Permanent life insurance is a type of insurance that doesn't expire and offers lifelong coverage. It also includes a cash value component that increases over time and can be used to borrow money, pay premiums, or withdraw funds. Because permanent life insurance offers more benefits and coverage than term life insurance, it tends to be more expensive. The cost of permanent life insurance is influenced by various factors, including age, health, coverage amount, tobacco use, occupation, and hobbies. It also offers tax benefits, such as tax-deferred cash value growth and income tax-free death benefits. Additionally, permanent life insurance policies provide more riders and customization options, which can increase the cost. Overall, the fees associated with permanent life insurance are higher due to the comprehensive nature of the coverage and the potential for long-term financial gains.

| Characteristics | Values |

|---|---|

| Permanent life insurance lasts a lifetime | Permanent life insurance is a type of life insurance that doesn't expire, no matter how long you live |

| Cash value component | Permanent life insurance includes a cash value component that builds over time and can be used to borrow money, withdraw cash, or pay premiums |

| Tax benefits | The cash value of a permanent life insurance policy grows tax-deferred, and the death benefit is typically paid out income tax-free |

| Higher premiums | Permanent life insurance premiums are higher than term life insurance due to increased coverage and benefits |

| Complexity | Permanent life insurance has more rules, features, and fees than term coverage, including variable cash value interest rates, investment options, and adjustable payments |

| Limited investment flexibility | With whole life and universal life policies, you cannot change how your cash value is invested |

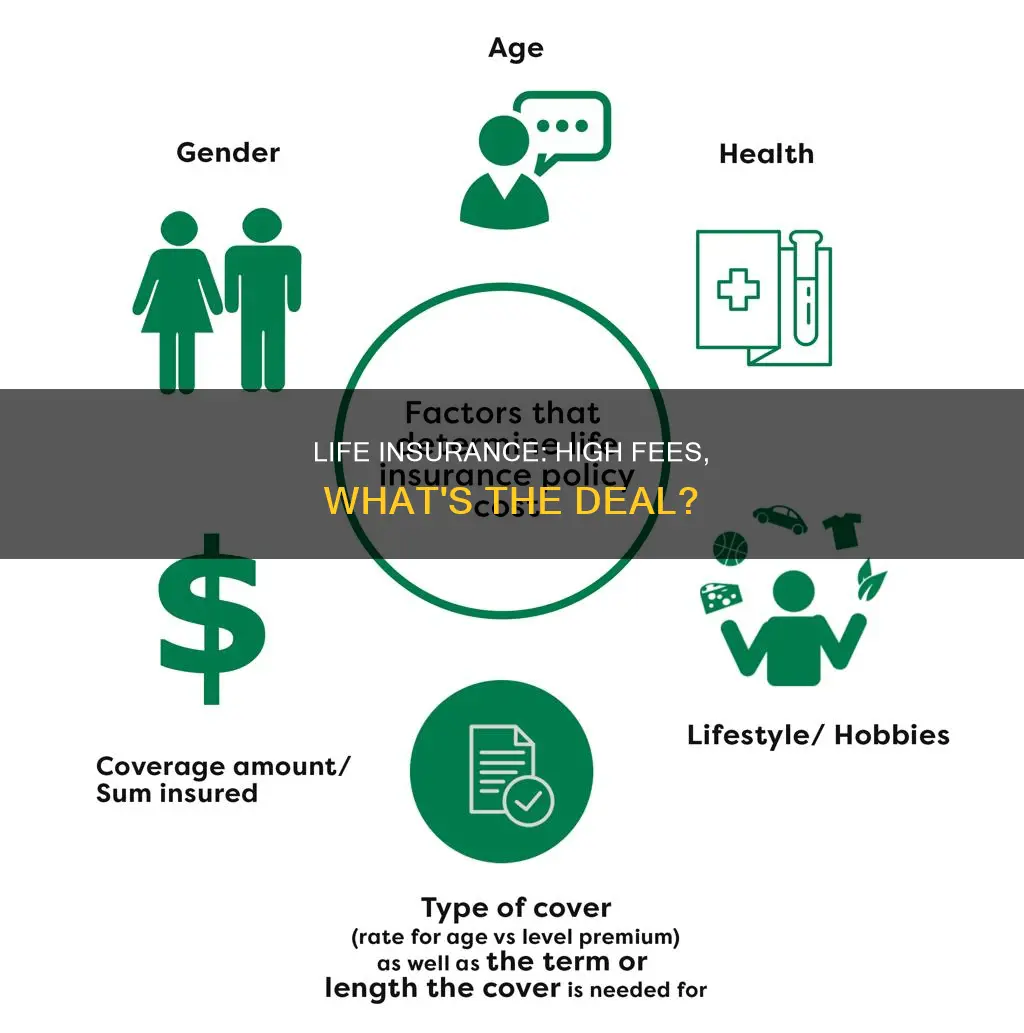

| High-risk hobbies and occupation | Engaging in high-risk activities and having a hazardous or high-risk job can result in higher premiums |

| Age | Younger individuals are considered lower risk and can secure lower premiums |

| Health | Insurers consider height, weight, medical history, and chronic or serious illnesses when determining premiums |

| Tobacco use | Life insurance for smokers typically has higher rates due to associated medical conditions |

| Coverage amount | Choosing a higher death benefit results in higher premiums |

Explore related products

What You'll Learn

![]()

Permanent life insurance has a cash value component

Permanent life insurance is a type of insurance that doesn't expire, no matter how long you live. It is designed to cover a lifetime of different possibilities and typically offers more riders and customisation than term life insurance. Permanent life insurance has a cash value component that increases in value over time, becoming an asset you can use to borrow money, withdraw cash, or even pay your premium. This cash value component is one of the reasons permanent life insurance costs so much.

