Life insurance dividends are payments from an insurance company to policyholders, usually for whole life insurance policies. They are considered a return of premium and are tax-deferred until they exceed the amount of premium paid. Policyholders can choose to receive their dividends as cash or use them to buy paid-up additions, which can increase the death benefit and cash value of the policy over time. This is because paid-up additions are like adding to the value of your original policy, and as you acquire more, your death benefit increases, making you eligible for more dividends.

Characteristics and Values of Life Insurance Dividend Options that Increase the Death Benefit

| Characteristics | Values |

|---|---|

| Paid-up additions | Additional coverage that is added to your face amount, increasing the death benefit and cash value of your policy |

| Interest accumulation | Accumulating interest within the policy can increase the overall value of your policy |

| Repay policy loans | Using dividends to repay loans can help preserve the value of your policy for your beneficiaries |

| Purchase term life insurance | Using dividends to purchase term life insurance can be an efficient way to build a death benefit with a whole life policy in the short term |

| Reduce premium payments | Applying dividends to your life insurance premium can make your policy more affordable |

Explore related products

What You'll Learn

![]()

Buy paid-up additions

Paid-up additional insurance is a way to increase the death benefit of your life insurance policy without increasing your premiums. It is an option for those with whole life policies that pay dividends. Paid-up additions are small chunks of extra coverage that you can buy using your policy's dividends. Each paid-up addition has its own death benefit and cash value and also earns dividends, allowing the value of your policy to increase over time.

The benefit of paid-up additions is that they are paid up—you don't have to pay premiums on them once purchased. This means that you can increase your coverage without going through medical underwriting, which is beneficial if your health has declined since the original policy was issued. The additional coverage can also help your life insurance keep up with inflation.

To purchase paid-up additions, you will typically need to add a paid-up additions (PUA) rider to your policy. This allows you to buy PUAs with additional premium payments on top of your base premium. Some policies contain a provision that allows the purchase of PUAs with your dividends, but this is less common. When deciding whether to purchase a PUA rider, it's important to note that some insurance companies have a "use it or lose it" policy, which may require you to buy a de minimis amount of PUAs each year to maintain your ability to use the rider in the future.

It's worth noting that dividends are never guaranteed, even though some mutual life insurance companies have a long track record of paying them. If you use dividends to purchase paid-up additions, you won't need to provide new proof of insurability, and the additional insurance you can purchase will be based on your age at the time the dividend is issued.

Group Life Insurance: Cashing Out and Claiming Benefits

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Reduce premium payments

Life insurance dividends are considered a return of premium and are tax-deferred until they exceed the amount of premiums paid. Policies with dividend options usually have higher premiums. Dividend options allow policyholders to reduce their out-of-pocket expenses by applying their dividends to their life insurance premium. This can make the policy more affordable by reducing the amount they need to pay each year.

It is important to note that even if you are able to suspend making out-of-pocket premium payments, you may have to resume them at a later date due to dividend changes, or if you take loans or withdrawals. The total cash value of your policy includes the guaranteed cash value, the cash value of paid-up additional insurance, dividends that have accumulated interest, and, for most permanent policies, termination dividends. The total death amount equals the policy face amount, plus all riders on the insured, plus any paid-up additional insurance, plus any dividend accumulations, plus any termination dividend.

If you choose to reduce your premium payments using dividends, you must start paying your premium annually. For instance, if your annual premium is $8,000 and your dividend that year is $1,500, you would still need to pay the remaining $6,500 all at once. Since dividends fluctuate, you might be paying more or less of your premium each year.

In addition, once the dividend payment equals or exceeds the premium due amount, the dividend can pay the entire premium due, and the policyholder does not need to make any further payments. This option is quite common in older whole life policies, as the policyholder can keep their death benefit active without paying the premium. However, choosing this option has some consequences that policyholders should understand. Firstly, the insurance company will require the policyholder to change the payment frequency to annual if it is not already. This could potentially cause cash flow problems for policyholders who pay premiums under a different frequency.

Variable Life Insurance: Can It Run Dry?

You may want to see also

Explore related products

![]()

Collect interest

When you choose to collect interest, any dividends declared by the life insurance policy are used to purchase additional death benefits, which are then added to your policy's face value. This option can be particularly advantageous if you're looking to maximize the death benefit payout and ensure your loved ones receive a substantial financial cushion in the event of your passing.

