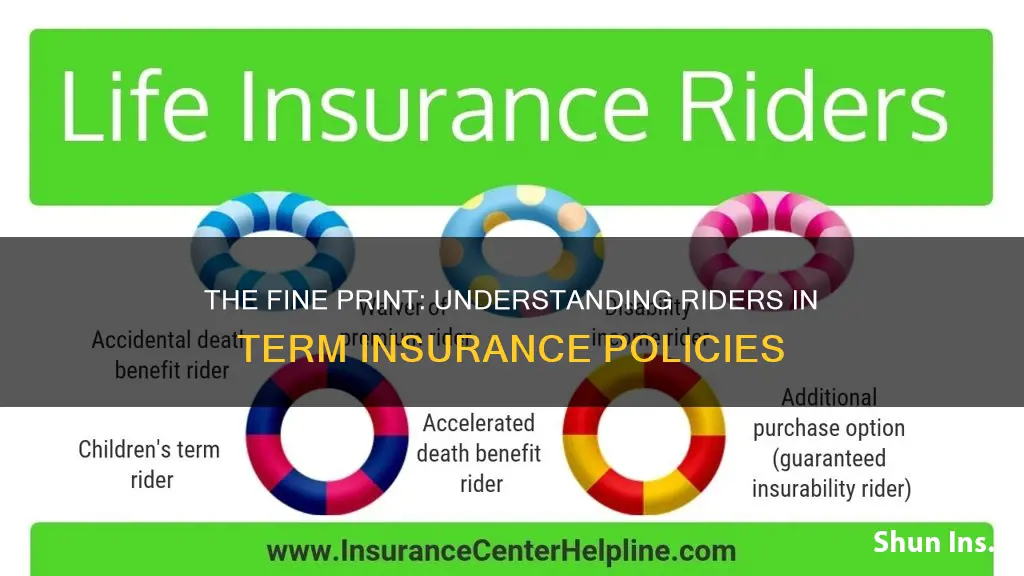

Riders are additional benefits that can be added to a basic term insurance policy. They are optional and provide extra protection or features beyond the core offering of a death benefit. The cost of adding a rider is usually low because it involves minimal underwriting. Riders can be added to enhance the coverage of a term insurance policy, making it more comprehensive and customisable.

| Characteristics | Values |

|---|---|

| Definition | Additional benefits or coverage that can be added to a basic term insurance policy |

| Purpose | To enhance the plan's base coverage and provide protection against a range of eventualities |

| Types | Accidental Death Benefit Rider, Accidental Total and Permanent Disability Benefit Rider, Critical Illness Rider, Waiver of Premium Rider, Terminal Illness Rider, HospiCare Benefit Rider, Income Benefit Rider, Long-Term Care Rider, etc. |

| Cost | Comes at an extra cost on top of the premiums for the policy |

| Customization | Allows policyholders to customize their term insurance policy according to their specific needs |

| Flexibility | Offers flexibility in adjusting coverage as needs change over time |

| Peace of Mind | Provides added reassurance that you and your loved ones are financially protected against a variety of risks |

Explore related products

What You'll Learn

![]()

Accidental Death Rider

An accidental death rider is an optional add-on that can be purchased in addition to a term life or whole life insurance policy. This rider provides financial protection to beneficiaries in the event of the policyholder's death due to an accident. It is one of the most affordable riders, offering ample life coverage.

The accidental death rider pays out an additional amount of the death benefit if the insured dies as a result of an accident. Typically, the additional benefit paid out is equivalent to the original policy amount, doubling the benefit. This is why the rider is also called a double indemnity rider.

For example, if the policyholder has a term life insurance policy with a death benefit of Rs 1 crore and an accidental death benefit rider of Rs 10 lakh, and they pass away in an accident during the policy term, the family will receive a total sum of Rs 1.1 crore. It is important to note that even if the insured person dies from something other than an accident, the base sum assured will still be paid out.

The accidental death benefit rider is a good option for those who travel frequently or work in hazardous conditions. It provides an extra layer of financial protection for the policyholder and their family in the event of an unforeseen accident.

It is important to understand the restrictions and exclusions associated with the accidental death rider. Many insurance companies have specific definitions of what constitutes an "accident", and there may be exclusions for certain activities or circumstances such as adventure sports, aviation accidents, or death due to drug or alcohol overdose.

Understanding Renewable Term Insurance: Unraveling the Benefits and Mechanics

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Waiver of Premium Rider

A waiver of premium rider is an optional add-on to a life insurance policy that waives premium payments if the policyholder becomes critically ill, seriously injured, or physically impaired. This rider ensures that the policy remains active even if the policyholder can no longer afford the premiums.

The waiver of premium rider is particularly useful if an injury or illness prevents the policyholder from working. It is important to note that the rider only comes into effect if the policyholder is disabled for a specific period, often six months or more. The exact definition of "total disability" may vary depending on the insurance provider but generally refers to the policyholder's inability to work in their regular occupation or any other occupation suited to their education, training, or experience.

