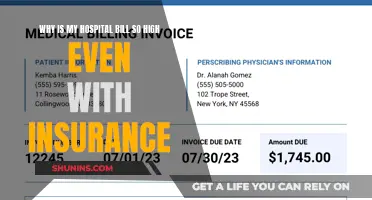

Many people with health insurance still find themselves in medical debt. This is often due to the fact that insurance plans are a cost-sharing agreement, where the insurance company will only cover costs for preventive care, such as check-ups and vaccinations. For other services, insurance companies require the insured to cover all costs until they reach a specified amount, known as a deductible. The amount of the deductible depends on the specific policy and can vary widely. Once the deductible is met, the insurance company will begin to cover some of the medical costs for the rest of the year. However, the insured is still responsible for a portion of the costs, known as coinsurance. Additionally, medical billing can be opaque, with providers and insurance carriers having nondisclosure agreements that prevent them from revealing the provider's billed rates or the insurance company's discounts. This makes it difficult for patients to know how much a procedure will cost upfront.

| Characteristics | Values |

|---|---|

| Reason for receiving a hospital bill | You have a cost-sharing agreement with your insurance company, which means that you are required to cover all costs until you reach a specified amount (deductible) |

| Deductible | A fixed dollar amount that you need to pay within a defined period of time before your insurer covers some of the costs for eligible medical services |

| Copayment | A fixed dollar amount ($5-$30) that you pay every time you receive medical care |

| Coinsurance | The percentage of costs the subscriber (the patient) has agreed to pay, e.g., 20% |

| Explanation of Benefits (EOB) | A document provided by the insurance company that breaks down how much they will pay for a service or visit and how much you are responsible for |

| Out-of-pocket maximum | The most you'll have to pay for your medical costs in a given time period, usually one calendar year |

| Out-of-network care | Out-of-pocket maximums for out-of-network care might be double the in-network amount |

Explore related products

What You'll Learn

- Insurance companies require patients to cover all costs until they reach a specified amount, known as a deductible

- After receiving care, the hospital sends a bill to the insurance company, which determines how much they will pay and how much the patient owes

- Copayments are a fixed dollar amount that patients pay every time they receive medical care

- Coinsurance is when patients pay a percentage of the total costs

- Patients may receive multiple bills after hospital treatment, as certain providers bill separately

![]()

Insurance companies require patients to cover all costs until they reach a specified amount, known as a deductible

Insurance Deductibles Explained

The amount of the deductible depends on the specific insurance policy and can vary widely. Deductibles can be a specific dollar amount or a percentage of the total amount of insurance on a policy. For instance, a health insurance policy may have a $500 deductible, while a homeowner's insurance policy could have a 2% deductible. Deductibles typically reset at the start of each new policy period.

It's important to note that deductibles only apply to covered expenses, and some insurance policies may not have deductibles at all. Additionally, the higher the deductible, the lower the insurance premium tends to be. This is because a higher deductible means you assume greater financial responsibility for expenses before the insurance company starts paying.

When choosing an insurance policy, it's crucial to consider your financial situation and individual circumstances. For example, if you have a chronic medical condition requiring frequent doctor visits, you may opt for a lower deductible to help manage out-of-pocket expenses. In contrast, a healthy individual who rarely needs medical care may prefer a higher deductible to save money on premiums.

Weighing the Benefits: Exploring the Switch from Term to Permanent Life Insurance

You may want to see also

Explore related products

![]()

After receiving care, the hospital sends a bill to the insurance company, which determines how much they will pay and how much the patient owes

After receiving care, the hospital will send a bill to your insurance company. This is a cost-sharing agreement between you and your insurance provider. The bill will outline the services provided and the costs incurred. The insurance company will then determine how much they will pay for each service or visit, and how much you, the patient, are responsible for. This breakdown is shown on the Explanation of Benefits (EOB) provided by the insurance company. The EOB is sent to both the hospital and the patient.

The EOB will detail the amount that the insurance company will cover and the amount that the patient owes. Once the hospital receives this information, they will send a bill to the patient for the amount they owe. This is known as the patient's responsibility. If you have questions about what was covered and how much was paid by your insurance company, you can contact them directly.

It is important to understand the different types of costs associated with your medical bill. These may include deductibles, copayments, and coinsurance. A deductible is a fixed amount that you must pay within a defined period, such as a calendar or plan year, before your insurer covers any costs. A copayment, or copay, is a fixed dollar amount that you pay each time you receive medical care. For example, you may have a $20 copay that you pay during a doctor's appointment. Copay amounts can vary depending on the type of service received. Coinsurance refers to the percentage of costs that the patient has agreed to pay. For instance, if your insurance covers 80% of eligible expenses, you may be required to pay the remaining 20% as coinsurance.

