Term life insurance is particularly useful for individuals who want to ensure their families are financially protected until large debts, such as mortgages, are paid off or until their children complete their education. It is also a good option for those who simply want to provide a financial safety net for their families without the need for cash value accumulation. This is because term life insurance does not have a cash value component, meaning it does not generate cash values that can be accessed during the policyholder's lifetime.

While term life insurance offers level premiums during the specified term, the rates increase substantially every year if the policy is renewed after the initial term ends. This is in contrast to whole life insurance, which offers the same premiums throughout the policyholder's life. However, term life insurance provides flexibility in that individuals can choose a term that suits their needs, such as ensuring coverage until retirement or until their financial dependents can support themselves.

In summary, term life insurance policies offer low-cost coverage for a specified term, making them ideal for individuals seeking financial protection for their loved ones without the need for cash value accumulation. These policies are a good option for those wanting to ensure their families are taken care of during specific periods, such as until mortgages are paid off or children finish their education. However, individuals should be mindful of the substantial rate increases if the policy is renewed after the initial term.

Life Insurance for Christians: A Biblical Perspective

You may want to see also

Explore related products

![]()

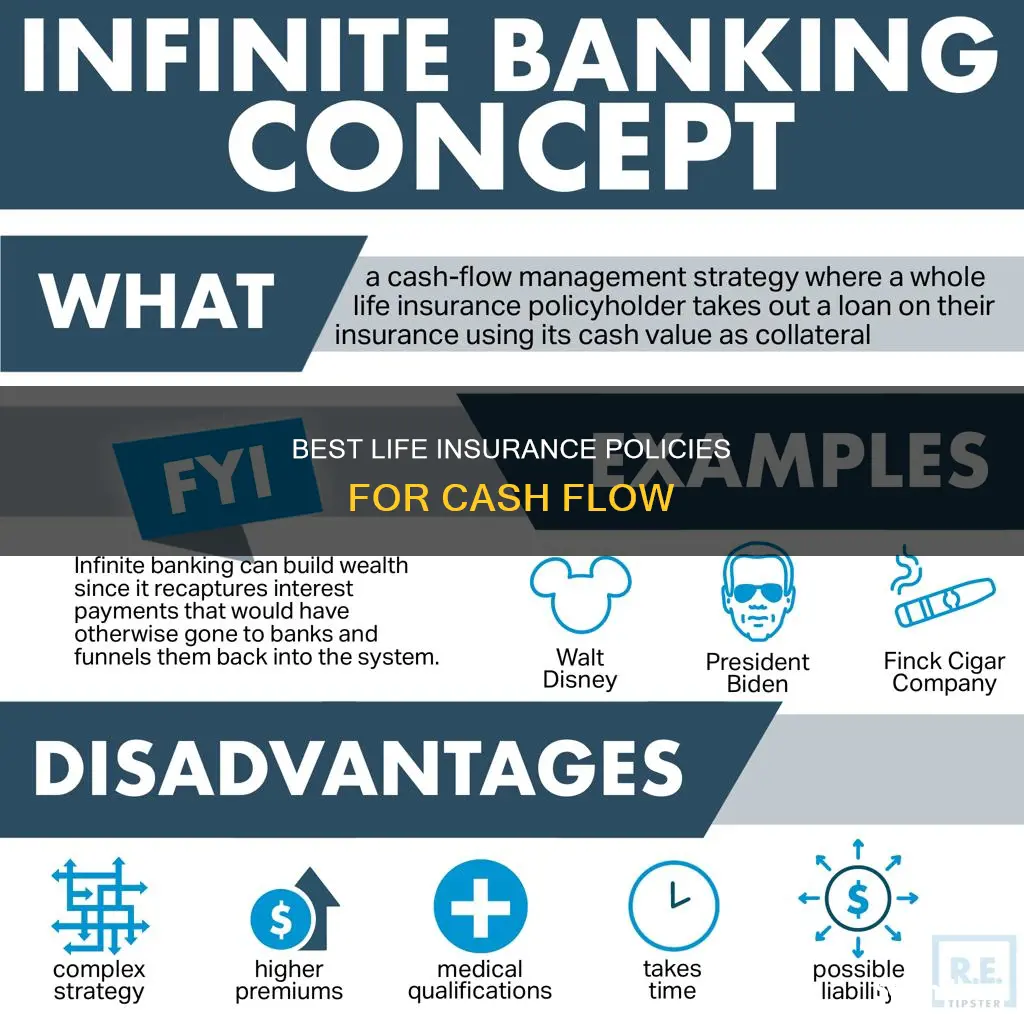

Cash flow banking

To implement cash flow banking, individuals obtain a whole life insurance policy that offers high cash value and dividend payments. This type of policy differs from traditional whole life insurance, which primarily focuses on providing a death benefit. With a cash flow banking-oriented policy, the emphasis is on building cash value from the outset. This is achieved by designing the policy with a higher proportion of "paid-up additions" compared to the base premium. The higher the paid-up additions, the greater the early cash value.

The cash value of the policy can then be used as collateral to secure loans from the life insurance company, essentially turning the policy into a bank account. This strategy is known as "infinite banking" or "becoming your own banker." The cash value continues to grow and earn interest even while the individual borrows against it, creating a source of funding for personal expenses, investments, or business ventures. Additionally, the loan withdrawals are typically tax-free, providing further financial advantages.

It is important to note that not all whole life insurance policies are suitable for cash flow banking. Individuals interested in this strategy should compare quotes and features from different providers to find the most appropriate coverage for their needs. Working with a certified cash flow insurance specialist can help ensure that the policy is structured correctly to minimize fees and maximize cash value growth.

Qualifying Life Events: Health Insurance Changes and You

You may want to see also

Explore related products

![]()

Policy loans