The cash value of a permanent life insurance policy grows tax-deferred, meaning that policyholders won't have to pay taxes on the gains until they withdraw them. This allows the cash value to accumulate more efficiently over time. The money in your cash value isn't taxed as it grows, so it has the potential to grow faster. It usually takes a few years for the cash value to grow into a usable sum, but once that happens, it becomes a financial asset with many advantages. The death benefit of a permanent life insurance policy is typically paid out income tax-free to beneficiaries, ensuring that your loved ones receive the full amount without any tax deductions. Policyholders can also take out loans against the cash value of their policy, providing a source of tax-efficient funds for various financial needs.

The market interest rates determine a policy's cash value, so the amount earned could change each year. Whole life insurance policies offer guaranteed cash value growth and fixed premiums, while universal life insurance policies are more flexible, allowing you to adjust your premiums each year. Variable life insurance is more expensive due to the investment component, which also introduces higher investment risk. With variable life insurance, you can invest your cash value in sub-accounts, similar to mutual funds, representing different investment strategies such as equity, bond, or balanced funds. Your return may be higher if your investments do well, but if they perform poorly, your return will be lower, and you could even lose money.

The cash value component of permanent life insurance is appealing to high-net-worth individuals looking for a tax-advantaged investment vehicle. For example, someone who has maxed out other tax-deferred investment options like IRAs and 401(k)s might use a permanent life insurance policy as an additional way to grow their wealth. Permanent life insurance can also be beneficial for individuals with long-term dependents, such as those with special needs children or elderly parents, as it provides long-term financial planning with security and investment benefits.

Trustee and Beneficiary: Can One Person Play Both Roles?

You may want to see also

Explore related products

![]()

It offers lifelong coverage

Permanent life insurance is a good option for anyone who wants lifelong coverage and a cash value component. Permanent life insurance policies are designed to cover a lifetime of different possibilities, and as such, they offer several benefits that term life insurance does not.

Firstly, permanent life insurance offers a death benefit that is typically paid out income tax-free to beneficiaries, ensuring that your loved ones receive the full amount. Secondly, permanent life insurance policies offer a cash value component that grows tax-deferred, allowing policyholders to access tax-efficient funds for various financial needs. This cash value is a financial asset that can be used to borrow money or withdraw cash, and it can also be used to pay premiums. The cash value component also means that permanent life insurance can be used to fund buy-sell agreements, provide key person insurance, and offer employee benefits, making it a useful tool for business owners.

Additionally, permanent life insurance policies offer more riders and customization options than term life insurance. Riders are optional provisions that give added protection and benefits, such as a waiver of premium rider, which pays your premium if you become disabled and can no longer work. The ability to customize your policy means that permanent life insurance can be adapted to diverse needs and situations, such as providing lifelong financial support for a child with special needs.

Finally, permanent life insurance can be a good option for high-net-worth individuals looking for a tax-advantaged investment vehicle. The cash value component of permanent life insurance can be used to grow wealth, pay estate taxes, provide liquidity for heirs, and offer a tax-efficient way to transfer wealth.

Whole Life Insurance: Is It a Safe Bet?

You may want to see also

Explore related products

![]()

It has higher premiums

Permanent life insurance policies have higher premiums than term life insurance policies. This is because permanent life insurance policies are designed to cover a lifetime of different possibilities and offer more riders and customisation. Riders are optional provisions that give added protection and benefits to the policyholder. Permanent life insurance policies typically offer more riders, and each rider comes with an additional cost. Examples of riders include a waiver of premium rider, which allows you to pause your premiums if you become disabled, and a child term rider, which provides coverage for your children.

Permanent life insurance policies also have higher premiums because they offer a cash value component that increases in value over time. This cash value feature is an asset that policyholders can use to borrow money, withdraw cash, or even pay their premium. The cash value of a permanent life insurance policy grows tax-deferred, meaning that policyholders won't have to pay taxes on the gains until they withdraw them. This allows the cash value to accumulate more efficiently over time. The cash value component also makes permanent life insurance policies more expensive because it allows policyholders to take out loans against the cash value of their policy, providing a source of tax-efficient funds for various financial needs.

