Appealing an insurance bill can be a long and frustrating process, but there are ways to make it more manageable. Firstly, it is important to stay organised and keep a record of all relevant information, including names, phone numbers, and notes from conversations with insurance providers. Secondly, understanding your insurance policy and knowing what is covered is crucial. This means reviewing your policy documents and identifying any discrepancies between what is covered and what you are being charged for. Thirdly, communicating effectively with both the insurance provider and the medical provider is key. It is important to remain polite and empathetic throughout the process, as this can increase the chances of a positive outcome. Finally, if you are unable to resolve the issue on your own, there are external resources available, such as medical billing advocates or state insurance commissioners, who may be able to assist you in appealing the insurance bill.

Explore related products

What You'll Learn

- Contact your medical provider to inform them of your plan to appeal the denial and work with them to handle any outstanding bills

- Delay paying the bill until you know the outcome of your appeal

- Set up a payment plan and try to negotiate the amount owed

- File an internal appeal by completing all required forms and submitting any additional information for the insurer to consider

- If your internal appeal is denied, you can file for an external review

![]()

Contact your medical provider to inform them of your plan to appeal the denial and work with them to handle any outstanding bills

Contacting your medical provider and informing them of your plan to appeal a denial is a crucial step in resolving outstanding bills. Here are some detailed steps and strategies to effectively handle this situation:

- Initiate Contact with Your Medical Provider's Office: Reach out to the billing department or administrative staff of your medical provider. Be sure to have your relevant medical records and billing statements on hand when making contact. It is essential to be proactive and initiate this conversation as soon as possible.

- Communicate Your Intent to Appeal: Clearly express your intention to appeal the denial of your insurance claim. Explain the situation and provide them with a copy of the denial letter from your insurance company. It is important that your medical provider is aware of your efforts to resolve the issue.

- Request Their Cooperation: Ask your medical provider to work with you in handling the outstanding bills. Emphasize the importance of their support and collaboration in navigating the appeals process. Their cooperation can make a significant difference in the outcome.

- Discuss Billing Options: Depending on your specific circumstances, there are several approaches you can consider:

- Delay Payment: If possible, request your medical provider's office to delay payment on the outstanding bill until the outcome of your appeal is known. This option buys you time and avoids immediate financial strain.

- Avoid Collections: Express your concern about the bill being sent to collections. Request that your medical provider's office refrain from sending the bill to collections during the appeals process. While they may or may not agree, it is worth asking to alleviate potential negative consequences.

- Negotiate and Set up a Payment Plan: Attempt to negotiate the amount you owe. See if there is flexibility in reducing the bill or creating a manageable payment plan. This can help alleviate financial pressure and demonstrate your willingness to work towards a solution.

- Gather Supporting Documentation: Obtain all relevant medical records, treatment details, and correspondence related to the denial. This includes doctor's notes, test results, and any other documentation that supports your appeal. This information will be crucial when building your case.

- Collaborate on the Appeal Letter: Work closely with your medical provider to craft a compelling appeal letter. This letter should address the specific reasons for the denial, provide detailed explanations, and include supporting evidence. A well-constructed appeal letter improves your chances of a successful outcome.

- Stay Organized and Persistent: Keep a meticulous record of all communications, including names, dates, and outcomes. Stay organized by creating a filing system for all relevant documents. Be persistent in your follow-ups with both the insurance company and your medical provider to ensure your appeal is actively addressed.

Remember, effective communication and collaboration with your medical provider are key to successfully navigating the appeals process and resolving outstanding bills.

Understanding the Ins and Outs of Insurance Billing: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Delay paying the bill until you know the outcome of your appeal

Delaying the payment of a bill until the outcome of an appeal is known can be a useful strategy, especially if paying the bill will cause financial hardship. This is a valid option for some types of bills, including medical bills and tax bills.

Medical Bills

If you receive a large medical bill that you think is incorrect, it is worth checking whether there has been a mistake in the billing or the insurer's processing of a claim. It is important to remain calm and polite when dealing with these matters, as the people on the other end of the phone are more likely to help you if you are pleasant. It is also a good idea to get a filing system going, so that you can keep track of all the relevant information.

If you are appealing a medical bill, you should first read the denial letter and identify the reason for the denial and the appeals process and timeline. If it is a billing or claims-processing error, call your medical provider's billing office and ask them to clear things up with the insurer. If it isn't a billing error, you will need to appeal to overturn the decision.