To access a policy loan, you need to have a whole life insurance policy that has accumulated cash value. The availability of policy loans depends on the insurance company and the specific terms of the policy. Some policies may offer early access to cash value, while others may require a certain number of years before funds are available for borrowing. It is important to compare quotes and features from different providers to find the most suitable coverage for your needs.

Life Insurance Premium Financing (LIPF) is a strategy where a policyholder borrows from a third-party lender, such as a bank, to cover the cost of their life insurance policy. The loan is then repaid over time, either through installments or a policy loan. LIPF allows policyholders to preserve liquidity and free up capital for other investments, but it is important to consider potential pitfalls, such as fluctuating interest rates, collateral requirements, policy performance, and complexity.

Generate Life Insurance Leads in India: Strategies for Success

You may want to see also

Explore related products

![]()

Riders

There are several types of riders that can be added to a life insurance policy, each offering unique benefits. For example, the Paid-Up Additions Rider increases the policy's death benefit, allowing the policyholder to leave a larger financial legacy for their heirs. The Guaranteed Insurability Rider allows the policyholder to purchase additional coverage in the future without medical underwriting, protecting their ability to expand their financial strategy as needed. The Child Term Rider provides affordable life insurance coverage for children, ensuring protection for the policyholder's family and allowing for a smooth conversion to a whole-life policy in the future.

Another type of rider is the Waiver of Premium Rider, which waives future premiums if the insured becomes permanently disabled or loses their income due to injury or illness before a specified age. This can be especially valuable for the main breadwinner of a family, as it exempts them from paying premiums until they are ready to work again. Similarly, the Accidental Death Rider also waives future premiums under certain conditions, however, it's important to understand the restrictions on this rider as the definition of an "accident" may vary between insurers.

The Best Time to Cancel Permanent Life Insurance

You may want to see also

Frequently asked questions

Cash flow life insurance is a policy that offers living benefits. This means that you can use the policy during your lifetime, and it will still pay out a death benefit to your beneficiary. Cash flow insurance policies have higher premiums, but they are guaranteed to pay out a death benefit for life.

The best cash flow life insurance company depends on your needs and financial situation. Some companies that offer cash flow life insurance include Guardian, MassMutual, Thrivent, State Farm, Northwestern Mutual, and Penn Mutual.

Cash flow life insurance allows you to use the cash value of your policy as collateral to receive a loan from a life insurance company. The money you borrow is tax-free, and the cash value of the policy continues to grow and earn interest even while you borrow against it.

When choosing a cash flow life insurance policy, it is important to compare quotes and features from different providers to find the most suitable coverage for your needs. You should also consider the company's financial strength and the policy's historical performance.