The higher premiums of permanent life insurance policies are also due to the fact that they offer lifelong coverage. Permanent life insurance policies do not expire, no matter how long the policyholder lives, whereas term life insurance policies last a set number of years. Because of the potentially longer coverage period, permanent life insurance policies have higher premiums. Additionally, permanent life insurance policies have higher premiums because they offer guaranteed cash value growth and fixed premiums. Whole life insurance rates tend to be higher than universal life insurance rates because whole life insurance offers fixed premiums and death benefit amounts, while universal life insurance offers more flexibility.

The age of the policyholder also affects the premium, with younger individuals typically resulting in lower premiums since they are considered lower risk. Other factors that influence the premium include the policyholder's health, coverage amount, tobacco use, occupation, and hobbies. Engaging in high-risk hobbies, such as skydiving, can result in higher premiums. Overall, permanent life insurance policies have higher premiums because they offer more benefits, features, and flexibility than term life insurance policies.

VA's Right to Recover: Resident's Life Insurance

You may want to see also

Explore related products

![]()

It has more riders and customisation

Permanent life insurance policies are designed to cover a lifetime of different possibilities. They offer more riders and customisation options than term life insurance policies. Riders are extra benefits that a policyholder can buy to add on to a life insurance policy. They allow you to customise your coverage and enhance your protection against unforeseen disasters.

There are several types of riders that can be added to a permanent life insurance policy. One example is the waiver of premium rider, which will pay your entire premium if you become disabled and are unable to work, allowing you to keep your policy in effect. A similar rider is the waiver of cost of insurance, which only pays the death benefit portion of your premiums, not the cash value portion. Another example is the accelerated benefit rider, which allows you to access a portion of the death benefit while you are still alive if you become terminally or chronically ill.

Other common riders include the accidental death rider, which offers extra payouts over the basic sum assured in case of death resulting from accidents, and the disability rider, which provides payouts if you become permanently disabled and unable to work. The critical illness rider is another valuable addition, as it disburses payments when you are diagnosed with a serious disease, protecting your family from the high expenses involved in the care of such illnesses.

In addition to these, there is the family income benefit rider, which provides a steady flow of income to family members if the insured dies, and the child term rider (also known as the child protection rider), which provides coverage for the policyholder's children. This rider can help cover the unexpected costs associated with a child's death, such as funeral and burial expenses, and can be converted into a permanent life insurance policy when the child reaches adulthood.

The cost of these riders will vary depending on the added coverage or benefits they provide. While some riders may come with additional costs, most are relatively low in price as they involve minimal underwriting and are less likely to be used by the insured. It's important to carefully consider your unique situation and choose the riders that provide the proper financial protection for yourself and your family.

Who Can Witness and Sign Life Insurance Documents?

You may want to see also

Explore related products

![]()

It has tax benefits

Permanent life insurance is a good option for anyone who wants lifelong coverage and a cash value component. It has several tax benefits that can help policyholders save money and maximise their coverage.

Firstly, permanent life insurance offers tax-deferred cash value growth. This means that the cash value of a policy grows tax-deferred, and policyholders don't have to pay taxes on the gains until they withdraw them. This allows the cash value to grow more efficiently over time. The money in your cash value is also not taxed as it grows, so it has the potential to grow faster.

Secondly, permanent life insurance provides an income tax-free death benefit. This means that the death benefit is typically paid out to beneficiaries income tax-free. This ensures that loved ones receive the full amount of the death benefit without any tax deductions.

Thirdly, policyholders can take out tax-efficient loans against the cash value of their policy. This can provide a source of funds for various financial needs, such as college fees for a child, a property down payment, or cash to use in retirement. It's important to note that the insurer will charge interest on these loans, and if the loan plus interest exceeds the total cash value, the policyholder would need to pay more into the policy or risk it lapsing.

Finally, permanent life insurance can be used to reduce tax obligations on other income. For example, if you wish to donate money to charities, you could reduce your income tax by signing over some of the benefits of your policy and naming the charity as a beneficiary. Additionally, permanent life insurance can be used to pay estate taxes, provide liquidity for heirs, and transfer wealth in a tax-efficient manner.

While permanent life insurance offers these tax benefits, it's important to consider that the fees associated with this type of insurance are generally higher than those of term life insurance due to the additional benefits and longer coverage period.

Universal Life Insurance: Converting to Term – Is it Possible?

You may want to see also

Frequently asked questions

Permanent life insurance fees are high because the coverage doesn't expire and the policy has a cash value component that increases in value over time. This cash value is also tax-advantaged, allowing it to grow faster. Additionally, permanent policies often have more rules, features, and fees than term coverage, and they usually offer more riders and customization.

Permanent life insurance is more expensive because it provides more benefits and can be used in ways that term life insurance cannot. It often has variable cash value interest rates, investment options, and the ability to adjust your payments, which requires paying more attention to your policy. The premiums are also influenced by age, gender, health, tobacco use, and occupation.

Permanent life insurance is beneficial for high-net-worth individuals as it provides a tax-advantaged investment vehicle. It can be used to pay estate taxes, provide liquidity for heirs, and offer a tax-efficient way to transfer wealth. The cash value component of permanent life insurance can be an attractive way to grow wealth for those who have maxed out other tax-deferred investment options.