Here's how it works: when a dividend is declared, the insurance company will use that money to buy something known as "paid-up additions." Essentially, these additions are small amounts of insurance that are attached to your existing policy. They function in the same way as your primary policy, with the exception that they have their own cash value and accumulate dividends independently. As a result, your overall death benefit grows over time, providing even greater financial protection for your beneficiaries.

The beauty of this option lies in its ability to leverage the power of compound interest. By purchasing these paid-up additions, you're not just increasing the death benefit; you're also investing in a vehicle that can generate its own growth. The cash value of these additions earns interest, and any dividends they generate can be used to buy even more additions. This compounding effect can lead to significant growth in the death benefit over the life of the policy, all without any additional out-of-pocket expenses from you.

Additionally, choosing to collect interest can provide tax advantages. The Internal Revenue Service (IRS) typically treats life insurance death benefits as non-taxable income. This means that any increase in the death benefit due to the collection of interest is generally free from income tax. This feature further enhances the financial benefit for your beneficiaries, ensuring they receive the full amount without tax deductions.

It's important to note that while this dividend option offers long-term benefits, it may not be suitable for everyone. If your primary goal is to access the dividends during your lifetime, other options, such as receiving cash payments or reducing premiums, might be more appealing. However, if maximizing the death benefit payout and harnessing the power of compound interest align with your financial goals, choosing to collect interest can be a wise strategy.

Life Insurance for Children: When to Keep or Cancel

You may want to see also

Explore related products

![]()

Repay policy loans

Repaying policy loans with dividends is a good way to reduce your outstanding debt without making out-of-pocket repayments. Policy loans are a quick and easy way to get cash in hand when you need it, but they do come with risks. Interest accrues on the loan, and if you don't pay it back, the death benefit will be lower. If the interest accrues to the point where you owe more than you have in your policy, it will lapse. If the policy lapses, the cash you took out may be treated as income by the IRS, and you may owe taxes on it.

Policy loans are available on permanent life insurance policies that build cash value, such as whole life and universal life insurance policies. Term life insurance does not have a cash value component, so you cannot borrow against it. When you take out a policy loan, the insurer lends you the money and uses the cash in your policy as collateral. You don't actually withdraw any money from the policy itself. The funds you borrow are tax-free, but there are typically interest payments.

The interest rate on a life insurance loan is usually lower than that of a personal loan or credit card, typically ranging from 5% to 8%. There is no strict repayment schedule for life insurance loans, but it is in your best interest to pay it back as soon as possible. The longer the loan is left unpaid, the more interest you will end up owing. You can make regular payments to pay down the loan, but if you don't, your policy will be in jeopardy of lapsing, especially if the amount owed exceeds your policy's cash value.

If you die with an outstanding loan on your policy, your insurer will deduct the amount owed from your death benefit, leaving your beneficiaries with less money. Therefore, using dividends to repay policy loans can help preserve the value of your policy for your beneficiaries.

Legal and General Life Insurance: Contact and Claims

You may want to see also

Explore related products

![]()

