Life insurance rates vary depending on several factors, including age, health, gender, and lifestyle choices. The younger and healthier you are, the cheaper your premiums are likely to be. The cost of life insurance also depends on the type of policy you choose. Whole life insurance tends to be more expensive than term life insurance, as it provides coverage for your entire life. When choosing a life insurance policy, it's important to consider your financial and family situation, as well as your coverage needs and budget. By comparing rates and policies from different insurers, you can find the best option that suits your unique circumstances and goals.

| Characteristics | Values |

|---|---|

| Average monthly cost | $26 |

| Factors that affect the rate | Age, gender, health, lifestyle choices, medical history, family medical history, coverage amount, high-risk hobbies, smoking, lifestyle and occupation, and more. |

| Whole life insurance | More expensive than term life insurance; may be worthwhile depending on your situation. |

| Term life insurance | More affordable; offers lower premiums than permanent policies. |

Explore related products

What You'll Learn

![]()

Age and health

Insurers assess premiums based on multiple personal rating factors, but an emphasis is placed on mortality risk. As applicants get older, the policy costs increase due to the heightened chance of a death benefit claim. While health status, medical history, and lifestyle choices also sway pricing, age remains a primary factor that can greatly inflate quotes over time.

Maintaining a healthy lifestyle can help lower your life insurance rate. Being overweight, for example, is linked to medical conditions with higher mortality rates, which can increase your premium. Similarly, if you engage in high-risk hobbies such as skydiving, you may pay more in premiums due to the increased risk of injury or death.

It's important to note that life insurance rates are highly personalized, and the best time to buy it is as soon as you realize you need it. Your financial and family situation, as well as your unique needs and circumstances, will determine the type and amount of coverage you require. Regularly reviewing your insurance policy is recommended to ensure it still aligns with your life circumstances.

Life Insurance with COPD: Is It Possible?

You may want to see also

Explore related products

$43.3

![]()

Coverage amount

The coverage amount you select for your life insurance will affect the rate you pay. The more coverage you opt for, the higher the rate. When deciding on the coverage amount, you should consider the following:

Funeral and Burial Expenses

The coverage should be enough to pay for funeral and burial expenses.

Mortgage and Other Debts

You should consider the amount of coverage needed to pay off your mortgage and any other debts. This includes student loans that you may have co-signed.

Income Replacement

The coverage should be sufficient to replace your income for the number of years your family would need financial support. This is especially important if you have children or are supporting a family.

Children's Tuition

If you have children, you should factor in the total cost of their tuition, whether it's for private school or college.

Age and Life Expectancy

Age is one of the most influential factors in determining life insurance rates. Younger people tend to pay lower premiums due to their longer life expectancy, while older individuals tend to pay higher premiums as the probability of death increases with age.

Health Status

In addition to age, your health status, medical history, and lifestyle choices can significantly impact your life insurance rates. Generally, the younger and healthier you are, the lower your premiums will be.

Lifestyle and Occupation

High-risk jobs, such as construction work, or participation in hazardous hobbies, such as skydiving, may result in higher life insurance premiums.

Type of Policy

The type of policy you choose, such as term life insurance or whole life insurance, will also affect your coverage amount and rates. Term life insurance is typically more affordable upfront, while whole life insurance offers coverage for your entire life at higher rates.

Employee Life Insurance: Voluntary Benefits for AD&D Protection

You may want to see also

Explore related products

![]()

High-risk activities

Life insurance rates are influenced by a variety of factors, including age, health, lifestyle choices, and the amount of coverage required. While age is a primary factor, with older applicants generally paying higher premiums, high-risk activities can also significantly impact the rates offered by insurers.

The frequency of participation in high-risk activities is a crucial factor. Individuals who engage in these activities occasionally may be viewed differently from those who do so regularly. For example, someone who skydives once a year may be considered lower risk than someone who does it every week. Therefore, reducing the frequency of high-risk activities can help lower insurance rates.

Certain occupations are inherently dangerous and may result in higher life insurance premiums or difficulty in obtaining coverage. Jobs with high mortality rates, such as working on an oil rig or in a mine, or in the military, pose a greater risk of injury or death. Insurers consider these factors when assessing an individual's risk profile, and it is essential for applicants to disclose any high-risk occupations.

In conclusion, high-risk activities encompass a wide range of pursuits, from extreme sports to specific occupations and even certain lifestyle choices. Engaging in these activities can result in higher life insurance rates or challenges in obtaining coverage. However, it is important to note that rates are highly personalized, and other factors such as age, health, and the amount of coverage also play a significant role in determining the final cost of life insurance.

Ulcerative Colitis: Life Insurance Considerations and Impacts

You may want to see also

Explore related products

![]()

Whole life insurance

The cost of whole life insurance depends on several factors, such as your age, health, gender, the policy design, and the amount of coverage. The younger and healthier you are, the less you'll pay for a permanent life policy. The bigger the death benefit, the higher the premium. Whole life insurance often costs more than term life insurance, but it may be worthwhile depending on your situation.