The cost of adding a waiver of premium rider varies depending on factors such as age, health, policy type, and the insurance provider. It typically increases the premium by 10% to 25%. The rider can be purchased at the time of policy inception, and the claim under the rider can be triggered only once. To activate the rider, policyholders may need to submit a claim with supporting documentation, including a statement from their doctor and a notice from the Social Security Administration (SSA).

The waiver of premium rider offers several benefits, including financial security during difficult times, peace of mind, and protection against policy lapse. However, it is important to consider potential drawbacks, such as additional costs, waiting periods, specific definitions of qualifying disabilities, and duration limits.

In conclusion, a waiver of premium rider can provide valuable financial protection by ensuring that life insurance policies remain active during periods of disability or critical illness. However, it is essential to carefully review the terms, conditions, and exclusions of the rider before purchasing it.

Understanding the Role of Short-Term Insurance in Meeting FRS Requirements

You may want to see also

Explore related products

![]()

Family Income Benefit Rider

A family income benefit rider is an optional add-on to a term life insurance policy. It provides the beneficiary with an amount of money equal to the policyholder's monthly income in the event of their death. This type of rider is particularly useful for individuals who are the sole breadwinners of their families.

Here's how it works: when you purchase a family income rider, you'll pay a monthly premium to ensure that your beneficiaries receive a monthly payout after your death for the remaining length of the policy's term. You can select a monthly payout amount equivalent to your monthly wages, so that your income is replaced if you pass away unexpectedly.

For example, let's say you purchase a family income rider for your term life policy that lasts until you plan to retire at 60. Unfortunately, you pass away unexpectedly at age 45. The family income rider will then make monthly payments to your spouse in the amount you specified for 15 years. At that point, the monthly payments will stop, and your spouse may receive the remaining death benefit as a lump sum.

Family income riders are often affordable and sometimes included in term policies at no extra cost. However, it's important to note that they may increase your monthly premium, and there may be a specification that the beneficiary must activate the rider within a certain time frame.

Understanding the Complexities of Extended Term Insurance Calculations

You may want to see also

Explore related products

![]()

Critical Illness Rider

A critical illness rider is an add-on benefit that can be purchased with a term insurance plan. This rider provides additional coverage in the event that the policyholder is diagnosed with a critical illness during the policy term. The list of covered critical illnesses varies by insurer but typically includes major illnesses such as cancer, heart attack, stroke, kidney failure, and paralysis.

When a policyholder with a critical illness rider is diagnosed with a covered critical illness, they receive a lump-sum payout, which can be used to cover medical expenses and other costs associated with the illness. This rider helps to ensure financial stability for the policyholder and their family during a difficult time.

The cost of adding a critical illness rider to a term insurance plan is generally affordable and can provide peace of mind, knowing that financial support is available if a critical illness occurs. It is important to note that the rider only pays out once, and there may be a waiting period before the benefit can be claimed.

In summary, a critical illness rider offers valuable protection against the financial impact of a critical illness, providing a lump-sum payout to help cover expenses. This rider is a cost-effective way to enhance the coverage of a term insurance plan and provide additional support during a challenging time.

The Renewal Riddle: Unraveling the Mystery of Level Term Insurance

You may want to see also

Explore related products

![]()

Long-Term Care Rider

A long-term care rider is a living benefit that can be added to a life insurance policy. It allows the policyholder to access their death benefit early to pay for long-term care needs, such as nursing home care or home health services. This type of rider is typically only available for whole and universal life insurance policies and comes at an additional cost, increasing the premium.

To qualify for a long-term care rider, a medical professional must certify that the policyholder is unable to perform at least two activities of daily living (such as eating, bathing, and dressing) or that they require substantial supervision due to cognitive impairment. There is usually a waiting period of around 90 days before benefits can be accessed.

The benefits received through a long-term care rider reduce the policy's death benefit, leaving beneficiaries with a smaller payout. However, if the long-term care benefits are not used, the policy pays out a full death benefit. Long-term care riders on life insurance policies are often more affordable than standalone long-term care policies.

The Truth About Term Insurance: Unraveling the Mystery of Surrender and Refund Values

You may want to see also

Frequently asked questions

A rider is an additional benefit or coverage that you can add to your basic term insurance policy. Riders provide extra protection or features beyond the basic coverage offered by the term plan.

Adding riders to a term insurance policy can provide enhanced coverage, customisation, cost-effectiveness, comprehensive protection, flexibility, and peace of mind.

Some common types of riders include accidental death rider, accidental disability rider, critical illness rider, terminal illness rider, and waiver of premium riders.

The cost of riders varies depending on factors such as the sum assured, age of the policyholder, policy term selected, and payment term. Generally, riders are relatively low in cost as they involve minimal underwriting.

Riders can typically be added at the time of purchasing the policy or at the policy anniversary, depending on the policy details. Consult your insurance agent or advisor to determine the specific riders available and suitable for your term insurance plan.