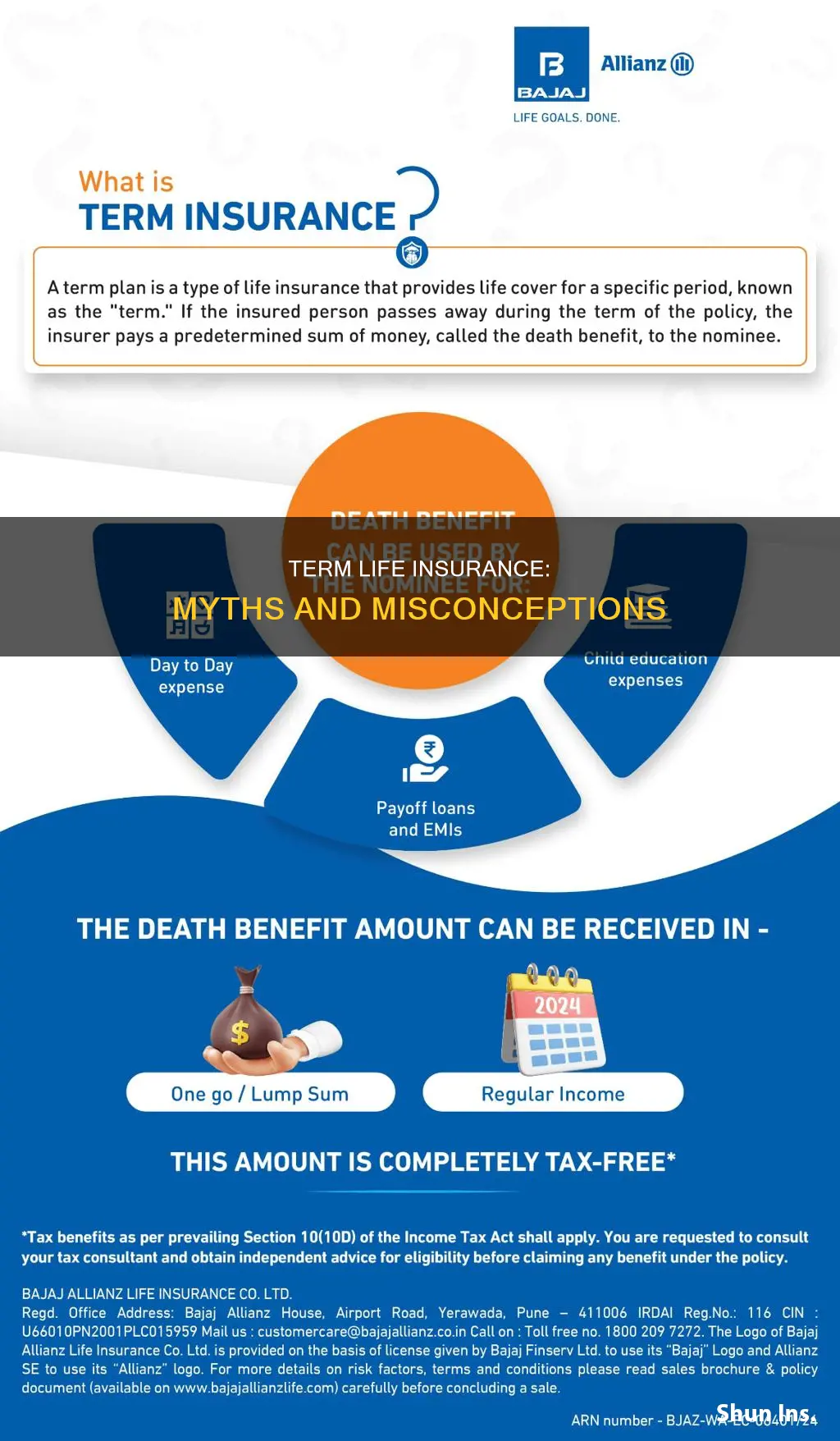

Term life insurance is a type of insurance that provides coverage for a specified period, typically 10, 15, 20, or 30 years. It is designed to provide a death benefit during the specified term of the policy, and any premiums paid are used to secure this benefit, rather than accumulating cash value. Term life insurance is ideal for people who want substantial coverage at a low cost and cannot afford the higher monthly premiums associated with whole life insurance. However, several misconceptions about term life insurance exist, and it is important to discern which statements about it are not correct.

