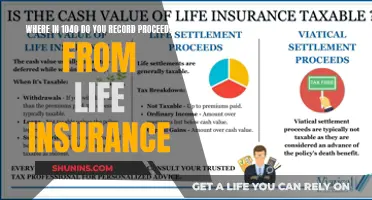

Life insurance proceeds are generally not taxable as income, but there are certain situations where taxes may be incurred. For example, if the beneficiary receives the payout in instalments, they will have to pay income tax on the interest accrued. This interest is reported to the Internal Revenue Service (IRS) by the insurance company. If the payout is a one-time payment, it is not taxed as income. However, if the policy was transferred for cash or other valuable consideration, the beneficiary may have to pay taxes on the proceeds. Additionally, if the beneficiary is anyone other than the spouse, the life insurance payout may be added to the value of the estate, and estate taxes may apply.

Explore related products

What You'll Learn

![]()

Interest on death benefits

The death benefit from a term life insurance policy is typically paid out in a lump sum. However, beneficiaries can choose to receive the benefit in installments. If the payout is spread over time, the beneficiary should be prepared to report the interest on their taxes. This interest is considered taxable income and must be reported to avoid penalties.

In some cases, a beneficiary may have to pay tax on any interest the policy accrued. This can occur when a policyholder leaves the death benefit to their estate instead of directly naming a person as the beneficiary. If the policyholder elects to delay the benefit payout and the money is held by the life insurance company for a given period, the beneficiary may have to pay taxes on the interest generated during that period.

It is important to note that life insurance premiums are typically not tax-deductible for personal policies. However, if you gift a life insurance policy to a charity and continue to pay the premiums, those payments are generally considered charitable donations and may be tax-deductible.

BNS Scotia Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Withdrawals from universal life insurance policies

Universal life insurance is a type of permanent life insurance that combines a death benefit with an investment savings element. The cash value of a universal life insurance policy is generally non-taxable while it remains in the policy. This allows the cash value to grow without the policyholder having to pay any tax bills. However, if you decide to withdraw cash, take out a loan, or surrender your policy, you might face some tax liabilities.

It's important to note that taking out a loan from your universal life insurance policy usually won't result in a taxable event. However, if your policy is a Modified Endowment Contract (MEC), loans are treated as withdrawals and may be subject to ordinary income taxes. Additionally, if you surrender your policy, any accumulated cash value you receive is usually tax-free up to the amount of total premiums paid. However, any gains may be taxed as income.

While life insurance proceeds received by a beneficiary due to the death of the insured are generally not considered taxable income, any interest earned on those proceeds is taxable and should be reported. This includes situations where the death benefit is paid out in installments, as the interest that accumulates on those payments will be taxed as regular income. Therefore, it is important for beneficiaries to be aware of the potential tax implications when receiving life insurance proceeds and to accurately report any interest earned during tax season.

Life Insurance Medical Exam: Does a Nurse Visit Your Home?

You may want to see also

Explore related products

![]()

Dividends from mutual insurance companies

Life insurance dividends are considered a return of premium and are generally not taxed. However, the way you choose to use your dividends may impact their tax status. For example, if you use your dividends to buy additional paid-up life insurance, this will typically be tax-deferred. On the other hand, if you choose to receive your dividends as a cash payment, this can help reduce what you owe on your policy each year. In this case, dividends themselves are not taxed, but any interest earned on those dividends is considered taxable income and must be reported.

According to the IRS, if you receive life insurance proceeds as a beneficiary due to the death of the insured person, you generally do not need to include this in your gross income or report it on your income taxes. However, any interest received on top of the benefit is taxable and should be reported as interest received. This also applies to interest accumulated on instalment payments of a death benefit.

In the case of mutual insurance companies, taxable income is determined by subtracting total losses from gross receipts. Deductions are allowed for depreciation, interest on indebtedness, and capital losses. These deductions are typically identical to those allowed for other corporations. Mutual insurance companies can also take special deductions as outlined in Section 822(c)(7).

Term vs Life Insurance: Which Policy is Best?

You may want to see also

Explore related products

![]()

Modified endowment contracts

Generally, the proceeds from a life insurance policy that you receive as the beneficiary are not considered gross income and do not have to be reported on your income taxes. However, any interest earned is taxable and should be reported. This includes interest accumulated on installment payments of a death benefit.

One key feature of MECs is their tax treatment. Unlike traditional endowment policies, where the investment growth within the policy is tax-deferred, MECs are taxed differently. According to the IRS, any distributions or withdrawals made from a MEC are taxed as ordinary income to the extent of the policy's gain. This means that the policyholder will be required to pay taxes on the investment earnings within the policy when they take money out. The taxation of distributions from a MEC is similar to that of a non-qualified annuity, where the earnings are taxed at the policyholder's ordinary income tax rate.

It's important to note that the rules and regulations regarding MECs can be complex, and there may be specific requirements or exceptions depending on the policy and the policyholder's circumstances. Additionally, the tax laws and regulations can change over time, so it's always advisable to consult with a tax professional or financial advisor for the most up-to-date information and personalized advice. By understanding the tax implications and planning accordingly, policyholders can make informed decisions about their MECs and maximize their tax benefits.

Life Insurance Payouts: Lump Sum Benefits Explained

You may want to see also

Explore related products

![]()

Estate and inheritance taxes

Life insurance proceeds are generally not subject to estate or income tax. However, there are certain scenarios where taxes may be incurred.

If the beneficiary of a life insurance policy is an estate rather than an individual, the person or persons inheriting the estate may have to pay estate taxes. This is because the death benefit from the life insurance policy is included in the value of the estate, increasing the estate's value and potentially subjecting it to higher estate taxes.

To avoid this, one strategy is to transfer ownership of the life insurance policy to another person or entity. This removes the proceeds from the taxable estate, as the proceeds are not considered part of the estate if the beneficiary is an individual. However, it is important to note the three-year rule, which states that gifts of life insurance policies made within three years of death are still subject to federal estate tax. Therefore, careful planning is necessary to ensure compliance with this rule.

Another strategy to reduce potential estate taxes is to set up an irrevocable life insurance trust (ILIT). By transferring ownership of the life insurance policy to an ILIT, the proceeds are not included as part of the estate. This allows the original owner to maintain some legal control over the policy and ensures that all premiums are paid promptly.

In addition, beneficiaries can minimize taxes by taking the payout as a lump sum instead of receiving it in installments. While the death benefit itself is typically not taxed, any interest that accumulates on installment payments will be taxed as regular income. Therefore, by taking a lump sum payout, beneficiaries can avoid paying taxes on the interest accrued.

Congresswoman Omar's Nay Vote on Life Insurance Payouts Explained

You may want to see also

Frequently asked questions

Life insurance proceeds are typically not taxable as income, but can be taxed as part of your estate if the amount being passed to your heirs exceeds federal and state exemptions.

Yes, any interest earned on life insurance proceeds is taxable and should be reported.

If you receive the life insurance proceeds as a series of installments, the insurer will typically pay interest on the outstanding death benefit, which is taxable.

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)