Turning 18 is an exciting milestone, but it can also bring new financial challenges, especially when it comes to car insurance. Many 18-year-olds are often classified as high-risk due to their limited driving experience, resulting in higher insurance premiums. This is further influenced by factors such as gender, location, and driving history. While it may be tempting to opt for a cheaper used car, insurance rates for teenagers can still be staggering, often reaching hundreds of dollars per month. So, what's driving these high insurance costs for 18-year-olds, and are there ways to keep costs down?

Explore related products

What You'll Learn

![]()

Insurers classify 18-year-olds as high-risk due to limited driving experience

Insurance companies often classify 18-year-olds as high-risk due to their limited driving experience, which leads to higher premiums. This classification is based on statistical data showing that younger drivers are more likely to be involved in accidents or receive citations. The lack of experience on the road increases the chances of making mistakes, such as failing to check blind spots or driving too fast, which are common causes of accidents and insurance claims. As a result, insurance companies must account for the added risk by charging higher premiums to inexperienced drivers.

In addition to limited driving experience, other factors contribute to insurers' perception of 18-year-olds as high-risk. Young drivers are statistically more prone to engaging in risky behaviours such as street racing, driving under the influence, or other reckless activities. These behaviours further increase the likelihood of accidents and claims, impacting insurance rates.

While age is a significant factor, it is not the sole determinant of insurance costs. An 18-year-old's gender can also influence their insurance premium, with young males often considered higher-risk due to statistical tendencies toward riskier behaviour. Additionally, factors like location and credit score can impact insurance rates. For example, residing in a high-risk area or having a low credit score can result in higher premiums.

It is worth noting that insurance rates are not static and tend to decrease as individuals get older. Significant drops in insurance costs typically occur at ages 21 and 25, as the risk associated with younger drivers decreases over time. Maintaining good grades and a clean driving record can also help mitigate the high insurance costs often faced by 18-year-olds.

To find the most affordable insurance options, 18-year-olds should compare quotes from different insurance providers. Some companies, such as USAA, American Family, and GEICO, are known for offering competitive rates for younger drivers. Additionally, adding an 18-year-old to an existing family policy can often be more affordable than them purchasing their own policy.

Smart Strategies for Shopping Auto Insurance

You may want to see also

Explore related products

![]()

Male teens are a much higher risk to insurance companies

The cost of car insurance for young drivers, especially males, can be very high. This is due to a variety of factors, including inexperience, high-risk behavior, and the potential for accidents. Male teens, in particular, are considered a much higher risk for insurance companies due to statistical tendencies toward riskier behavior.

Insurers often classify 18-year-olds as "high-risk" due to their limited driving experience. Statistically, younger drivers are more likely to be involved in accidents or receive citations, leading to higher premiums than more experienced drivers. Male teens are seen as more prone to accidents and poor decision-making, which increases the potential cost of claims for insurance companies. This added risk results in higher premiums when insuring teenage males.

Additionally, male teens may have lower credit scores, which can also affect insurance rates. Insurers may consider an individual's history of paying bills and handling debt when determining premiums. A poor credit score can indicate higher levels of risk, leading to higher insurance costs.

The specific car model can also impact insurance rates. Certain vehicles are associated with higher accident rates or are more popular among ""drifters," resulting in elevated insurance premiums. Male teens may be attracted to these riskier car models, further contributing to their higher insurance costs.

While it may be challenging for male teens to obtain affordable insurance, there are a few ways to mitigate the costs. Maintaining good grades and enrolling in driver's education programs can help demonstrate responsibility and lower premiums. Additionally, being added to a parent's existing policy is usually more affordable than obtaining a separate policy.

As male teens gain more driving experience and age, their insurance rates will typically decrease. The risk associated with younger drivers reduces over time, leading to lower premiums.

Tipping Auto Insurance Agents: Christmas Custom or Not?

You may want to see also

Explore related products

![]()

It's cheaper for 18-year-olds to share car insurance with their parents

Car insurance for 18-year-olds is generally pretty expensive, with an average annual rate of $7,367 per year for full coverage. This is because young drivers are seen as more prone to accidents due to their inexperience, making them riskier clients for insurers. This added risk leads to higher premiums when insuring teen drivers.

However, if your teen lives with you and your name is also on their vehicle, they will likely save money by staying on your policy. Teens can save anywhere from $503 to $3,163, on average, by staying on a parent's policy. Parents who add a driver under the age of 21 to their auto policy see an average premium increase of $2,411 per year, which is still more affordable than the alternative.