| Characteristics | Values |

|---|---|

| Type of insurance | Term life insurance |

| Coverage | Substantial coverage |

| Cost | Low cost |

| Premium | Premium increases with age |

| Premium calculation factors | Age, gender, health, company's business expenses, earnings from investments, and mortality rates |

| Premium calculation requirements | Medical exam, driving record, current medications, smoking status, occupation, hobbies, family history |

| Payout | Payout to beneficiaries if the insured dies during the policy term |

| Payout usage | Settle healthcare and funeral costs, consumer debt, mortgage debt, and other expenses |

| Payout tax | Not typically taxable |

| Payout to beneficiaries | Not required to settle the deceased's debts |

| Maximum age | 80 to 90 years old |

| Comparison to whole life insurance | Higher monthly premiums |

| Conversion to whole life insurance | Possible with a conversion rider |

| Conversion rider features | Maintain original health rating, decide when and how much to convert |

| Whole life insurance premium basis | Age at conversion |

| Accumulation of cash value | No accumulation of cash value |

Explore related products

$15.53

What You'll Learn

![]()

Term life insurance does not accumulate cash value

Term life insurance is a good option for people who want substantial coverage at a low cost but cannot afford or do not want to pay the much higher monthly premiums associated with whole life insurance. It is similar to car insurance in that it is statistically unlikely that you will need it, and the premiums are lost if you do not. However, if the worst happens, your family will receive the benefits.

Term life insurance premiums are based on the policy's value (the payout amount) and factors such as age, gender, and health. The insurance company may also consider business expenses, earnings from investments, and mortality rates for each age. The premium increases with age, and a medical exam may be required. The insurance company may also inquire about your driving record, current medications, smoking status, occupation, hobbies, and family history.

Convertible term life insurance is a type of term life policy that includes a conversion rider, allowing the policyholder to convert an in-force term policy or one about to expire to a permanent plan without going through underwriting or proving insurability. The conversion rider allows the policyholder to maintain their original health rating and decide when and how much of the coverage to convert. While this guarantees approval without a medical exam, overall premiums will increase significantly since whole life insurance is more expensive than term life insurance.

Financial Advisors and Life Insurance: What's the Deal?

You may want to see also

Explore related products

$12.99 $14.95

![]()

Premiums are based on policy value and factors like age, gender and health

When purchasing a term life insurance policy, the insurance company determines the premium based on the policy's value and factors such as age, gender, and health. Term life insurance is a good option for those who cannot afford the much higher monthly premiums associated with whole life insurance.

Age is the most important factor in determining the cost of your premium. The younger you are, the lower your payments. This is because the likelihood of an insurer having to pay out on your policy increases as you age. As a result, premiums increase. The premium cost increases from 8% to 10% on average for every year of age. Therefore, the longer you wait to buy life insurance, the more you will have to pay for premiums.

Gender is also a key factor in determining the price of life insurance. Women generally live longer than men, so they pay less for life insurance than men do. Men generally pay more for life insurance than women because they have a shorter life expectancy.

Health is another important factor in setting the premium for term life insurance. Insurers may require a medical exam and access to your health records before issuing a policy. Having a history of medical conditions, especially serious illnesses such as heart disease or cancer, will increase your premiums. Insurers will also look at other metrics that could indicate future medical conditions, such as your weight, cholesterol levels, and blood pressure.

Other considerations that affect the premium rates include the company's business expenses, investment earnings, and mortality rates for each age. Additionally, the insurance company may inquire about your driving record, current medications, smoking status, occupation, hobbies, and family health history.

Life Insurance Lock-Ins: 30-Year Commitment?

You may want to see also

Explore related products

![]()

It is a good option for those who can't afford whole life insurance

Term life insurance is a good option for those who want coverage for a specific period and cannot afford the much higher monthly premiums associated with whole life insurance. It is ideal for those who want substantial coverage at a low cost. Term life insurance is often the most affordable option as it is temporary and has no cash value. Whole life premiums are much higher as the coverage typically lasts a lifetime and the policy grows in cash value.

Term life insurance is a good option for those who want to save money in the short term. It is also a good option for those who are less familiar with how life insurance and financial planning work, as the whole life policy's cash value, dividends, and policy loan components can be challenging to understand and manage. Whole life insurance is a lifelong commitment, so it is important to make sure you can afford the higher premiums. If you miss premium payments, your policy could lapse.

Term life insurance is also a good option for those with current or future health concerns. A convertible term policy can help you maintain coverage without taking a new medical exam. When you buy a whole life insurance policy, the insurance company may require a medical exam and inquire about your driving record, current medications, smoking status, occupation, hobbies, and family history.