You can delay paying the bill until you know the outcome of your appeal. Ask your medical provider's office to not send the bill to collections, although they may or may not agree to do this. You can also set up a payment plan and try to negotiate the amount you owe to avoid having the bill sent to collections. If you pay the bill and then win your appeal, your health plan should reimburse you.

Tax Bills

If you disagree with a tax decision, you can appeal against it. In some cases, you may be able to delay paying a tax bill or penalty while you are going through the appeals process. For example, if you have appealed to HM Revenue and Customs (HMRC) against a direct tax decision (such as Income Tax, Corporation Tax or Capital Gains Tax), you can write to the HMRC office explaining why you think the amount is too much and what you think the correct amount is, as well as when you will pay it. HMRC will then inform you in writing if they agree to delay the payment.

If you have appealed against a penalty, you will not have to pay until your appeal has been settled. Similarly, if you have asked HMRC to review an indirect tax decision (e.g. VAT or Insurance Premium Tax), you will not need to pay until the review has been completed. However, if you are appealing directly to the tax tribunal, you will usually have to pay the tax before they will hear your case, unless you can demonstrate that paying the bill will cause you extreme financial difficulty.

Maximizing Valant's Features: Navigating Electronic Billing for Insurance Claims

You may want to see also

Explore related products

![]()

Set up a payment plan and try to negotiate the amount owed

If you're facing a large insurance bill, it's a good idea to set up a payment plan and try to negotiate the amount owed. Here are some steps to help you through the process:

Contact Your Insurance Provider:

Reach out to your insurance provider to discuss the bill and express your intention to set up a payment plan. Be polite and patient throughout the conversation, as the process may take some time. Ask about their payment plan options and try to negotiate a plan that works for your budget. Remember that the billing department is accustomed to handling negotiations, so don't be afraid to advocate for yourself.

Review Your Bill:

Request an itemized bill from your insurance provider to understand the charges in detail. Carefully review the bill for any errors, such as duplicate charges or services you didn't receive. Look for common mistakes, such as incorrect balances or charges for services that weren't provided. If you identify any discrepancies, contact the billing department to address them and request corrections.

Compare with Other Sources:

Compare the itemized bill with explanations of benefits (EOB) from your insurance company. EOBs are not bills but can help you identify discrepancies. If part of your bill should have been covered by insurance but wasn't, contact your insurance company to resolve the issue. Additionally, research the estimated costs of similar procedures in your area using tools like Healthcare Bluebook and FAIR Health. This information can provide valuable data points for your negotiations.

Seek Financial Assistance:

If you are facing financial difficulties, inquire about financial assistance programs offered by the insurance company or hospital. Non-profit hospitals, in particular, may have programs to assist low-income patients. You can also explore options like medical credit cards, loans, or patient advocates who can guide you through the process. Remember that amounts under $500 typically won't appear on your credit report, so work towards keeping your debt below this threshold if possible.

Negotiate the Amount:

Once you have all the necessary information, negotiate the amount owed. If you can afford to pay a lump sum upfront, ask for a settlement amount, as you may be able to get a significant discount. If a lump sum is not feasible, negotiate a payment plan with reasonable monthly payments and lower interest rates than a credit card. Remember that you can always try to pay less than the full amount, and it's in the insurance provider's interest to receive payments rather than having you default.

The Perils and Pitfalls of Insurance: Understanding the Risks Covered by Your Policy

You may want to see also

Explore related products

![]()

File an internal appeal by completing all required forms and submitting any additional information for the insurer to consider