Additionally, there are plenty of car insurance discounts available for teen drivers. For example, most companies offer discounts to students with good grades, generally a B average or higher. USAA, Nationwide, and Geico offer the cheapest car insurance for teens on a parent's policy.

Furthermore, having your entire household on one policy could make it easier for you to make changes, pay bills, and keep track of your insurance documents. It is important to note that once your child turns 18, they will have the option to get their own car insurance, but this is typically not the most affordable or practical option.

Driver Insurance: A Compulsory Coverage for All Motorists?

You may want to see also

Explore related products

![]()

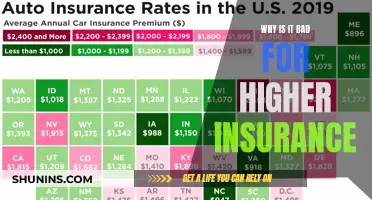

Location impacts insurance rates

Additionally, your location can also affect your insurance rates through its associated risks. For example, if you live in an area prone to natural disasters such as hurricanes, floods, or wildfires, your insurance rates will reflect the increased risk of damage to your vehicle. Similarly, if you live in an area with a high crime rate, your insurance costs may be higher due to the increased risk of theft, vandalism, or accidents.

The impact of location on insurance rates is also influenced by state and local regulations. Each state has different laws and requirements regarding insurance, which can affect the cost of coverage. For example, some states may mandate certain minimum levels of coverage, which can drive up the cost of insurance for residents.

Furthermore, your location can also determine the cost of repairs and the availability of replacement parts. If you live in a remote area, the cost of towing and repairs may be higher, which can be reflected in your insurance rates. Additionally, if your vehicle requires specialized parts that are not readily available in your area, the insurance company may factor in the additional cost and time required to source those parts.

Finally, your location can also impact the cost of doing business for insurance companies. Overhead costs, such as rent and employee salaries, tend to be higher in certain areas, and these costs are often passed on to customers in the form of higher insurance premiums. Therefore, it is important to consider not only the inherent risks of a particular location but also the operational costs for insurance providers when understanding how location influences insurance rates.

Launching Your Own Auto Insurance Company

You may want to see also

Explore related products

![]()

Driving history impacts insurance rates

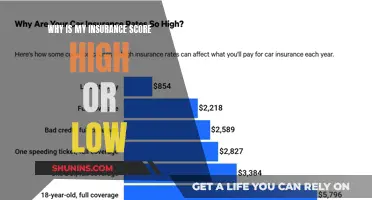

Insurance companies consider an individual's driving record to be the most crucial factor when determining auto insurance rates. A driver with a clean record in the United States typically pays around $135 to $175 per month for full coverage car insurance. However, a single violation or incident on a driving record can lead to significantly higher insurance rates. For example, a speeding ticket can increase rates by up to 21% to 49% depending on the state, while a single at-fault accident can raise premiums by about 34% to 43%.

More severe incidents, such as driving under the influence (DUI) convictions, have an even greater impact on insurance rates. A DUI conviction can increase insurance rates by 50% to 92%, or even more in some states. For example, in North Carolina, auto insurance rates can increase by about 325% after a DUI conviction, while in Texas, rates increase by 40%. On average, drivers with a DUI pay around $203 per month for insurance, which is nearly double the cost for a regular policyholder.

The time incidents stay on a driving record varies by state, typically ranging from three to five years. During this period, drivers with incidents on their record can expect to pay higher insurance rates. In addition to the type of incident, the number of incidents on a driving record can also impact insurance rates. Insurance companies consider customers with multiple violations and incidents to be high-risk drivers, and therefore charge higher rates to offset the increased risk of claims.

While a perfect driving record is ideal for keeping insurance rates low, there are other factors that can influence insurance rates, such as age, location, credit score, and level of education. These factors can help insurance companies assess the risk level of a driver and determine the appropriate premiums. By considering these factors and maintaining a clean driving record, drivers can work towards obtaining the lowest possible insurance rates.

Auto Insurance in Ohio: Minimum Coverage Requirements Explained

You may want to see also

Frequently asked questions

Insurance companies often classify 18-year-olds as "high-risk" due to their limited driving experience and driving history. Statistically, younger drivers are more likely to be involved in accidents or receive citations, leading to higher premiums than more experienced drivers.

You can lower your insurance rate by being added to an existing policy, which is usually more affordable than having your own policy. Maintaining good grades and a clean driving record can also help lower your insurance rate.

The average car insurance rate for an 18-year-old is $514 per month or $6,168 per year. However, this can vary depending on factors such as gender, location, and driving history.