It is worth noting that you may receive multiple bills after being treated at a hospital. This is because certain providers, such as specialists, may bill separately for their services. Additionally, if you were transported to the hospital by ambulance, you may receive a separate bill for that service as well. These charges are typically referred to as professional fees for physicians and facility fees for the hospital or emergency room.

**The Ins and Outs of Insurance Billing: Understanding a PCP's Role**

You may want to see also

Explore related products

![]()

Copayments are a fixed dollar amount that patients pay every time they receive medical care

Copayments, or copays, are a common feature of many health insurance plans. They are a fixed, flat fee for certain types of office visits, prescription drugs, or other services. Copayments are usually a set dollar amount, such as $20 for a doctor's visit or $10 for a prescription medication. They are a form of cost-sharing between the insurance company and the policyholder, helping to keep monthly medical bills in check.

Copayments are typically paid directly to the healthcare provider at the time of receiving medical service or care. They are usually due at the time of your visit to the doctor and are paid either before or after you see the doctor. The amount of the copayment depends on the type of visit, such as a visit to a doctor, specialist, or emergency care. Copayments for doctor visits are generally lower compared to specialist or urgent care visits.

Copayments are usually the responsibility of the policyholder. For example, if your plan includes a copayment of $20 for office visits, you'll pay $20 to your doctor whenever you have an appointment. This is a shared cost between you and your insurance company. You pay the copayment, and your insurer pays the rest of the bill.

Copayments are a predictable way for individuals to contribute to their healthcare costs, making it easier to access medical care without bearing the full financial burden. They are a standard part of many health insurance plans and help to share the cost of healthcare services with policyholders.

Exploring the Benefits: How Secondary Insurance Impacts Out-of-Pocket Costs

You may want to see also

Explore related products

![]()

Coinsurance is when patients pay a percentage of the total costs

Coinsurance is usually billed after a service is received. The amount of coinsurance depends on the health plan. Most health insurance policies include an annual deductible, which is the amount the person covered must pay before insurance coverage "kicks in". Once the deductible is met, coinsurance takes effect, and the patient is responsible for paying a percentage of the remaining costs.

Coinsurance is different from a copay, which is a set dollar amount that the patient pays each time they receive medical care. Copays are typically smaller amounts, such as $5 to $30, while coinsurance can result in larger payments as they are based on a percentage of the total cost.

Coinsurance is one way that patients pay for health insurance. Other ways include premiums, copays, and deductibles. Health plans also typically have out-of-pocket maximums, which is the most a patient will pay out of pocket for health care services over a year. Once the patient reaches this maximum, the health insurance company will cover 100% of the health service bills for the rest of the plan year.

The Hidden Hazards of Insurance Avoidance: Understanding the Complexities and Risks

You may want to see also

Explore related products

![]()

Patients may receive multiple bills after hospital treatment, as certain providers bill separately

For example, if a patient visits the emergency room and has an X-ray and laboratory tests, they may receive a bill from the hospital for technical resources, a bill from the emergency room physician for professional services, a bill from the radiologist for interpreting any X-rays, and a bill from the pathologist for analyzing any specimens taken.

In addition, patients may also receive separate bills from specialists who provide services at the hospital, such as radiologists, anesthesiologists, cardiologists, surgeons, and pathologists. These specialists bill for their services separately from the hospital or emergency room.

Furthermore, if a patient is transported to the hospital by ambulance, they may receive a separate bill for this service as well. These charges are often referred to as "professional fees" by insurance companies and providers.

It is important to understand the breakdown of charges and which services are covered by insurance to avoid unexpected costs and manage financial responsibilities effectively.

The Pros and Cons of Direct Billing for Body Shop Repairs

You may want to see also

Frequently asked questions

Your insurance plan is a cost-sharing agreement between you and your insurance company. Many insurance companies require you to cover all costs until you reach a specified amount, known as a deductible. Once you reach this amount, the insurance company starts paying for covered services.

A deductible is a fixed amount that you need to pay within a defined period before your insurer will start to cover some of the costs for covered medical services. For example, if you have a $500 deductible, you will have to pay for your medical costs for non-preventative care until you have paid a total of $500.

Coinsurance is when you are required to share costs with your insurance provider. Instead of paying a fixed amount each time you receive medical care, you pay a percentage of the total costs. For example, your insurance company may pay 80% of the cost, and you pay the remaining 20%.

A copayment, or copay, is a fixed dollar amount that you pay every time you receive medical care. For example, you may have a $20 copay that you pay to the provider's office when you go in for a doctor's appointment.