For example, a $500,000 whole life insurance policy costs an average of $440 to $451 per month for a 30-year-old non-smoker in good health. The same policy for a 35-year-old non-smoker in good health could cost between $542 and $708 per month, or approximately $6,500 to $8,500 per year. For a healthy, non-smoking 40-year-old, the typical cost of a $500,000 whole life insurance policy is $6,408 a year for men and $5,654 a year for women.

If you're looking to treat your life insurance policy as a cash asset, whole life insurance might be a good option. The cash value in a whole life policy is low-risk and low-return, but it grows at a predictable and steady rate. It's important to note that accessing the cash value in a whole life insurance policy reduces your death benefit, leaving less for your beneficiaries.

Life Insurance Payouts: Are They Counted as Assets?

You may want to see also

Explore related products

![]()

Term life insurance

The cost of term life insurance depends on several factors, including age, health, gender, lifestyle, and occupation. Younger people tend to pay less for term life insurance because they have a longer life expectancy and are less likely to have health problems. The cost of insurance tends to be more for males because they have shorter lifespans and are more likely to have dangerous jobs or lifestyles. However, it's important to note that each insurer has its own evaluation process, so it's advisable to compare quotes from multiple insurers.

To estimate how much term life insurance you need, you can use a life insurance calculator or a simple formula. One common method is to take your annual salary, add a "0" at the end, and that's your coverage amount. For example, if you earn $50,000 per year, you would aim for $500,000 in coverage. Another approach is to multiply your current income by 10 to 12, depending on your financial obligations and goals.

It's worth noting that term life insurance rates tend to increase with age, so purchasing a policy earlier can help lock in lower rates. Additionally, maintaining a healthy lifestyle, avoiding risky activities, and refraining from smoking can contribute to more favourable rates.

Health Insurance and Life Alert: What's Covered?

You may want to see also

Frequently asked questions

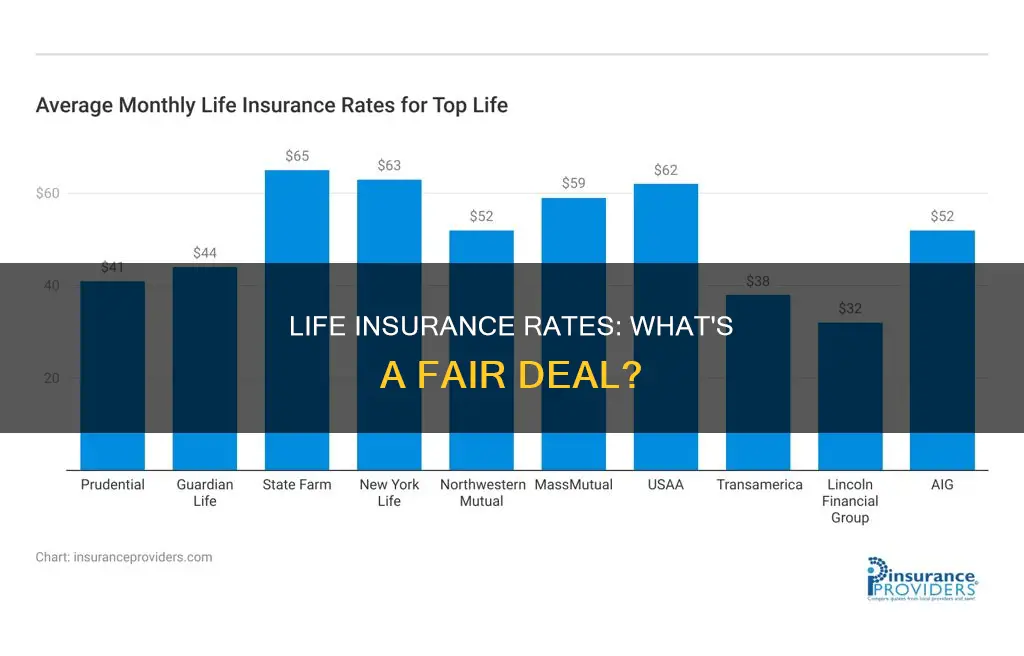

The average cost of life insurance is $26 a month. This is based on data for a 40-year-old buying a 20-year, $500,000 term life policy. However, life insurance rates can vary dramatically among applicants, insurers and policy types.

Age is one of the most influential factors affecting life insurance premiums. Younger people tend to pay lower rates than older people as the probability of death rises as we get older. It's best to apply for life insurance early, as the cost of a term life insurance policy is typically higher for someone who applies in their 40s or 50s compared to someone in their 20s or 30s.

Life insurance premiums are based primarily on life expectancy. The younger and healthier you are, the cheaper your premiums will be. If you have health issues such as diabetes, heart disease, or high blood pressure, you may have to pay higher premiums.

Your lifestyle and occupation can also impact your life insurance rates. People with high-risk jobs or hobbies may pay more in premiums. For example, a construction worker or a skydiver may pay higher rates. Additionally, if you smoke, you may pay more for life insurance due to being at higher risk for health issues.