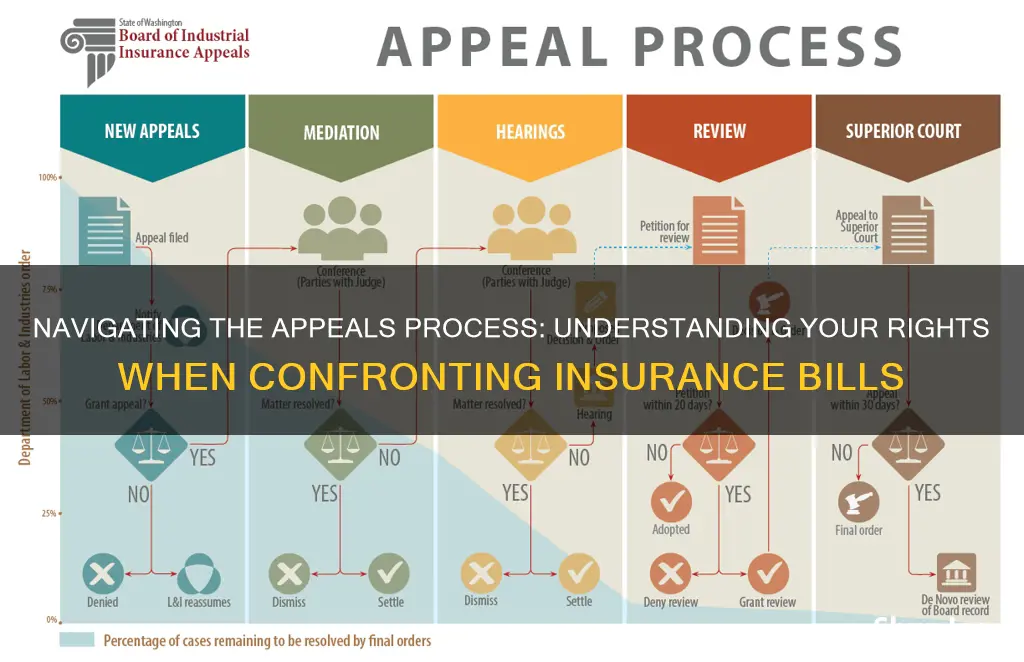

If your health insurance claim is denied or your coverage is cancelled, you have the right to file an internal appeal. This involves requesting that your insurance company reconsider its decision. You must file your internal appeal within 180 days (6 months) of receiving notice that your claim was denied.

To file an internal appeal, you need to:

- Complete all forms required by your health insurer. These may include the "Explanation of Benefits" forms or letters, which show what payment or services were denied. You will also need to include any documents with additional information that you sent to the insurance company, such as a letter or other information from your doctor.

- Alternatively, you can write to your insurer with your name, claim number, and health insurance ID number.

- Submit any additional information that you want the insurer to consider, such as a letter from your doctor explaining the necessity of the treatment.

- Keep copies of all information related to your claim and the denial.

- Send your insurance company the original request for an internal appeal and your request to have a third party (like your doctor) file your internal appeal for you. Make sure to keep your own copies of these documents.

If your situation is urgent, you can request an external review at the same time as your internal appeal. An external review involves having your appeal reviewed by an independent third party. If your insurance company still denies your claim after the internal appeal, you can then file for an external review.

Understanding Triterm Insurance: The Trifecta of Coverage

You may want to see also

Explore related products

![]()

If your internal appeal is denied, you can file for an external review

There are two steps in the external review process. First, you must file a written request for an external review within four months of receiving a notice or final determination from your insurer that your claim has been denied. You can do this by visiting externalappeal.cms.gov, calling 1-888-866-6205 to request an external review form, or by mailing an external review request form to MAXIMUS Federal Services. Secondly, the external reviewer will issue a final decision, either upholding your insurer's decision or deciding in your favor. Your insurer is required by law to accept the external reviewer's decision.

The external review process is available to you regardless of the type of insurance you have or the state you live in. If your state has an external review process that meets or goes beyond federal consumer protection standards, insurance companies in your state will follow that process. If your state does not meet these standards, the federal government's Department of Health and Human Services (HHS) will oversee an external review process for health insurance companies in your state.

Haven Insurance: Understanding the Fine Print

You may want to see also

Frequently asked questions

The first step is to file a claim, which is a request for coverage. You can usually do this by filling out forms or writing to your insurer with your name, claim number, and health insurance ID number.

Your insurer will notify you in writing about whether your claim has been accepted or denied, and they must explain the reason for their decision.

You can file an internal appeal, which involves requesting that your insurance company conduct a full and fair review of its decision. You must file your internal appeal within 180 days of receiving the notice of denial.

You have the right to take your appeal to an independent third party for an external review. This means the insurance company no longer has the final say over whether to pay the claim.

You can try to negotiate a lower price with your medical provider or reach out to the state insurance commissioner for assistance. Additionally, consider seeking help from a medical billing advocate, although they may charge a fee for their services.