Choose a whole life policy

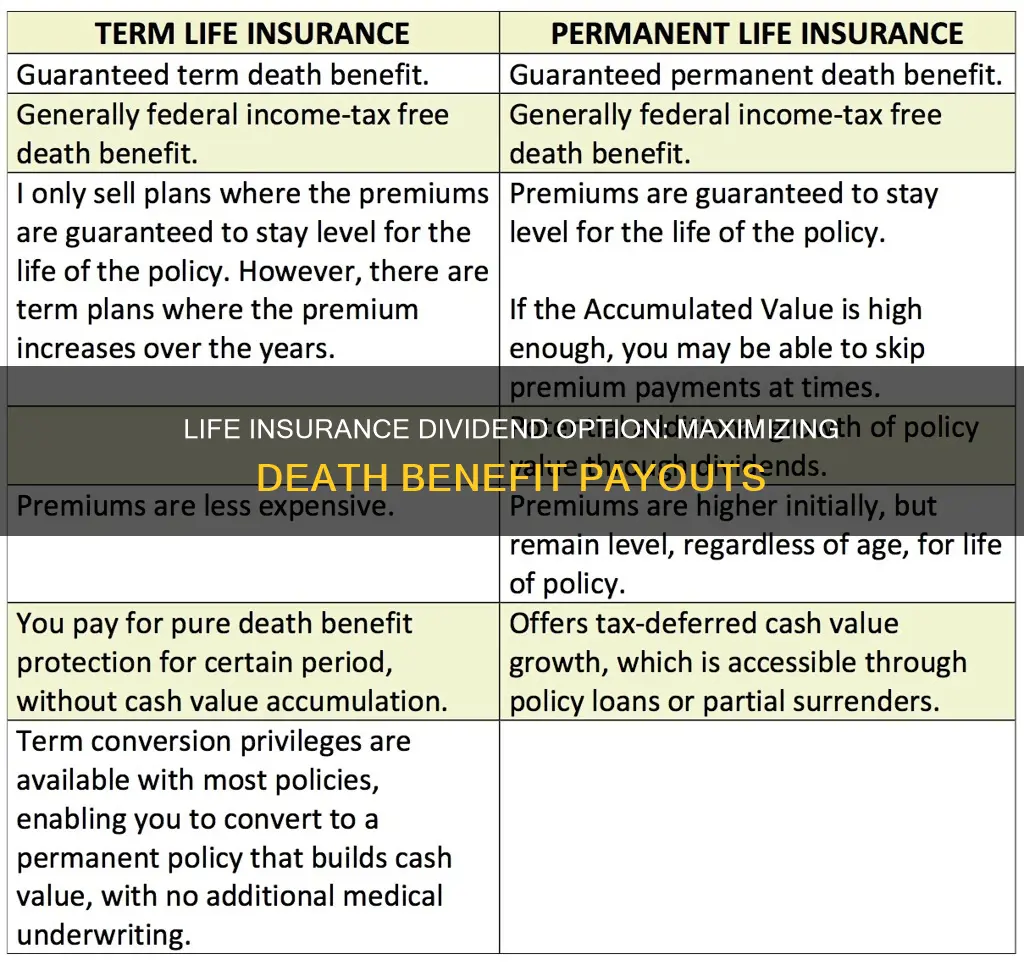

Whole life insurance is a type of permanent life insurance that covers you for your entire life. Unlike term life insurance, which covers you for a specific period, whole life insurance stays in effect as long as you pay the premiums. Whole life insurance policies typically have fixed premiums, which do not increase over time. This means that the amount you pay every month will stay the same, offering predictable costs.

Whole life insurance also has a savings component, known as the "cash value," which the policy owner can draw on or borrow from. This cash value grows over time, usually at a guaranteed rate set by the insurance company, and can be used for things like education expenses, buying a home, or retirement income. The death benefit is also established when you sign up for your policy and stays the same while the policy remains active.

When choosing a whole life insurance policy, it's important to assess your financial goals and needs. Determine whether you are seeking lifelong coverage, a savings component, or both. Calculate the coverage amount you need by considering factors such as outstanding debts, future expenses, and income replacement. It's also crucial to evaluate whether you can afford the premium payments over the long term.

Whole life insurance policies often pay out dividends, and policyholders can choose how to receive them. Dividends can be used to reduce premium payments, making the policy more affordable. They can also be used to increase your coverage by purchasing paid-up additions, which will increase both the death benefit and the cash value of your policy. Dividends can also be collected with interest in a separate account, allowing for long-term growth. This option may be suitable for those seeking a significant death benefit.

Universal Life Insurance Malaysia: What You Need to Know

You may want to see also

Frequently asked questions

Dividends are payments from the insurance company to policyholders, typically for whole life insurance policies. They vary based on the company's performance and are not guaranteed. Dividends are considered a return of premium and are tax-deferred until they exceed the amount of premium paid.

Life insurance dividends can be used to purchase additional paid-up life insurance, also known as paid-up additions (PUAs). This increases the death benefit and the cash value of the policy over time. The growth is compounded and typically tax-deferred.

Life insurance dividends can also be used to reduce premium payments, repay policy loans, or collect interest in an account. Dividends can be taken as cash, but this option may be taxable.

When choosing a life insurance dividend option, consider your financial goals and circumstances. If you want to increase the death benefit, purchasing paid-up additions is a good option. If you want to reduce expenses, consider using dividends to lower premium payments or repay policy loans. Interest accumulation can be a good option for long-term growth, but the interest may be taxable.