Term life insurance is customizable and specific to your timeline. It is ideal for young families as it ensures children can afford an education and maintain their standard of living until they are old enough to support themselves. It is also a good option for homeowners with mortgages, as it can help families pay off the home if the insured person dies before the mortgage term ends.

Life Insurance: Age-Related Eligibility and Options

You may want to see also

Explore related products

![]()

Convertible term life insurance includes a conversion rider

Convertible term life insurance is a type of term life insurance policy that includes a conversion rider. This rider allows the policyholder to convert their term life insurance policy into a permanent life insurance policy at any point during a specified period or before reaching a certain age. The conversion rider guarantees the right to make this change without undergoing further medical underwriting or providing proof of insurability.

The inclusion of the conversion rider in convertible term life insurance offers several benefits. Firstly, it provides flexibility to the policyholder by giving them the option to convert their term policy to a permanent one, such as whole life or universal life insurance. This conversion can be done without the need for a new health exam or update, ensuring that the policyholder's original health rating is maintained even if their health deteriorates. Secondly, it allows policyholders to secure lifelong coverage, which is a significant advantage over term life insurance, which only provides coverage for a specified period.

The cost of a convertible term life insurance policy with a conversion rider may vary. In some cases, the rider may be included in the term life insurance policy at no additional cost. However, certain companies might charge an extra fee for this feature. While the rider itself may be free or inexpensive, converting the term policy into a permanent one will generally result in a substantial increase in premiums. This increase in cost is due to the lifelong coverage and cash value component of permanent life insurance policies.

It is important to note that the specifics of term conversion riders can vary between insurance companies and policy terms. Each insurance company sets its own procedures for policy conversion, and the exact policies that can be converted will be stated in the contract. Therefore, it is advisable to consult with an insurance agent or the insurance company to understand the conversion options available and make an informed decision based on individual needs and circumstances.

In summary, convertible term life insurance with a conversion rider offers policyholders the flexibility to convert their term policy into a permanent one without undergoing additional medical underwriting. While the rider may be included at no extra cost, converting to a permanent policy will generally result in higher premiums due to the nature of lifelong coverage. The specifics of the conversion rider can vary, so it is essential to review the contract and consult with insurance professionals before making any decisions.

Life Insurance Double Indemnity: Still a Viable Option?

You may want to see also

Explore related products

![]()

It is a temporary form of insurance

Term life insurance is a temporary form of insurance that provides coverage for a set period, usually 10 to 30 years. It is a good option for people who want substantial coverage at a low cost and cannot afford or do not want to pay the higher monthly premiums associated with whole life insurance. Term life insurance is similar to car insurance in that it is statistically unlikely that you will need it, and the premiums are a waste of money if you don't. However, if the worst happens, your family will receive the benefits.

When you buy a term life insurance policy, the insurance company determines the premium based on the policy's value (the payout amount) and factors such as age, gender, and health. The premium is locked in for the period of coverage selected. If you choose to renew your coverage, the premiums will increase annually. The right choice for you will depend on your needs.

Term life insurance policies are ideal for people who want substantial coverage at a low cost. People who buy term life insurance pay premiums for an extended period and get nothing in return unless they die before the term expires. Term life insurance premiums also increase with age.

Convertible term life insurance is a type of term life policy that includes a conversion rider. The rider guarantees the right to convert an in-force term policy—or one about to expire—to a permanent plan without going through underwriting or proving insurability. The conversion rider should allow you to convert to any permanent policy the insurance company offers without restrictions. The primary features of the rider are maintaining the original health rating of the term policy upon conversion and deciding when and how much of the coverage to convert.

Temporary life insurance is a short-term coverage option that can be purchased during the life insurance application process before your official policy goes into effect. It provides coverage while you wait for your life insurance application to be approved. If you die before underwriting is complete, your beneficiaries will receive a death benefit from your temporary life insurance policy. Temporary life insurance usually lasts a maximum of 60 to 90 days.

Renewing Your Massachusetts Life Insurance License: A Step-by-Step Guide

You may want to see also

Frequently asked questions

No, term life insurance does not have a cash value component. Its primary function is to provide a death benefit during the specified term of the policy.

No, term life insurance is not permanent. It provides coverage for a specified term, typically 10, 15, 20, or 30 years.

No, if you outlive the term of the policy, you will not receive any money back.

Yes, term life insurance is ideal for people who want substantial coverage at a low cost. It is a good option for those who cannot afford the higher premiums associated with whole life insurance.

Yes, you can convert your term life insurance policy to a whole life insurance policy. This can be done by adding a conversion rider to your term policy, which guarantees the right to convert to a permanent plan without additional underwriting.